Shares for This Holding Retreat and Aggressive Buying Opportunity Looms

Recent price action for one of our portfolio holdings has left us wondering where we should pick up more shares.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*Below we share our reaction to Guggenheim’s downgrade of ServiceNow shares

*We also share the levels at which we would look to add more NOW shares to our holdings

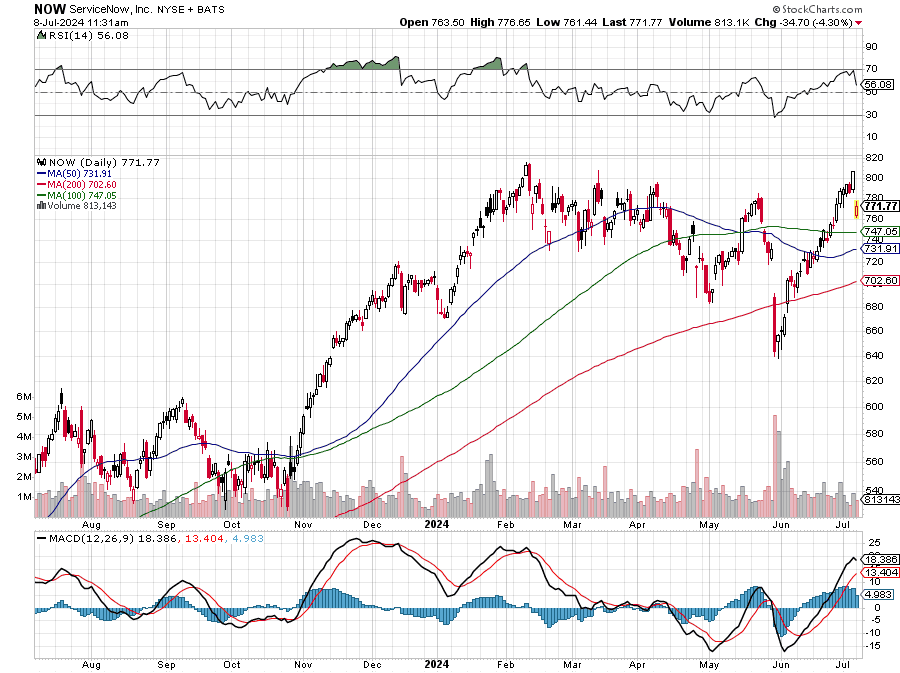

The portfolio’s position in ServiceNow NOW, one we picked up in early June, has been a champ but it’s being challenged today by a downgrade from Guggenheim. The firm questions the rich valuation, which is fair, but raises questions about the ability to monetize AI in the coming months, calling it more of a 2025 event. The crux of Guggenheim’s downgrade to a sell rating from neutral reflects what it sees as a rich valuation and findings from its field work, which contradicts the KeyBanc’s 2024 CIO survey findings we shared with you last week.

To recap, the KeyBanc survey found slightly stronger budget spending this year with further acceleration in 2025. Incrementally larger spending, in what could be a back-end loaded 2024, likely reflects key corporate initiatives including AI and cybersecurity. That supports our long-term thinking on ServiceNow, which is already seeing stronger pricing with its AI offerings and that should fuel EPS growth as it becomes a larger part of the company’s revenue mix.

While we may not agree with Guggenheim’s thinking, NOW shares rocketed higher by more than 25% since bottoming out in late May right before we scooped some up for the portfolio. While we hoped to pick up more shares, the quick catapult-like rebound in the shares made it impractical, putting us on watch for other opportunities.

While some may want to jump at this modest pullback relative to the overall move in the last five to six weeks, we will soon be entering the June quarter earnings season with both the S&P 500 and Nasdaq Composite overbought. Expectations are running high, and given the move in NOW shares, the company will have to deliver a pristine quarter and stronger-than-expected outlook when it reports on July 24, 2024. Between now and then, we will have a few hundred companies report and what they say about AI spending will matter. If the overwhelming message is that they are spending on AI, it will add further support for our thesis on NOW shares. On the other hand, if the start of the June quarter earnings season leaves folks wanting, we could see the market repeat the more than 4% pullback experienced in mid-April.

This brings us to the question we’re pondering: Where should we pick up more NOW shares?

While we would love to buy more NOW shares much closer to our $662.65 cost basis, the odds of that are likely low. We do see support at the 100-day and 50-day moving averages at $747 and $732 and if NOW shares found their way to the lower end of that range it would be a nice level to add more NOW shares to our holdings. Below those levels, there is further support near $702 to $703, which makes for an even more aggressive buying opportunity should the shares find their way there.

More Pro Portfolio:

- Locking in Big Gains on This High-Flying Stock

- Weekly Roundup: Reasons to Be Cautious

- Reading the 'News Signals' From Our Investing Notebook

At the time of publication, TheStreet Pro Portfolio was long NOW.