Workday Gets It Done

After WDAY's beat, let's check the prices and key technicals, and what I'm watching.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Workday WDAY posted on Thursday night fiscal second-quarter results, revealing an adjusted earnings per share of $1.75 (GAAP EPS: $0.49) on revenue of $2.085 billion. These top- and adjusted bottom-line results both beat Wall Street's expectations, while the sales print was good enough for year-over-year growth of 16.7%. Adjustments were made primarily for the purpose of share-based compensation expense.

Subscription revenue grew 17.2% to $1.903 billion. The 12-month subscription revenue backlog is now $6.8 billion, up 16.1% from the year-ago period, while total subscription backlog is $21.58 billion, up 20.9%. The company now has more than 70 million users under contract and more than 2,000 Workday Financial Management Customers. Workday now has strategic working arrangements with Salesforce CRM, Equifax EFX, and Kainos.

Operations: Solid

As total revenue was growing 16.7% to $2.085 billion, total costs and expenses increased 12.7% to $1.974 billion. This left a unadjusted operating income of $111 million, up from $36 million, on an operating margin of 5.3%, up from 2.0%. On an adjusted basis, operating income increased from $421 million to $518 million, as operating margin increased from 23.6% to 24.9%.

After accounting for interest, taxes and other income, unadjsuted net income attributable to shareholders printed at $132 million, up from $79 million. This works out to $0.49 per diluted share, up from $0.30. On an adjusted basis, the EPS of $1.75 compares well to $1.49 for the year-ago comparison.

Guidance: Lookin' Good

For the current quarter, Workday sees subscription revenue of $1.955 billion, which would be good for annual growth of 16%. For the full year, the company projects subscription revenue of $7.7 billion to $7.725 billion, which would be good for year-over-year-growth of 17%. It also sees an adjusted operating margin of 25.25%. Readers will see that the adjusted operating margin for the just-reported quarter was 24.9%. This does have Wall Street a bit excited over this outlook.

Strong Fundamentals

For the period reported, Workday generated operating cash flow of $571 million (up 34.4%). Out of this number came capital spending of $55 million, leaving free cash flow of $516 million (up 43.3%). Out of that number, the company repurchased $312 million worth of common stock for the corporate treasury. Workday does not pay cash dividends to shareholders.

As of the end of the reported quarter, Workday held a cash position of $7.373 billion and current assets of $9.2 billion. Current liabilities add up to $4.513 billion, including no short-term debt, but $3.549 billion in unearned revenue. As we recall, unearned revenues are not financial obligations, but rather a tally of goods and / or services owed. This puts the current ratio at a strong 2.03. Adjusted for unearned revenue, this ratio rises to an incredibly muscular 9.54.

Total assets amount to $16.234 billion, including $3.588 million in goodwill and other intangibles. At 22% of total assets, this is enough to put on one's radar, but not yet enough to be concerned over. Total liabilities less equity comes to $7.889 billion. This does include $2.982 billion in longer-term debt that the company could take care of out-of-pocket almost two-and-a-half times over. In short, this is an excellent balance sheet.

Wall Street: Buys and Holds

Since these earnings were released last night, I have come across 13 highly rated sell-side analysts who have opined on WDAY. Just as a side note, for those interested in doing more work on their own, an unusually large number of less highly rated analysts chimed in on this name as well.

Across these 13 analysts, after allowing for changes, there are 8 "Buy" or buy-equivalent ratings and 5 "Hold" or hold-equivalent ratings. One of the "holds" did not set a target price, so we are working with 12 of those. The average target price across them is an even $290 with a high of $315 (Keith Weiss of Morgan Stanley) and a low of $255 (Yun Kim of Loop Capital).

Once omitting those two as possible outliers, the average target across the other 10 rises to an even $291. The average "buy" target is $301.25, while the average "hold" target is $267.50.

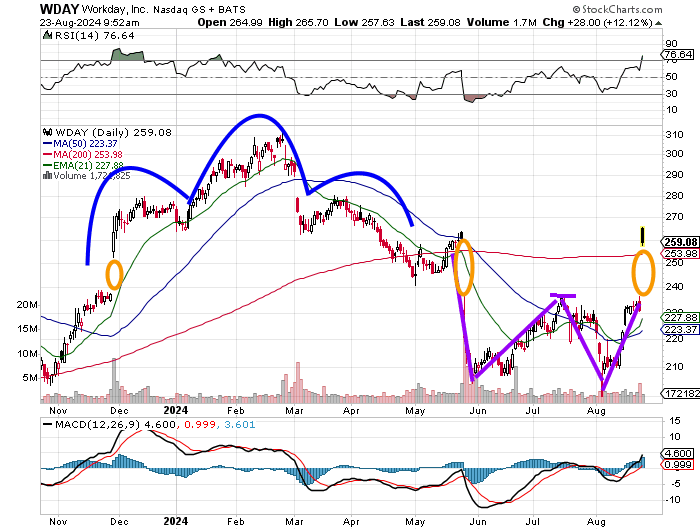

My Thoughts on the Quarter, the Chart

The company had a nice quarter. Cloud-based, AI-infused human capital management is a big business, but Workday appears to be holding its own or even better than that. Key competitors would be SAP's SuccessFactors HCM SAP, ADP Workforce Now ADP and Oracle Fusion Cloud HCM ORCL. That's a crowded field, but sales of subscriptions have been steady and are projected to remain so.

During the call, not part of the official guidance, CFO Zane Rowe said the focus areas "have been ramping over the past year, providing us better insight into how their growth trajectories augment our core business. As we incorporate this into our planning, along with the current environment, we now expect subscription revenue growth in the mid-teens for both FY ‘26 and FY ’27."

I think that quote is at least contributing to the stock's overnight pop that has now turned into a gap up opening.

Also, CEO Carl Eschenberg in the press release touted the power of Workday's AI-powered platform and "expanding partner ecosystem."

A lot's going on in this chart, but readers will see that for about a year now, WDAY has traded by its technicals as if by clockwork.

From November 2023 into late April 2024, WDAY built a near perfect head-shoulders-pattern that produced a sell-off that itself created a gap down in May. From May into the present, WDAY has developed a near perfect double-bottom pattern of bullish reversal with a $237 pivot. The stock broke through that pivot to the upside with a violent move this morning, filling the gap from May.

Additionally, as WDAY has retaken its 200-day simple moving average, the stock's reading for relative strength has spiked as has the posture of its daily moving average convergence divergence indicator, which is now bullish. The 200-day simple moving average, and whether it can be held, is key for WDAY going into the weekend. My target price for these shares, in which I unfortunately have no position, would be $284 based on the already mentioned pivot. But based on where the 200-day simple moving average currently stands, I can see a bull case for $305.

Should the stock fail to hold the 200-day SMA, I would be an interested buyer toward the lower bound of the overnight unfilled gap.

At the time of publication, Guilfoyle had no position in any security mentioned.