Traders Anticipate Apple, Microsoft Deal This Week

Apple is holding its Worldwide Developers Conference this week with one analyst calling it the company's "most important event in a decade."

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The day has come, or should I say the week? Apple AAPL, the second- or third-largest public U.S. corporation depending on the moment, but still the greatest consumer electronic company of all-time, will hold its annual Worldwide Developers Conference (WWDC) this week and the event does indeed run the length of the five-day workweek.

The event has been very much hyped in financial and technical circles. but not by Apple. Apple has been rather quiet even as the stock has not, running from a low of $146.07 in mid-April to $196.89, which is where it closed on Friday. That's almost a 35% run in six weeks or so.

A lot of traders had sold the shares earlier in the year when it was clearly mired in a weakening trend, only to pile back once the worm had turned. I am one of those traders. I did not do a great job on executing my re-entry. I am only up 9% on this tranche, not anything close to the 34% that perfect timing would have allowed.

Great Expectations

I have always liked Charles Dickens. I really do not waste my time with fiction, but Dickens I will always make an exception for. That said, Dickens has nothing to do with Apple, but Apple too has had great expectations placed upon this week's events.

Wall Street is looking for AI this and AI that, all while CEO Tim Cook has probably been the most close-lipped of all of the elite-level tech CEOs when it comes to making announcements or pronouncements concerning the integration of generative artificial intelligence into the software and, in Apple's case, into the software that's already inside of the hardware.

While we all look to hear a little something about an AI-infused iOS for iPhone, an artificially-intelligent version of Siri, smarter Macs and smarter iPods, the number-one thing that traders and investors are looking for is potentially a deal between Apple and the Microsoft- MSFT backed OpenAI to provide something along the lines of that firm's artificially-intelligent ChatGPT chatbot for Apple's mobile consumer products. You see a deal like that, and I think trader and algos alike may just celebrate without considering the expense side or potential for margin compression even if the improved product helps the firm move more merchandise.

Wall Street

Well-known sell-side analyst Dan Ives of Wedbush wrote on the matter over the weekend. Ives' fans might be dismayed to learn that the analyst has recently been downgraded from five stars to four by TipRanks. But that's still what I refer to as "highly rated." Ives reiterated an "outperform" rating (buy-equivalent) on AAPL over the weekend with a $275 target price.

The analyst's optimistic stance is based on the potential for generative AI to act as a catalyst for Apple across many hardware and services ecosystem fronts.

"In our view, WWDC represents the most important event for Apple in over a decade as the pressure to bring a generative AI stack of technology for developers and consumers is front and center," Ives wrote.

Ives then went in deeper: "We expect the formal announcement of a flagship OpenAI partnership will consist of an OpenAI Chatbot with exclusive features that take advantage of Apple's con-device large language models as well as cloud-powered ones."

Brian White, a five-star rated analyst with Moness, Crespi, Hardt & Co., was also complimentary. While, who rates AAPL as a "buy" with a $205 target, wrote last week that "Apple chose wisely not to participate in the gen-AI propaganda campaign. We believe this discipline and foresight has served the company well."

Earnings and Fundamentals

Readers are reminded that Apple reported the firm's fiscal second quarter earnings back on May 2, 2024. The firm beat the street with top- and bottom-line results that exceeded expectations despite a 4.3% contraction in sales on a year-over-year basis. The firm increased the dividend at that time, while beefing up its authorization for share repurchases to $110 billion.

Free cash flow for the quarter printed at more than $20 billion and more than $100 billion for the trailing 12 months at that time. The balance sheet remained healthy with a cash position of over $162 billion once long-term investments are included as they well could be. Total debt-load came to $104.6 billion, which is mostly long-term and was mostly borrowed at very low interest rates. The firm also has the cash and the cash flows to pay the whole darn thing off tomorrow if need be.

My Thoughts

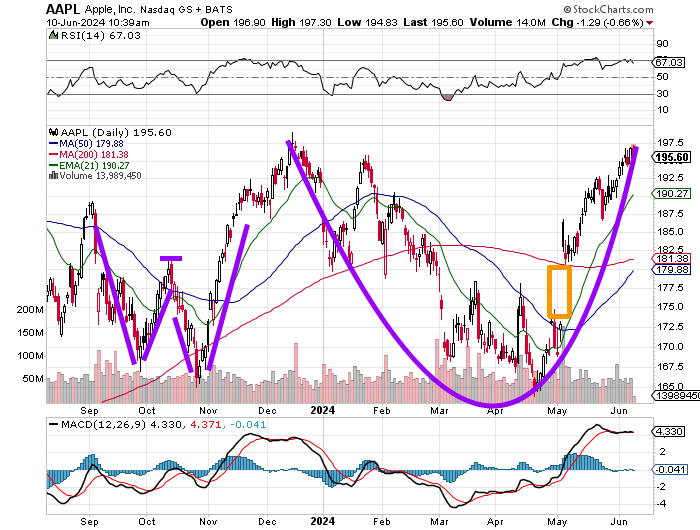

Readers will see that the double-bottom pattern last Autumn worked like a charm. AAPL has now developed a cup pattern with a $199 pivot (right side of the cup), while spotting a nearly overbought RSI and a cautiously bullish daily MACD. For the bears, there is an unfilled gap created in early May that would need a $173 tick to fill.

The stock is probably, in my opinion, at a good place to sell off a bit and add a handle to this cup. That would move the pivot from the left-side apex of the cup to the right-side apex. Right now, we do not know if we have yet seen a right-side apex. Therefore, I consider my current long position a trade with a $238 target based on my current pivot. Should a handle develop, I would look forward to both adding on that dip, creating a larger position and turning my trade into an investment, which is what I wanted originally, before the darned thing took off on me.

Panic? Only on a break of the 200-day SMA ($181), which would be assign that the gap below would likely fill. Should that happen, the idea would be to re-enter near the lower end of that gap. Either a breakout for the cup or the development of a handle would be fine with me. Having to exit and re-enter intelligently upon a harsher sell-off is something I would prefer to avoid.

At the time of publication, Guilfoyle was long AAPL and MSFT equity.