Adding 2 Aerospace Plays to the Bullpen

One is focused on commercial aircraft deliveries, the other on LEO satellite launches.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following Monday’s removal of Qualcomm (QCOM) shares from the Bullpen (and, by the way, those shares are down double-digits on Tuesday), we are adding two new contenders to the Bullpen.

One of them you’ve likely heard of before, and the other was a podcast guest from a few months back: Boeing (BA) and Starfighters Space (FJET).

Let’s break it down.

Boeing

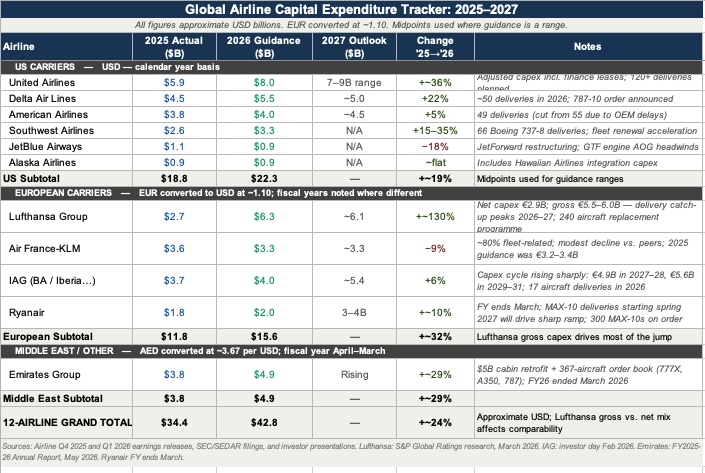

We are adding Boeing shares to the Bullpen due to the expected increase in airline capital spending on new aircraft, which has lifted Boeing’s backlog level to a record near $700 billion that spans over 6,100 commercial airplanes. That reflects airline capital spending that is expected to rise nearly 20% this year across the six major U.S. airlines and closer to 25% when we factor in key international airlines. The airlines are primarily driven by the economic necessity to reduce operating costs—specifically fuel consumption and maintenance expenses, as well as rising global passenger traffic.

To frame that, Boeing’s Commercial Airplanes segment (41% of Q1 2026 revenue) delivered 143 aircraft in the most recent quarter, up from 130 in Q1 2025. During the company’s earnings call, management indicated that production for the 737 aircraft would climb to 47 per month this summer from 42 during Q1 2026 and that its 787 program would rise to 10 per month later this year, up from the current eight per month.

Quickly, Boeing’s two other segments are Defense, Space & Security (34% of Q1 2026 sales) and Global Services (25% of Q1 2026). The Defense, Space & Security segment focuses on manned and unmanned military aircraft and weapons systems, and exiting Q1 2026, its backlog stood at $86 billion. And the defense demand environment spilled over to the Global Services business, which services both commercial and defense customers. Backlog for that segment stood at $33 billion exiting the latest quarter, up from $30 billion exiting 2025. Program wins that led to that increase included Boeing Defense U.K.’s largest ever maintenance and support contract for the U.K.’s Rotary Wing Enterprise and the largest Landing Gear Exchange contract in Boeing’s history with Singapore Airlines.

As we do our homework on BA shares, three items that will be in our focus are backlog levels, margins and production levels. Production levels are expected to move higher during the year, which bodes well for revenue and margins. In Q1 2026, the Commercial Aircraft segment posted an operating loss which, when balanced against the operating profit generated by the other two segments, resulted in a total company operating margin closer to 2.0%. That compares to the 9% to 10% operating margins posted in 2017 to 2018. If Boeing can get on a flight path back toward those figures, that would drop a lot to its bottom line.

One concern we have is something we touched on in Tuesday’s opening comments: higher for longer oil prices and the impact on jet fuel prices, and in turn, airline profitability. We are seeing some airlines adjust fleet plans, including United Airlines (UAL) and American Airlines (AAL), reducing deliveries, while Delta Air Lines (DAL) pushed out some 737 Max 10 deliveries into 2027.

As jet fuel prices remain a potential headwind to airlines, we’ll monitor airline announcements pertaining to new aircraft. We’ll also keep an eye on BA shares, which climbed a swift 26% off their March low, a quicker rate of ascent compared to the S&P 500’s gain of just over 16% over the same time frame. From a chart perspective, we see multiple layers of support for BA shares between $217 to $225, with stronger support between $217 to $220.

Starfighters Space

This is a bit of an anomaly for us, for Starfighters is a pre-revenue company, but near $5 per share, it’s also more like a call option on the low earth orbit (LEO) satellite market. That market involves the launch of small, low-latency satellites at altitudes below 1,000 kilometers for high-speed internet, Earth observation and communications services. We’ve talked about this recently with regard to Amazon’s (AMZN) Amazon LEO initiative and its pending acquisition of GlobalStar (GSAT).

The advantage that Starfighters has is in its active fleet of seven F-104 Starfighters aircraft, which makes it the only company with the capability to fly at Mach 2 while launching payloads into space. What Starfighters looks to bring to the LEO party is lower cost per launch, potentially as much as 10x cheaper compared to traditional rocket launches, the ability to carry smaller payloads, and quicker turnaround times compared to traditional rockets like those from SpaceX, Blue Origin and others.

The Starfighters fleet could act as horizontally launched, piloted vehicles capable of acting as a first stage in launching smaller payloads into space. To that end, the Company is developing a second-stage rocket, StarLaunch I, capable of carrying smaller payloads into space. As part of that effort, it has partnered with GE Aeronautics to develop a prototype StarLaunch I, a proprietary air-launch rocket capable of carrying small payloads into space.

As Starfighters works on that effort, it has also partnered with the U.S. Air Force Research Lab to provide supersonic flight testing for hypersonic and aerospace technologies. Interesting and something that may keep the lights on, but some something that is going to serve as a major catalyst for the shares.

When it comes to FJET shares, the key, in our view, will be the company securing LEO satellite launch program wins. The question we have is whether it has enough capital on hand to sustain itself until that time, and if not, it means another capital raise would be necessary. At the end of 2025, Starfighters had about $20 million in cash and short-term investments on hand, but its operating expenses for that year totaled more than $15 million. We’ll look to see what the company has to say about 2026 expenses, program win timing, and capital needs when it reports its Q1 2026 results.

Here’s the thing: Until we have a more defined timeline for program wins and corresponding revenue, we’re likely to keep FJET shares in the Bullpen. We could see the shares get pulled higher as enthusiasm for the SpaceX IPO builds, and that could be fodder for investors with large risk appetites. While we find the multi-year opportunity interesting, we’ll remain disciplined investors until we the stars are in better alignment.

More Pro Portfolio

- Picking Up More Shares of This AI Holding After Selloff

- Tracking 25 Signals Across 9 of Our Investing Themes

- Weekly Roundup: New Highs, Extreme Greed, and Overbought Risk

At the time of publication, TheStreet Pro Portfolio was long AMZN shares.