Fed Day on Steroids, Dot Plot, CPI, Apple Breakout, S&P Performance Gap

Are you ready? The CPI is important, but it's an ingredient. An important ingredient, but still, it's the stuffing. The Fed's projection for the Fed Funds Rate is Thanksgiving dinner.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There you stood, a distant memory

So good, like we never parted

Said to myself I knew you'd set me free

And here we are, right back where we started

Something's come over me

And I don't know what to feel

Maybe this fantasy is real

Now I know I see what I want it to be

But it's still a mystery

- "Street of Dreams" Turner, Blackmore (Rainbow), 1983

On Second Thought...

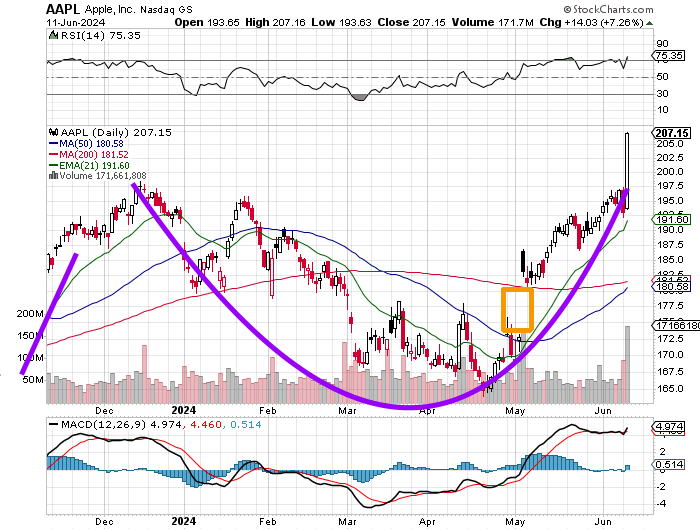

It was no mirage. On Monday, Apple AAPL stock sold off 1.91% in response to the company's revelation of a deal with Microsoft MSFT backed OpenAI to integrate the ChatGPT AI chatbot into Siri and into its consumer devices. What changed? Not much. However, on day two of the week-long WWDC conference in Cupertino, California, investors rethought that selloff, and bought AAPL. They bought AAPL on the open, during the day and into the close as the stock soared 7.26% for the session.

The stock went out at an all-time high of $207.15 on Tuesday afternoon, adding $215 billion to its market cap. This put Apple's market cap at $3.176 trillion, not only retaking second place among public U.S. corporations, leaving Nvidia NVDA in the dust at $2.974 trillion, but closing just short of retaking the stop spot from Microsoft. As of Tuesday afternoon's closing, bell, Microsoft held a market cap of $3.215 trillion.

Remember, that cup pattern that we showed you on Monday with that $199 pivot? Yeah... breakout!

Apple shares have broken out from that cup pattern without (or without yet) developing a handle. This puts the stock's target price at the $238 level that we spoke about on Monday with Relative Strength poking its head above 70, with the daily Moving Average Convergence Divergence (MACD) setting up more bullishly than it had been in a month, and with the 50-day simple moving average (SMA) coming much closer to executing a "golden" crossover of the stock's 200-day SMA.

Huzzah!

Marketplace

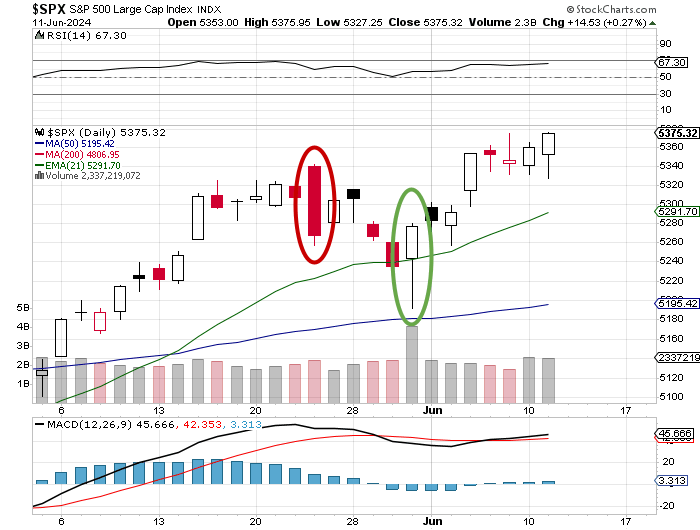

Apple supported both the S&P 500 and Nasdaq Composite, as both of those headline level equity market indexes closed at all-time records (again). The S&P 500 gained just 0.27% for the regular session on Tuesday as the Nasdaq Composite popped for 0.88%.

The rest of the market was not so strong, however. All of your small-to mid-cap indexes closed in the red as did the Dow Transports. The banks took another beating as well. That group has been under considerable pressure of late as more and more light is being shed upon delinquency rates for commercial real estate loans, which are at multi-year highs and also on performance for consumer loans, where delinquency is at its highest level since 2020.

Despite the fact that the headline-level equity indexes both closed in the green, nine of the 11 S&P sector SPDR ETFs closed in the red, led lower by those Financials XLF that gave up 1.23%. Technology XLK was your obvious upside leader at +1.85% as the Dow Jones U.S. Computer Hardware Index (which includes AAPL) gained 6.63%.

Breadth was mixed for the session. Losers beat winners by roughly 5 to 3 at the NYSE and by a narrow 7-to-6 margin at the Nasdaq. Advancing volume took just a 35.3% share of composite NYSE-listed trade, but a 52.4% share of composite Nasdaq-listed trade as aggregate trading volume dropped off for names listed at both exchanges on day over day basis.

