Construction Spending Shows Positive Trend for These Four Holdings

And when it comes to Fed rate cuts, we’re watching these two data points next.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In today’s Daily Rundown video, we shared our thoughts on the favorable data points we found in today’s November Manufacturing PMI from ISM and now we’re turning to the October Construction Spending report. Construction spending in the United States during October rose by 0.4% month over month to a seasonally-adjusted annual rate of $2.174 trillion, a 5.0% gain compared to October 2023.

That marks the third consecutive increase in construction spending and the strongest since April. What stood out to us in the report was residential construction, which climbed 6.4% year over year, a quicker pace than non-residential construction, which rose 3.9% compared to year-ago levels. Residential construction also accelerated sequentially to its highest level in several months, a positive for our shares of Builders FirstSource BLDR, but also United Rentals URI, Vulcan Materials VMC and Waste Management WM.

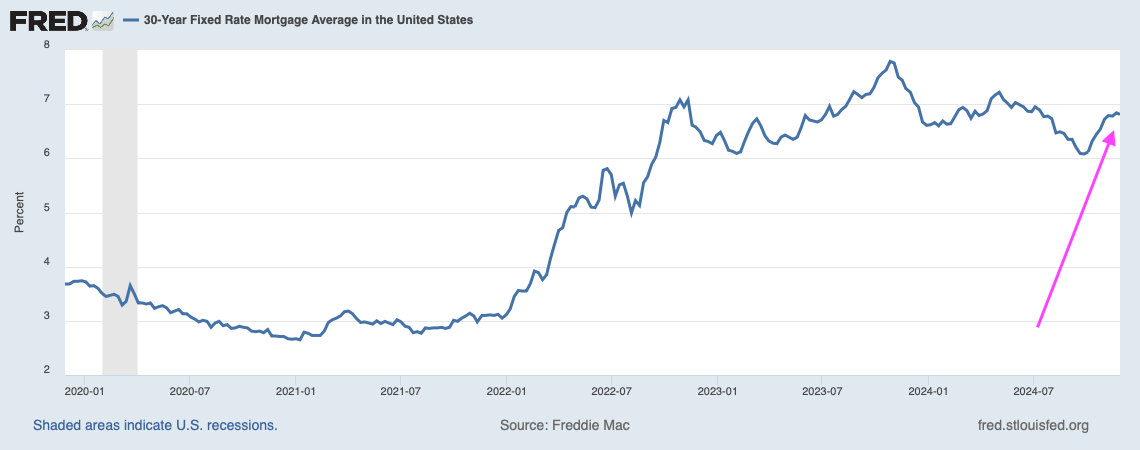

As you can see in the graph above, we’ve also seen mortgage rates rebound from their recent lows, which means we will want to see if the October residential construction spending gains continue in follow-up data. The rebound in mortgage rates has taken its cue from the move we’ve seen in the 10-year treasury yield but as we can see in the graph below, more recently that has softened.

Today’s better-than-expected inflation findings in the November Manufacturing PMI data from ISM suggest inflation may be getting back on track when it comes to the Fed’s 2% target. That is helping the 10-year treasury yield inch lower. While that November price data stopped short of falling into contraction territory, the print of 50.3 was far lower than the consensus forecast of 55.2 and October’s 54.8 figure.

That’s very constructive for Fed rate cuts, but we will want to see further confirmation in the November Non-Manufacturing PMI data that will be reported on Wednesday, December 4. If we see a similar move lower in that price data, we are likely to see the market warm up to a December rate cut and that should pull our BLDR, URI, VMC and WM shares higher.

We’ll also want to keep our eye on this week’s jobs data. Should the employment data be far stronger than expected it could counter-balance the collected PMI price data. We’ll know more once we have that November Non-Manufacturing PMI report and ADP’s November Employment Change report on Wednesday.

Based on what we learn, we'll revisit price targets for the holdings mentioned above as needed.

More Pro Portfolio

- We're Buying More of This Holding After Elon Musk's Comments

- Weekly Roundup: After a November to Remember, What's in Store for December?

- Headlines for the Holidays: News That Speaks to the Pro Portfolio

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, VMC and WM.