The Games Begin, Microsoft, AMD Earnings, Trading Tesla, CrowdStrike Tumbles

After tiptoeing through the tulips Monday it's game on now for the market, as Tesla and CrowdStrike pass each other on the escalator. Plus, good fiscal news? Gemany lags? Yup.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

At last.

The games finally begin this day. A glance at Tuesday's earnings highlights below show a morning focus on big pharma and then that shifts to large or mega-cap tech this evening. That's when we'll hear from $3 trillion enterprise AI/cloud/all things tech giant Microsoft MSFT and perennial AI-capable chip designing runner-up Advanced Micro Devices AMD. That will be when the fun and games really take over. Yes, we'll dance with the Fed on Wednesday afternoon and the Bureau of Labor Statistics on Friday morning, but from Tuesday afternoon through Thursday afternoon, from a corporate/earnings perspective, big tech will be headlining this show.

Markets behaved rather timidly on Monday as if forced to cross flower beds on foot while trying to leave no damage behind. With the earnings, macro and central banking calendars all about to heat up, it's no small wonder that traders and investors tried to "tiptoe through the tulips" on Monday.

Even Treasury markets were quiet. The U.S. 2-Year Note went nowhere, ending the day yielding 4.38%, which is where the day began. U.S. 10-Year paper "rallied" as that yield ratcheted down two basis points to 4.17% as that spread has managed to reinforce its inversion over the past couple of days after almost a month of "steepening" or moving towards an un-inversion.

Forgive My Brevity

If my work seems abbreviated or less wordy in any way, I apologize. I dislocated my left shoulder in the garage gym last night. It was a pretty bad one as far as dislocations go.

I was alone on the bench under a bunch of weight, and it took me a while to get the ball back in the joint. At least there were no crunchies, which means I probably did it right (I am not new to dislocations). Hence, I'm pretty much typing with one hand this morning.

Marketplace

What action there was across the regular trading session on Monday was in an unwind of the recent rotation into smaller-cap stocks. Though gains were not truly evident across large-caps, the small-cap indexes took a hit. The Russell 2000 gave back 1.09%, as the S&P 600 lost 0.68%. This happened as the S&P 500 and Nasdaq Composite added a paltry 0.08% and 0.07%, respectively. The general lack of movement at that level means that the S&P 500 remains on the right side of its 50-day simple moving average (SMA), while the Nasdaq Composite continues to look on from the wrong side of that fence.

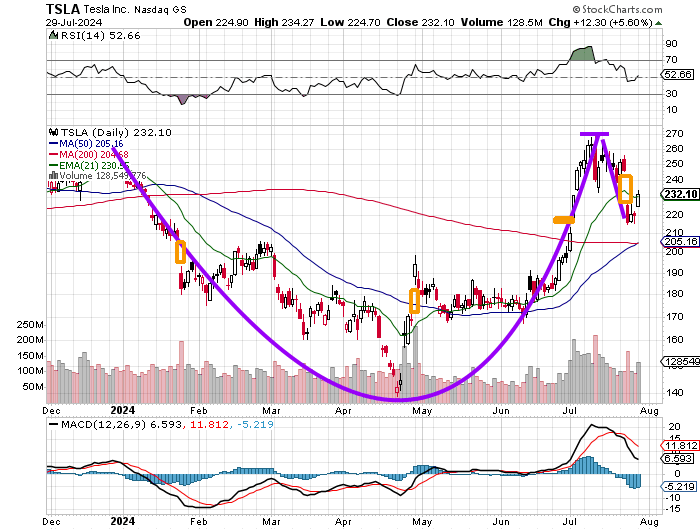

Despite a generally sullen feel to the equity marketplace on Monday, seven of the 11 S&P sector SPDR ETFs shaded green for the day, led by the Discretionaries XLY as Tesla TSLA rallied 5.6%. Tesla took back a chunk of last week's post-earnings losses during the session. Energy XLE led the losers on Monday as the U.S. dollar rallied, and crude oil weakened.

For the day, losers beat winners by roughly 7 to 5 at the NYSE and by close to 7 to 4 at the Nasdaq. Advancing volume took a 39% share of composite NYSE-listed trade and a 46.6% share of composite Nasdaq-listed action as aggregate trading volume itself sagged close to 10% on a day-over-day basis for all names.

Back to Tesla. Readers will see that since we did a focused piece on this name about four weeks ago, the cup pattern that we spoke of at that time has indeed added a handle that may have found its depth late last week. With a still neutral Relative Strength Index (RSI), and a suddenly negative looking daily Moving Average Convergence Divergence (MACD), the stock itself is setting up for a potential rally. No, I am not in the name.

On Monday, TSLA took back its 21-day exponential moving average (EMA), while the shares benefited from an algorithmic reaction to a golden crossover of its 200-day SMA by its 50-day SMA. With the pivot having migrated from the left side of the cup to the right ($271), technically, the case can be made for a price target between $310 and $325. The EV manufacturer has struggled of late and there may not be a fundamental story in place to support such targets.

