Hot May Job Creation Puts Fed’s Focus Firmly on Inflation

Friday’s job report for May crushed expectations, with big March and April revisions as well.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

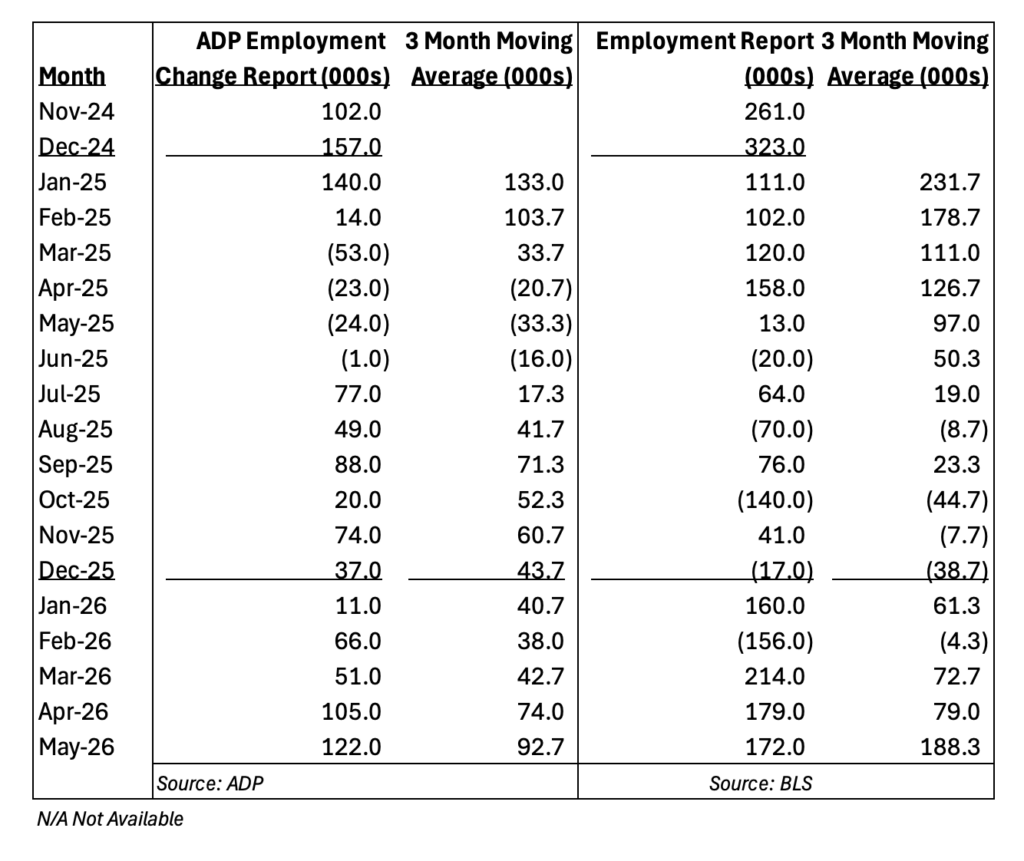

Following the job creation data reported earlier this week from ISM and ADP, we suspected the May Employment Report would come in somewhat stronger than the market consensus of between 85,000 and 105,000 jobs. However, like many others, we did not see the tally reaching 172,000 jobs, nor did we see the massive upward revisions for March and April. The change in total nonfarm payroll employment for March was revised up by 29,000 to 214,000, and the change for April was revised up by 64,000 to 179,000.

Viewed through the lens of a three-month moving average, the picture is one of accelerating job growth over the last few months. There will be some folks who quibble over the types of jobs being created, with leisure & hospitality and food service accounting for 70,000 of the number created in May. But when it comes to measuring job creation and the Unemployment Rate, a job is a job, and that’s most likely how the Fed is going to view it.

That reacceleration in the jobs market gives the Fed little reason to contemplate rate cuts. Mixed with the inflation data we’ve been getting and prospects for more of that with the May CPI and PPI data next week, not to mention renewed tariff talk from President Trump, the Fed’s focus is going to be on inflation. No two ways about it.

We have no Fed speakers Friday but Saturday brings a speech from Federal Reserve Governor Michael Barr, the last likely word from a Fed official before the central bank enters its blackout period ahead of the June policy meeting. We’ll look to see if Barr adopts an incrementally more hawkish tone on the topic of monetary policy, but we would be surprised if he didn’t, given the data we’re seeing.

To be clear, we are all in favor of more people working, putting more money in their pockets along the way, especially when inflation pressures are becoming a greater headwind to disposable spending dollars. The downside is that for more interest-rate-sensitive sectors, like housing, the timetable for rate cuts is that much further out.

More reason for us to stay on the sidelines for that sector and others at a time when the overall market is once again overbought.

More Pro Portfolio:

- Taking Advantage of Jensen Huang’s ‘Gift’

- We’re Tracking 29 Signals Across 9 Portfolio’s Investment Themes

- May Monthly Roundup: Sell in May? No Way!

At the time of publication, TheStreet Pro Portfolio had no positions in any securities mentioned.