Is This Just the Latest Example of Algorithmic Overshoot?

Let’s get real about South Korea’s wild market swings, a new ADR listing, oil’s decline, the DJIA, and what I’m seeing from the S&P 500.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The headlines will say that, on Wednesday, South Korean investors bought that market on weakness. I might have a different take.

Oh, don’t get me wrong. South Korea’s tech-laden Kospi Index gave up almost 10% on Tuesday and then rallied almost 3.3% on Wednesday. So, yes, South Korean investors did indeed buy the dip that they had created. Samsung Electronics was the star on Wednesday, taking back roughly 9.8% after having lost almost 12% on Tuesday. The other big tech name that lost almost 12% on Tuesday, SK Hynix, only recaptured a rough 1% on Wednesday.

That dip, though. One has to wonder (really, it’s quite obvious) if South Korean investors simply caught an ugly lesson in algorithmic price overshoot. Like in the U.S., algorithmic traders, by design, force overshoot and inefficiency, which in turn creates artificial opportunity.

In the “olden” days of slower, open outcry trading in fractions of dollars, buyers and sellers would meet in real-time at a centralized location. The ongoing, two-sided auction was great at one thing. That thing was price discovery. Volatility was suppressed by the fact that buyers and sellers knew where to reach out to find someone on the other side of any given trade idea and both sides had time to react.

This differs from the modern model greatly where the whole idea is to use momentum to push prices as far as possible before those on the other side can react. Algorithms are built to trade in microseconds because milliseconds are just too darned slow (true story) and will actually read each other and race each other through the pipes to the various and fractured points of sale. Never mind the fact that when humans and dinosaurs ruled the earth that reading someone else’s order was considered a rules violation and was punishable with a ban; in the algorithmic, electronic era, everything is just okay.

I am long over the replacement of humans by algorithms across U.S. and global equity markets. I had to adapt and adapt is what I did quite well. Knowing one’s levels and existing in a disciplined world is how one defeats the algos. We cannot beat those algos on speed, so we have to be where we want to be before said algos get there. Algorithms are written by humans and humans read the charts, providing technical analysis to those writers. Being as smart and even smarter than them is difficult but not impossible.

That said, the current market model for the U.S. exchanges is far less fair to those who might be less sophisticated or maybe are not especially talented in the field of mathematics than it used to be.

Someone has to say it out loud or write it. Mom and Pop are not going to get help from the large investment banks or from their brokers. The “big boys” were in on the changes that impacted the way assets trade. The move towards some kind of happy medium, because we’re never going all the way back, is going to have to develop at the grass-roots level. Unfortunately, Mom and Pop, unless they grew up in this industry, just see lower commissions and have no idea that they are being taken to school at the point of execution by the very people they trust.

More Memory

My Memory/Storage basket, which was absolutely shredded on Tuesday, is about to grow. This morning, SK Hynix, which is a large-cap memory chip maker, and was mentioned above, filed its intentions with the SEC to list ADRs (American Depositary Receipts) at the Nasdaq Market Site, raising as much as $29.4 billion in doing so. This offering will be led by Bank of America (BAC), Citigroup (C), Goldman Sachs (GS) and JPMorgan Chase (JPM).

The ADRs are currently expected to trade freely here in the U.S. by July 10. SK Hynix is one of the world’s leading HBM (high bandwidth memory) suppliers and is a direct competitor to Micron Technologies (MU) on the global stage. Micron, by the way, will report its quarterly results this evening.

Oil Continues to Fall

Overnight, I have seen front-month WTI Crude futures trade well below $72 per barrel. The “sweet stuff” is now trading at its lowest market prices since very early March. The International benchmark, Brent Crude, is now trading closer to $75 per barrel than it is $76 and is now changing hands at its lowest price since February.

These prices have continued to fall of late as it is estimated that despite rumors of closures, roughly 19 million barrels of oil are moving through the Strait of Hormuz per day. That’s just below the pre-war average of less than 21 million barrels. Yes, it is believed that Iranian oil, which is being sold freely for U.S. dollars, makes up more than 5 million of these barrels. Still, prices for oil continue to fall rapidly.

Though prices at the pump for gasoline have come in as well, they are not coming in fast enough for President Trump. The president posted to social media, “The big Oil Companies are not dropping their price at the pump commensurate with the sharply lower prices they are paying for Oil. Those prices are dropping like a rock!” The president went on… “In other words, customers are being “gouged.” I have instructed the DOJ to immediately start looking into this. Gasoline prices better start going down a lot faster than what I’m seeing!”

Tuesday’s Child

Full of grace? Uhm, no. As bad as it seemed? Well, for tech, certainly. At least Treasury yields continued to come down.

At the index level, Tuesday was ugly for U.S. markets as capital rotated away from the semis, memory and AI with a vengeance. The S&P 500 lost 1.44% for the day, while the Nasdaq Composite surrendered 2.21%. The Nasdaq 100, which had escaped without much damage on Monday, was taken out to the woodshed for a drubbing of 3.29% on Tuesday.

That was, for the most part, due to a 7.87% beating suffered by the Philadelphia Semiconductor Index. Leading the beat-down across he semis were Sarge-folio darlings SanDisk (SNDK) and Micron. ON Semiconductor (ON) and Arm Holdings (ARM) were also pummeled. As mentioned in this column twenty-four hours ago, I did use the weakness to bring Western Digital (WDC) back up to strength and to increase the size of my position in Advanced Micro Devices (AMD).

Getting out into the weeds, all of the small-to mid-cap indices gave up between 0.36% and 1.04% while the Dow Transports gave back 0.75%. The KBW Banks, however, closed out the day in the green, gaining 0.65%, making them one of the few non-defensive bright spots.

