Season of Change, Big Tech's Big Week, S&P, Nasdaq Charts, How Many Rate Cuts?

Remember the Recession of 2022? Neither does anyone else. Remember all those jobs created in 2023? We now know that more than half of them were never actually created.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For all things, for all times, there is a season. Some seasons last seemingly forever. Asset-backed currency had been the way currency had been done, since people got tired of both the nuisance and the risk associated with carrying gemstones and coins minted of various precious metals around with them. That now seems ridiculous, does it not? Who could have even imagined the wonders and potential pitfalls associated with both fractional banking and fiat currency. Yet here we are. These "norms" have led to an over-indebted world where there is no way out, there is no way around the stench and public humiliation of modern monetary theory. For there will be a monetization of said debt, global in nature, that will destroy the fortunes of those who did right, while making fortunes for others who maybe did not.

Oh, that will be some season alright. Will that season end? Probably not in my lifetime. Talk about inviting the black swan into the living room. Waddle, waddle, honk, honk... surprise!! If it were predictable and avoidable based on knowledge already held by the many, for the swan would not be black, now, would it? Maybe just live within a budget and pay off one's bills on time. Don't be foolish. Such behavior sounds rules bound. Surely, they must know that rules are only for peasants. Surely that whole... "Blessed are the meek, for they will inherit the Earth." (Matthew 5:5) thingee mentioned in the Beatitudes went right over their heads.

Now, this week, we'll think about a much shorter kind of season. The season that ends and begins anew as the central bank moves "in spirit" from a "higher for longer" policy towards something far more fluid. As the wheel turns from what has been for a couple of years to what will be, very soon. For the Fed has a mandate. A dual mandate. Price stability. Full employment. One often becomes what I would describe as opportunity cost for the other. Rob Peter, pay Paul so to speak. The war has been waged upon consumer-level inflation. Inflation has slowed. Inflation has not been beaten. Yet, the economy calls... Labor markets are getting heavy. No recession in sight, say those loose with concept and keen on maintaining a narrative. Yet nearly every metric followed says different.

Perhaps this time, the Fed knows it's different. Perhaps this time, the pain will be felt so broadly and be so obvious that there can be no tall tales told. Remember the Recession of 2022? Neither does anyone else. The definition of recession was simply changed in order to accommodate the story told. Remember all those jobs created in 2023? We now know that more than half of them were never actually created. The BLS itself told us last week.

The financial media? Not interested. I am not political. I try not to be anyway. However, I do have to wonder if "they" would have changed the definition of "economic recession" in 2022 for every administration. I have to wonder if "they" would have actually reported the story last week when the BLS came forth with more accurate, but far less flattering data for 2023 job creation. I have to wonder if economic growth would have been reported as it was in 2023, when every economist in the world knows that you average GDP and GDI when they are not close. That's not what "they" did.

Enjoy the season, my faithful band. For the season of change is coming. A season of much wailing and gnashing of teeth awaits. But not yet.

Into the Now

You may want to buckle that chinstrap. We don't need any John Waynes around here.

With 41% of the S&P 500 already having reported their second-quarter financial results, this week, as July melts into August, will be our busiest earnings week yet. Mega-cap tech stock after mega-cap tech stock will release their numbers, project their futures and mention the phrase "AI" as often as possible during their conference calls. Will it matter? For the smell of rate cuts is in the air, and a rotation out of the mighty and into the lost has begun. Can it last?

Surely many small-caps, overly indebted and less than profitable as many are, will be able to push the string a little further with reduced borrowing/refinancing rates at hand. Surely, those "hold until maturity" portfolios on the balance sheets of both large and small banks alike will suddenly appear less horrific. Those regional lenders will both inhale and exhale, while cracking a fake smile for those who care.

How Fitting

Assistant Secretary of the Treasury Josh Frost will release the Treasury Department's latest quarterly refunding announcement on Wednesday morning. That afternoon Fed Chair Jerome Powell and his band of merry riders very likely pave the way for a first rate cut (of the coming change in season).

One hand must "very independently" wash the other, you know.

Also, how fitting that the BLS twin (and in all likelihood extremely inaccurate) employment surveys for the month of July will cross the tape a mere 42 hours after the Fed Chair takes the podium before the financial press.

The Week That Was

There was not a lot of macro last week, but the BEA did release the agency's first (of three) estimate for Q2 GDP. The headline print hit the tape at growth of 2.8% (q/q, SAAR) which was considerably better than the 2% that Wall Street was looking for. The Atlanta Fed, to its credit, went out looking for a 2.6% print, which was much closer than its peers who were all much lower.