Unless one is really investing in Tesla's FSD version 12.5 and beyond. The latest update to the company's full self-driving software is the next visible step in the evolution towards an evolving demand for real-world AI... and will be meaningful as well in the evolution of not just the "robotaxis" but also in humanoid looking robots performing menial tasks.

Anyone Else Notice This?

The Eurozone's flash Q2 GDP printed at growth of 0.3% q/q this morning despite the fact that Germany's flash GDP hit the tape at a disappointing -0.1% with expectations for +0.1%. The German economy has now landed in a state of contraction for two quarters of the past three and for four quarters so the past seven. The Eurozone has now painted flat or in expansion for three successive quarters.

A European economy expanding despite, not because of German economic performance. How many would have expected that outcome a few years ago? Spain's economy, by the way, is on fire (in a good way) The ECB does not meet on policy again until mid-September.

The Yellow Rose

The Dallas Fed Manufacturing Index for July printed at -17.5. That district has become the poster child for the "Industrial Recession" that the U.S. economy has now been mired in for years.

Manufacturing activity in the Dallas district has now slowed from the month prior for 27 consecutive months. Not a misprint.

Some Decent News

Yes, we are a fiscal trainwreck. That hasn't changed. That's also not a shot at the current administration specifically. Though the Biden administration and our legislators did pour a little too much kerosene on that fire (which is why consumer-level inflation that would have spiked anyway, did go as high as it did), Joe was really the fourth president in a row to behave recklessly when considering fiscal matters.

On Monday, the U.S. Treasury Department did announce that it ended June with a roughly $778 billion cash balance, above the $750 billion targeted for the quarter in April. The Treasury also projected the need for an estimated $740 billion in net borrowing for the quarter ending September 30. That's down quite a bit from the $847 billion originally projected for the current quarter. Treasury now expects to end this quarter with a cash balance of $850 billion and a year-end cash balance of $700 billion.

The Treasury will outline its refinancing plans in regard to these borrowing needs this Wednesday morning, ahead of FOMC-mania that afternoon. This of course, does not solve our budget imbalances, but is better than projecting greater-than-expected needs and it is better than a sharp stick in the eye.

On That Note...

Anyone else following Stephanie Pomboy at MacroMavens and her idea concerning the finding of support for U.S. sovereign debt during a slower period of domestic economic activity? Pomboy suggests freeing the interest earned on Treasury debt securities from federal tax obligations much the way municipal debt works.

Would this unleash enough increased demand to actually lower rates without a significant reliance upon central bankers as the buyers of last resort? Pomboy thinks maybe it does and I certainly think some work should be done in finding out. According to Pomboy, a one percentage point drop in Treasury yields across the spectrum might cost the Treasury $100 billion in tax revenue but save the Treasury approximately $350 billion in debt service costs.

Would it work? I don't see any other bright ideas. It might buy some time as "we" try to figure out how to move forward without the monetization or at least delay that monetization of the debt that seems unavoidable at this point.

Not So Fast, My Friends

Readers likely noticed that Sarge's old pal CrowdStrike CRWD fell out of bed again last night. During the regular session on Monday, CRWD gained more than 1%, as Morgan Stanley analyst Hamza Fodderwala (who is not highly rated by TipRanks ) wrote "Bottom line, we are slightly more constructive on CRWD's ability to limit long-term reputational damage post the outage given the company's swift response and partner checks indicating limited churn risk so far."

Remember, switching up on cybersecurity providers is not something done on the cheap, so there could be some foot dragging. Fodderwala added, "However, we believe the stock is nearing the bottom here given valuation discount versus large-cap peers and continue to see recent events as a two- to three- quarter headwind."

Huzzah! Uhm, not so fast, Sparky.

After the closing bell, CNBC broke news that Delta Air Lines DAL had hired famed attorney David Boies of Boies Schiller Flexnie. It is expected that the airline will be seeking compensation from both CrowdStrike and Microsoft after the outage had crippled their business for several days. Analysts currently see the outage as a $500 million disruption to Delta's bottom, not top line, impacting both Q3 and full-year performance materially.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 4.9% y/y.

09:00 - Case-Shiller HPI (May): Expecting 7.4% y/y, Last 7.2% y/y.

09:00 - FHFA HPI (May): Expecting 0.2% m/m, Last 0.2% m/m.

10:00 - CB Consumer Confidence (July): Expecting 99.9, Last 100.4%.

10:00 - JOLTs Job Openings (June): Last 8.14M.

10:00 - JOLTs Job Quits (June): Last 3.459M.

16:30 - API Oil Inventories (weekly): Last -3.9M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: AMT (2.58), ADM (1.24), ITW (2.47), LDOS (2.27), MRK (2.14), PFE (0.46), PG (1.37), SOFI (0.01), SYY (1.38)

After the Close: AMD (0.68), CZR (0.07), LSTR (1.46), MSFT (2.94), QRVO (0.71), SWKS (1.21), SBUX(0.93)

At the time of publication, Guilfoyle was long ADM, SOFI, AMD, MSFT and CRWD equity.