My Tech Price Target Reveal; Out-of-This-World IPO; Peace … At Last?

Let’s check my price targets for Micron and other storage and semiconductor stocks, SpaceX’s IPO, the latest on Iran talks.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The prospect of peace in the Middle East seems somewhat realistic this time. We think. After many fits and starts that have unleashed the algorithms that control financial market price discovery in one direction or the other, this time is different, we’re told. On Thursday, after several days of downward pressure had impacted US markets, President Trump pulled back from threats he had made just hours earlier. These threats were made against Iranian military sights and included the seizure of locations crucial to Iran’s oil industry.

The president said that Iranian Supreme Leader Mojtaba Khamenei has signed off of a plan that would pave the way for additional talks regarding Iran’s nuclear program. Iran had made demands in the past that any plan include the release of tens of billions of dollars that had been frozen by U.S. sanctions. This capital is crucial to the Iranian regime as that nation’s military and economy had both been shattered since the start of the conflict.

Apparently, on Thursday, a delegation from Qatar returned from a trip to Tehran announcing that Iran would agree to some new language that could be incorporated into the existing draft of a peace plan that had already been on the table. U.S. officials were informed that Iran had come closer to meeting its nuclear demands after the past two days of bombing and the president called off plans to increase the pace of the attack for a third.

The president added that a signing ceremony could happen as soon as this weekend, in Europe and that Vice Pres. JD Vance would likely represent the U.S. Markets rejoiced.

There’s More…

Overnight, Iranian state media reported that a draft version of a 14-point memorandum of understanding meant to end the U.S. / Iran war includes a commitment by the U.S. to lift oil sanctions and a commitment by Iran to reopen the Strait of Hormuz. The draft also supposedly includes the eventual, but not immediate, release of half of Iran’s frozen funds, and the lifting of the U.S. naval blockade of Iranian ports. Iran is also apparently asking for the U.S. and its allies to present reconstruction plans for that nation that would amount to at least $300 billion. Again, this is being reported by Iran’s Mehr News Agency, so treat this information as “subject.”

It’s IPO Friday!

Elon Musk’s SpaceX (SPCX) goes public today. The stock is set to begin trading today at the Nasdaq Market Site. On Thursday evening, the firm priced 555.6 million shares at $135 apiece. The funds raised at the moment, come to more than $75 billion, with an over-allotment option where the underwriters could exercise an additional 83.3 million shares. That would bring the fundraising to $86 billion and would value the company at $1.78 trillion. The deal drew more than four times the shares available as investors placed orders worth more than $100 billion.

Goldman Sachs (GS), JPMorgan Chase (JPM) and Morgan Stanley (MS) are the leading managers of what is a 23-bank syndicate. Goldman is running the order book. Just as a heads up if one has placed orders. In my experience, Goldman Sachs is probably the slowest bookrunner that I know of and it’s not close. I doubt that the first trade will occur before lunchtime. How well this stock performs after it opens could have implications down the road for both Anthropic and OpenAI.

Thursday’s Market

It was “game-on” for U.S. markets on Thursday after the markets adopted a more optimistic stance after catching wind of the “memorandum of understanding.” Crude oil prices simply fell out of bed. I now see WTI Crude trading with an $83 handle. Bond traders flocked back into U.S. Treasury debt securities forcing yields lower across the slope of the curve. I now see the U.S. Ten-Year Note paying 4.44% after having paid as much as 4.58% earlier this week.

On Thursday, during the regular session, the S&P 500 gained 1.75% as the Nasdaq Composite popped for 2.54%. The Dow Transports added an impressive 3.21% as the small-to-mid-cap indexes all gained between 2.48% and 3.02%. Really taking the football and running with it, the Philadelphia Semiconductor Index soared 7.91% on the day, led by SanDisk (SNDK), KLA Corp (KLAC) and Lam Research (LRCX).

Breadth: Minty Fresh!

Market breadth was minty fresh on Thursday. Eight of the 11 S&P sector SPDR ETFs closed out the day in the green, led by Technology (XLK), the Materials (XLB) and the Industrials (XLI). Energy (XLE), for good reason, finished the session at the bottom of the performance tables. Overall, growth and cyclicals easily outperformed defensives.

Winners beat losers by a rough eight-to-three margin at the NYSE and by about five-to-two at the Nasdaq. Advancing volume took a commanding 74.5% share of composite NYSE-listed trade and a 70.7% share of composite Nasdaq-listed activity. Aggregate trading volume was higher as well. Activity was up 7.8% day over day across NYSE-listings and up 6.1% across Nasdaq-listings. Activity also increased across the membership of the S&P 500.