Breadth

Again, for the second straight day on Tuesday, breadth was not nearly as weak as performance across the headline indexes had implied. Seven of the 11 S&P sector SPDR ETFs managed to close out the day’s regular session in the win column. Admittedly, the four defensive sectors, led by the Staples (XLP) took the top four slots on the daily tables. That’s definitely not positive. Technology (XLK) was pasted for a 4.14% loss, but that was all on the semis. The Dow Jones U.S. Software Index posted a gain of 0.8% for the day.

Was Tuesday heavy enough to declare a “Day One” bearish reversal of trend? Not even close. Even after two days of headline losses? Read my lips (even though this is print) … so far this is an aggressive rotation. The markets are not crying out in panic. Winners beat losers on Tuesday by a small margin at the NYSE. I repeat, winners beat losers at the NYSE. Losers beat winners at the Nasdaq, but by a 5 to 4 margin, not so decisively.

Advancing volume took a 46.7% share (not the end of the world) of composite NYSE-listed trade and an impressive 67.8% share (wait, what?) of composite Nasdaq-listed activity. Aggregate trading volume was admittedly higher day over day across the Nasdaq, but also sharply lower across the NYSE and sharply lower across the membership of the S&P 500. Those trying to find overwhelming bearish technicals, at least so far, are making things up.

Do You See What I See?

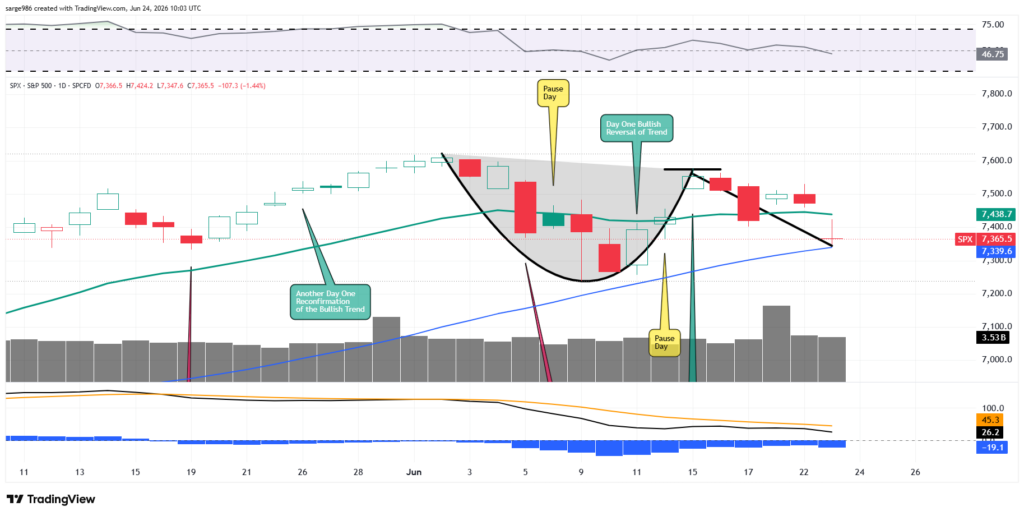

The S&P 500 found support at its 50-day simple moving average (SMA) on Tuesday. That means to me that professional managers were looking to add to their long positions on Tuesday at technically sound levels. The swing traders were lost at the 21-day exponential moving average (EMA) and that’s what provided the opportunity. Am I sure of anything? Of course not. I’m also not a wimp, so I play the game to the best of my ability.

Should that test of the 50-day SMA hold, we probably do have that mini-cup-with-handle pattern that I have been talking about for the S&P 500. The pivot for the pattern is the recent high of 7578 (right side apex of the cup). Retaking that pivot would open the door to levels as high as 9400 over a medium to longer-term time frame.

Nobody Cares/What Matters

In a press release on Tuesday afternoon, S&P Dow Jones Indices announced that Alphabet (GOOGL) will move into the Dow Industrial Average on June 29. Verizon (VZ) will be exiting that once prestigious index. Almost no professional money tracks the Dow Industrials

and nobody cares. This index continues to dominate TV screens because the financial media assumes that viewers are too unsophisticated to adapt. Psst… this index has not been considered important by the pros since the early 1990s.

More importantly, also on June 29, the Honeywell Aerospace (HONAV) spinoff from Honeywell (HON), will begin trading regular way (it’s currently trading as a “when issued”) under the symbol HONA and will immediately be added to the S&P 500. HONA will replace Conagra Brands (CAG) as a member of that highly tracked and truly prestigious index.

Be There or Be Square

For those who for some strange reason have an interest (besides seeing my handsome face), I have returned to financial TV, at least for a bit. We’ll see. I appeared with Charles Payne at Fox Business last week and with Marley Kayden at the Schwab Network on Monday.

This afternoon, I am booked to again appear with Charles (I really, really like that dude) on his FBN show (2pm – 3pm ET). Micron earnings tonight. Rock on.

Economics (All Times Eastern)

07:00 – MBA 30 Year Mortgage Rate (Weekly): Last 6.6%.

07:00 – MBA Mortgage Applications (Weekly): Last -3.8% w/w.

10:00 – New Home Sales (May): Expecting 639K, Last 622K SAAR.

10:30 – Oil Inventories (Weekly): Last -8.262M.

10:30 – Gasoline Stocks (Weekly): Last -906K.

The Fed (All Times Eastern)

16:00 – Bank Stress Test Results.

Today’s Earnings Highlights (Consensus EPS Expectations)

Before the Open: PAYX (1.31)

After the Close: JEF (1.24), MU (20.05), TCOM (6.15)

At the time of publication, Guilfoyle was long MU, SNDK, WDC and AMD equity.