Within that release, there was a rebound in both personal consumption expenditures and inventory building. Personal consumption accounted for 157 basis points of the whole, up from 98, while inventory building accounted for 82 basis points up from -42. Government spending added 53 basis points up from 31. Net imports/exports subtracted 72 basis points getting us to 2.84%.

So, why are financial markets acting like the Fed is rushing towards rate cuts if inflation has not yet been defeated and the economy is growing at a 2.8% annualized pace? Probably because the economy is not as hot as that number sounds. Remember 2023, when real GDP showed growth of 2.5% but real GDI showed growth of only 0.4%. The first estimate for any quarter does not include GDI. Therefore, there is no proper check on the number as of yet.

On Friday, Personal Income for June disappointed, as Personal Spending landed on the number. What encouraged markets to rally on Friday, was the fact that PCE and Core PCE for June both printed close to expectations. Never mind that Core PCE hit the tape just a tad on the warm side both on a month-over-month and year-over-year basis. We've got rates to cut. Haven't you seen the spread between the yields of the U.S. 10-Year and 2-Year Notes move sharply towards un-inverting? Get with it, man!

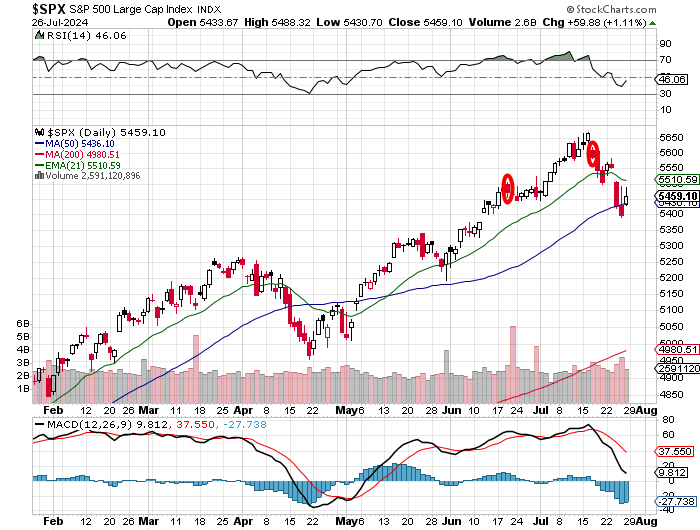

The S&P 500 Held the 50-Day SMA!

How key was the S&P 500 maintaining contact with the 50-day simple moving average (SMA) on Thursday and then retaking and holding that line on Friday? Both Relative Strength and the daily Moving Average Convergence Divergence (MACD) suggest that there will be another test.

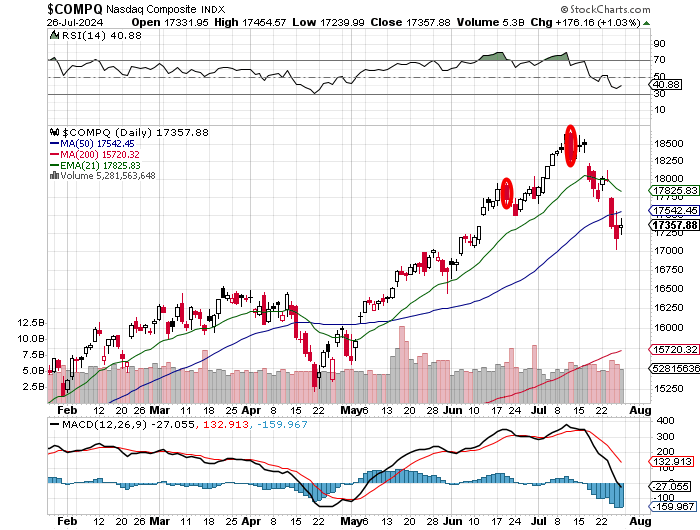

The Nasdaq Composite... Uh Oh!

How important was it that the Nasdaq Composite's contact with the 50-day SMA was lost on Thursday and never re-established on Friday. Another attempt must be made ahead of this week's key earnings and FOMC meeting.

Rotation-alapalozza

"You will be mine; you will be mine all mine."

- Mick Jagger

- The S&P 500 gained 1.11% on Friday to close the week down 0.83%.

- The equal-weight S&P 500 gained 1.44% on Friday to close the week up 0.82%.

- The Nasdaq Composite gained 1.03% on Friday to close the week down 2.08%.

- The Nasdaq 100 gained 1.03% on Friday to close the week down 2.56%.