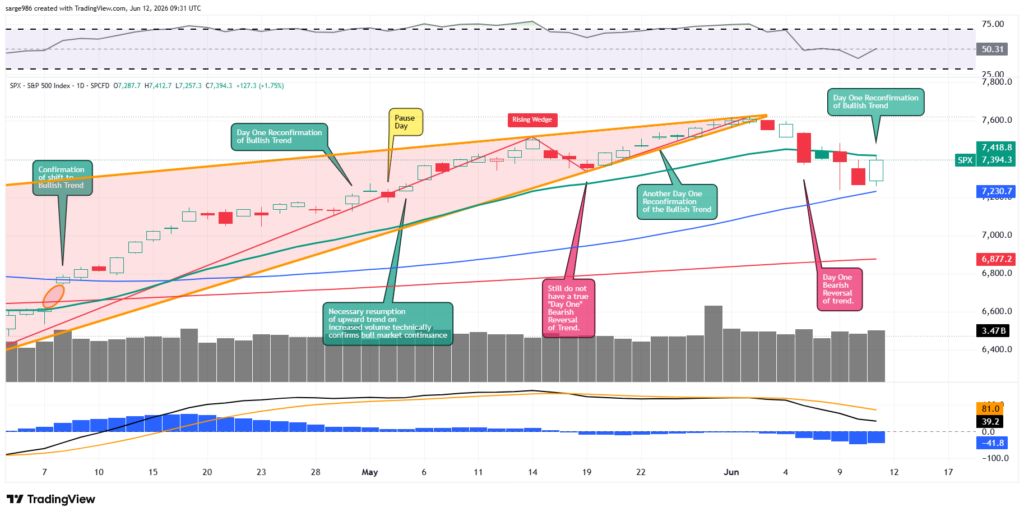

Yes… the Chart

This action does indeed make Thursday a new “Day One” bullish reversal of trend. As readers are well aware, all week, despite the selling pressure, there was never a technical

confirmation of the bearish trend after last Friday’s bearish reversal. Now, the bulls will need to see a pause and then confirmation. Relative strength is neutral and the daily MACD is still set up quite bearishly, so this positivity is tenuous at best. A peace deal needs to happen, and the market needs to absorb SpaceX well.

Target Price Updates

I appeared on Fox Business on Thursday afternoon with the mighty Charles Payne. This was my first appearance on live television in quite some time and the response from viewers/readers has been shockingly impressive. Thank you. As requested overnight by those interested, I will go over for you here, the target prices that I mentioned on that show as many did not have their pens at the ready. (I guess most talking heads are not nearly as forthright with their positions and their targets / plans. Who knew?)

The Foundry Capacity Basket:

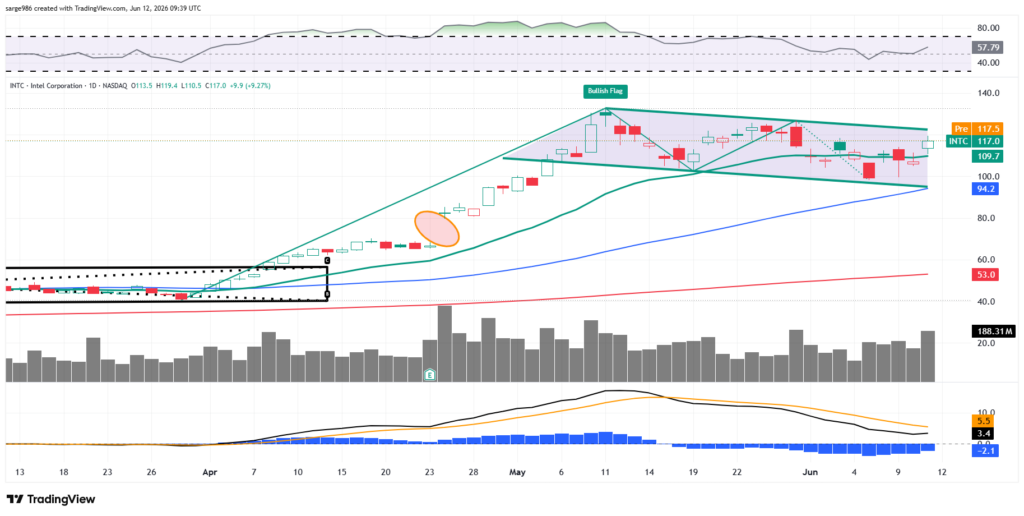

1) Intel (INTC)

Target Price: $155 (reiteration)

Pivot: $129

Add: Down to 50-day SMA (currently $94)

Panic: Loss of 50-day SMA.

2) Taiwan Semiconductor (TSM)

Target Price: $460 (reiteration)

Pivot: $382

Add: Down to 50-day SMA (currently $397)

Panic: Loss of 50-day SMA.

Memory / Storage Basket:

1) Micron Technology (MU)

Target Price: $1,375, up from $1,100.

2) SanDisk (SNDK)

Target Price: $2,100 (reiteration)

3) Western Digital (WDC)

Target Price: $750 (reiteration)

4) Seagate Technology (STX)

Target Price: $1,150 (reiteration)

Economics (All Times Eastern)

10:00 – U of M Consumer Sentiment (Jun-adv): Expecting 46.3, Last 44.8.

10:00 – U of M One-Year Inflation Expectations (Jun-adv): Expecting 4.8%, Last 4.8%.

10:00 – U of M Five-Year Inflation Expectations (Jun-adv): Expecting 3.8%, Last 3.9%.

1:00 p.m. – Baker Hughes Total Rig Count (Weekly): Last 563.

1:00 – Baker Hughes Oil Rig Count (Weekly): Last 431.

The Fed (All Times Eastern)

Fed Blackout Period.

Today’s Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long INTC, TSM, MU, SNDK, WDC, STX equity.