Interesting

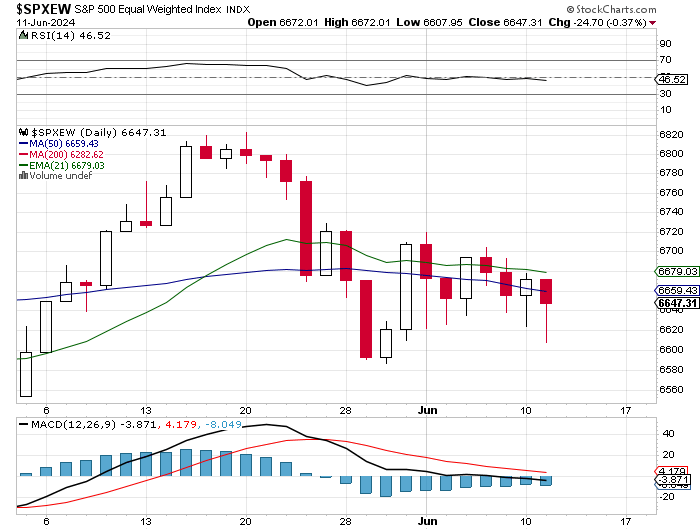

I showed readers this yesterday. I think we really need to drive this home. As the S&P 500 has been closing at record highs on what seems like a daily basis, the equal-weight S&P 500 is nowhere near doing so, as the gap between the two has been exacerbated, especially since the start of June.

Check out the performance gap between the two:

Up, up and away.... in my beautiful balloon for the S&P 500.

More like "Anchors aweigh" for the equal-weight S&P 500. Look at the difference, not only in the daily performance and the now month-long downtrend for the "equal weight" version of the index, but also the difference between the Relative Strength Index (RSI) and daily MACDs. This truly illustrates just how different this most recent leg of the equity market rally has really been.

The chart above shows what the two look like when laid over one another. Interesting. Very interesting.

Are You Ready?

It's May CPI Day, gang. No, wait, it's also Fed Day. Not just a regular Fed Day, but a Fed Day on steroids, meaning that in addition to a policy statement and a press conference, we'll get an update on the FOMC's economic projections. They do this quarterly, and the most famous part of these projections is the now infamous "dot plot" that will give the public an idea of what the committee is thinking, at least at the median, as far as the year-end target for the Fed Funds Rate is.

That's what really matters as far as today is concerned. Yes, the CPI is just as important, but it's an ingredient. Maybe one of the most important ingredients, but still, it's the stuffing. The Fed's projection for the Fed Funds Rate is Thanksgiving dinner.

Stocks Matter

-- Oracle ORCL popped overnight as less-than-spectacular fiscal fourth-quarter performance was overshadowed by upbeat guidance, growth in remaining performance obligation and the announcement of a new partnership with Alphabet (GOOGL) where Oracle Cloud infrastructure will be able to work with technology from the Google Cloud.

-- Paramount Global PARA fell off of a cliff late Tuesday afternoon as reports circulated that Shari Redstone had called off discussions with Skydance Media about a possible merge or deal.

Policy Matters

-- Reports are also making the rounds that G-7 leadership will soon announce a plan to unlock the value of frozen Russian assets in order to pass on that value as aid to Ukraine. The numbers being spoken about are probably in the $50B neighborhood.

-- Bloomberg News is reporting that the U.S. is considering the imposition of additional restrictions on China's access to high-end chip technology that can be used for generative AI purposes. The Bureau of Industry and Security, which is within the Department of Commerce, has recently sent a draft of rule changes to a technical advisory panel.

Treasuries Really Matter

-- On Tuesday, the U.S. Treasury Department auctioned off $39B worth of new 10-Year Notes with strong results one day ahead of the Fed. The high yield awarded came to 4.438%, stopping through the "when issued" by a whopping two basis points at the time. Bid to cover was strong (2.67), as were the internals. Indirect Bidders (foreign accounts) took down 74.5% of the auction, with Direct Bidders (domestic accounts) taking home just 13.8%. That number for the home team was kind of light, but the strong demand from abroad left dealers holding just 11.6% of the issuance, which is the lowest percentage that this group was stuck with since last August.

All of the above matters, at least until 08:30 ET this (Wednesday) morning. Then, the CPI will matter until 14:00 ET. After that, only Jerome Powell will matter. How will markets perform? I would expect an eerie quiet until this afternoon. Then the keyword-reading algos will take over. Then, probably some misdirection and some mayhem.

Stay alert. Stay ready, and to quote the best-known floor trader of them all.... Arthur Cashin... "Stay Nimble, my friend."

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 7.07%.

07:00 - MBA Mortgage Applications (Weekly): Last -5.2% w/w.

08:30 - CPI (May): Expecting 0.1% m/m, Last 0.3% m/m.

08:30 - Core CPI (May): Expecting 0.3% m/m, Last 0.3% m/m.

08:30 - CPI (May): Expecting 3.4% y/y, Last 3.4% y/y.

08:30 - Core CPI (May): Expecting 3.5% y/y, Last 3.6% y/y.

10:30 - Oil Inventories (Weekly): Last +1.223M.

10:30 - Gasoline Stocks (Weekly): Last +2.102M.

The Fed (All Times Eastern)

14:00 - FOMC Policy Decision.14:00 - FOMC Economic Projections.

14:30 - FOMC Press Conference.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: AVGO (10.84), PLAY (1.72)

At the time of publication, Guilfoyle was long AAPL, MSFT and NVDA equity.