- The Russell 2000 gained 1.67% on Friday to close the week up 3.47%.

- The S&P Small Cap 600 gained 1.81% on Friday to close the week up 3.54%.

- The S&P Mid Cap 400 gained 1.63% on Friday to close the week up 1.98%. .

- The Dow Transports gained 1.66% on Friday to close the week up 0.86%.

- The Philly Semiconductor Index gained 1.95% on Friday to close the week down 3.11%.

- The KBW Bank Index gained 0.95% on Friday to close the week up 2.61%.

On Friday, all 11 S&P sector SPDRs shaded into the green with eight of these funds gaining at least 1%. All good? Not sure. Trading volume on Friday's "up" day was down significantly from Wednesday and Thursday when the S&P 500 and Nasdaq Composite were slapped around pretty good.

For the week, seven of these sector SPDRs closed higher with the Utilities XLU and Health Care XLV out on top. While defensives provided safe haven, cyclicals and growthy type sectors were introduced to the ugly stick. Discretionaries XLY gave up 2.77% led lower by the autos. Ford Motor F, General Motors GM and Tesla TSLA were all beaten severely.

Technology XLK was not far behind at -2.08% as sellers continued to pile on CrowdStrike CRWD. Alphabet GOOGL reported on Monday and provided no relief, citing expectations for increased AI-related expenses going forward. That makes this week even dicier as many of Alphabet's peers will be reporting.

The Call of the Wild

Considering this Wednesday's Fed policy decision, according to futures markets trading in Chicago, the probability for no change made stands at 96%, as the likelihood for a 25-basis point reduction made to the target range for the Fed Funds Rate by September 18 is now up to 100% from 92% a week ago. The odds of at least 50-basis points worth of rate cuts by November 7 now stands at 72%.

By year's end? A 69% likelihood for 75 basis points worth of rate cuts are now priced in. How about a year from now? A 67% chance for 150 basis points worth of cuts. Without a collapse in labor markets coupled with economic contraction? No promises. Those kinds of things are contagious, you know.

Earnings and Valuation

According to FactSet, for the second quarter, with 41% of companies having already reported, the S&P 500 is expected to sport earnings growth of 9.8% on revenue growth of 5%. That's up from 9.7% on 4.7% a week ago. So far, 78% of S&P 500 companies reporting have posted earnings beats while 60% have reported revenue beats.

Interestingly, earnings growth projections for the third quarter have been coming in rapidly... from 8.1% to 7.4% to 6.8% in successive weeks, with revenue growth stuck at 5%. For the full year, projections are for earnings growth of 10.9%, down from 11.2% two weeks ago on revenue growth of 5.1%.

For the second quarter, three sectors are running at 15% earnings growth or greater. Those sectors would be Communication Services (+20.7%), Technology (+17.2%) and Financials (+15%). Thre sectors are running in a state of earnings contraction for the quarter. Those groups would be Energy (-0.8%), Industrials (-2%) and Materials (-10.3%).

The S&P 500 closed out the past week trading at 20.6 times forward-looking earnings, down from 21.2 times a week ago. This remains well above both the five-year average (19.3 times) and the 10-year average (17.9 times) for the index.

The Week Ahead

Earnings, The Fed, and Jobs on Friday.

Corporate... There are far too many high-profile names reporting this week for me to list here. That would probably just annoy you anyway. All you really need to remember is that Advanced Micro Devices AMD and Microsoft MSFT report on Tuesday evening, followed by Lam Research LRCX, Arm Holdings ARM and Meta Platforms META on Wednesday evening. Thursday evening brings both Amazon AMZN and Apple AAPL before Exxon Mobil XOM and Chevron CVX report on Friday morning.

The Fed... The Fed will still be in quiet mode until Wednesday afternoon. At 2 p.m. ET that day, the FOMC will release the policy statement followed by Jerome Powell's dog-and-pony show a half hour later. There are no economic projections being made this time around, so no dot plot. I can see the disappointment in your faces.

Macro... This Friday will be June jobs day. Even though this series has been wildly inaccurate for over a year now and we all know it, somehow, the media will swallow their price and report the numbers as if they were factual and the algorithms that control price discovery in this post-modern humanless marketplace will do their thing.

Economics (All Times Eastern)

10:00 - Dallas Fed Manufacturing Index (July): Expecting -12, Last -15.1.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MCD (3.07), ON (0.92)

After the Close: LSCC (0.24), TLRY (-0.01)

At the time of publication, Guilfoyle was long XLU, AMD, MSFT, AMZN and XOM.