Handle With Care

You say the market doesn't care about oil and interest rates? It's not that simple and might be more about market structure.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A few weeks ago the most common question I had in my inbox was something like, "How can the market be up so much when oil is so high and interest rates are so high?" At the time I explained that stocks cared and I highlighted how the banks and industrials and all sorts of other groups were reacting as they ought to. It was that semiconductors and tech in general was not, and therefore the indexes were staying up there.

And what has transpired in those weeks? Before Tuesday’s rally the banks were down 5%. The industrials remain below their peak high and Tuesday we looked at the potential head-and-shoulders top in the retailers. They cared.

Then came Tuesday with the high inflation print and the question once again littered my inbox. Again let me report that the "market" is being whipped around by the tech stocks and the semis in particular. I mean when one group is about 20% of the index, the discussion should be about that group if you want to discuss the index, shouldn’t it?

Maybe the question should be about market structure, not why the S&P 500 doesn’t care. But let me take on the "market doesn’t care" commentary.

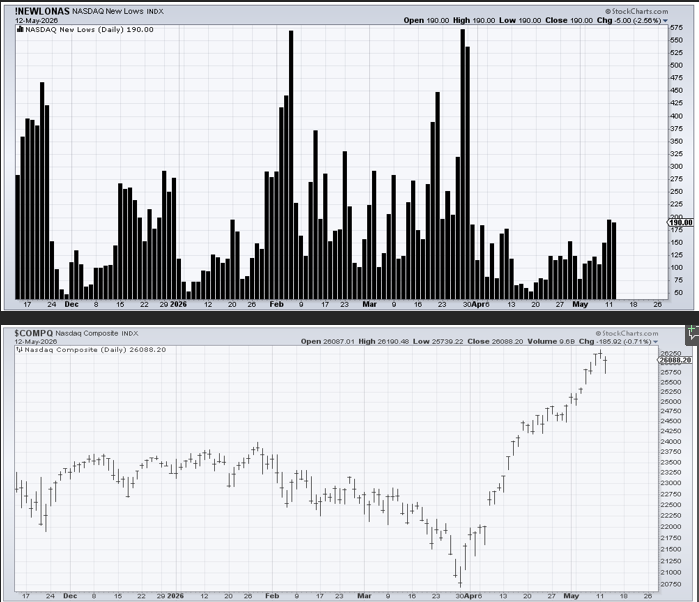

We all know that there are times when the market is down and things are getting better, improving and the market "doesn’t care." Look at early February. The number of stocks making new lows soared to 575, which was pretty much the peak reading for new lows. The Nasdaq (lower chart) was barely down. But then the Nasdaq kept creeping lower, accelerating in March. But the new lows? They kept contracting. The selling was drying up.

That last whoosh down couldn’t really get an increase in new lows, but the point is that the Nasdaq index kept creeping lower but most stocks were already making higher lows in the month of March. It takes time for the indicators to work their way into the market. We all want it to happen instantaneously, but it doesn’t really work that way.

So when I tell you to notice that for the second straight day the Nasdaq’s new lows hovered in the 200 area that doesn’t mean I expect the market to care tomorrow. It may, but often it doesn’t. And when I tell you that not just the Nasdaq but the NYSE had more new lows than new highs on Tuesday, I’d like you to think about that.

Does it sound healthy that a market just pennies off the high has more stocks on the new low list than the new high list? It doesn’t to me.

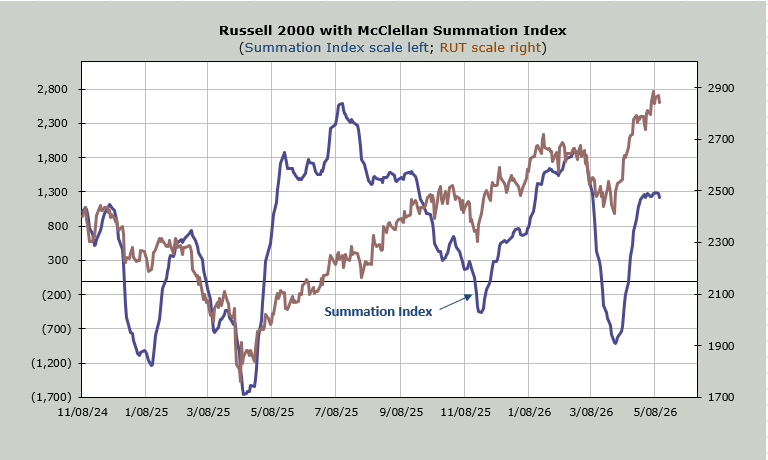

I mean the McClellan Summation Index remains stalled. It has not yet rolled over. We should wait to see if that happens. That would signal there is a change.

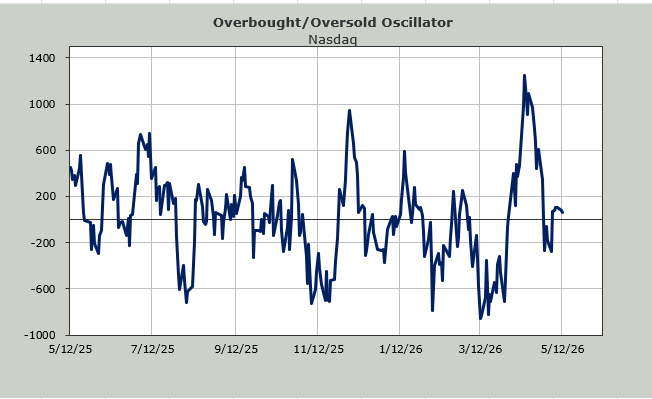

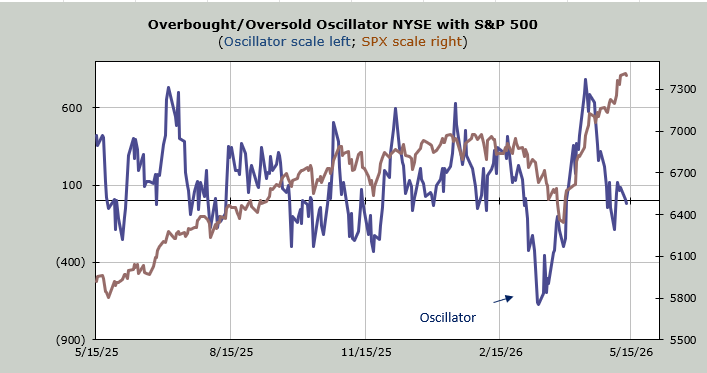

I still expect us to have more volatility in the next few weeks — no matter what occurs on Wednesday or even Thursday — because the intermediate-term indicators are overbought and when they are overbought it is a lot easier to shake things up.

One day does not make a market even though the selling dried up a few hours after the market opened Tuesday. Maybe that will be that with the selling, but I can tell you individual stocks care about oil and rates.