As September Winds Down, Geopolitical Risk Ramps Up

China stocks are up big again as the month comes to an end. Let's also look to the week ahead, including a jobs report, with a spotlight on trading Intel and Lockheed Martin.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There was some concern heading into September this year. The economy appeared to be on shakier ground than had been reported. Or so we thought. There was more than enough geopolitical risk to go around.

Sure, it's a presidential election year in the U.S., and those years tend to treat U.S. markets well, but this is a different kind of election, something like the last two, but nothing like what came before that. We have an election where roughly half of the American public actually thinks poorly of those who they disagree with politically, and regardless of electoral outcome, half of the populace will likely feel cheated in some way.

What could go wrong? What could go right. For starters, back on September 18, the FOMC took an aggressive first step towards much easier monetary policy. The fact that consumer-level inflation in the U.S. has neared, but not reached the Fed's target caused some to wonder why. The risk to the labor market had come into balance with the risk from inflation was all the Fed could come up with.

Then, the Bureau of Economic Analysis shocked the world (OK, maybe not the world, but at least your author) by revising higher basically the past two and a half years worth of growth in GDP.

What really shocked this economist was the absolute gigantic upward revisions to GDI over that time frame. I was right about GDI and GDP needing to be closer together. The fact that GDI was ratcheted (much) higher towards GDP, and not the other way around was for me, a humbling head scratcher. Was I wrong about a weak economy? I still have some doubts, but not admitting having come to an incorrect conclusion would make me nothing more than a sore loser.

So, it would appear so (that I was incorrect), and it is better for our country and our people if I were. That said, maybe we cool it a little on the easing of monetary policy if inflation has not yet been licked and this is really an economy growing at 3%? Just a thought. About that labor market balancing act, I guess we'll know a little more by this Friday.

As for September, going into the final day of trading for the month, the S&P 500 is up 1.59%, and the Nasdaq Composite is up an even nicer 2.29%. Even the Russell 2000, which has struggled more than its larger-cap cousins, is up 0.32% month to date.

The Week That Was

Where do we start? With Chinese economic stimulus perhaps. First there was some stimulus. A couple of days later there was more. Down came reserve requirement ratios and down came interest rates. The buying of equities was facilitated. The real estate market would be the focus of the support, but the support was broad.

The Shanghai Composite and Hang Seng Index rejoiced, as did much of the planet in real time, though to me, while this could spark some demand for the import of certain materials, this seems like a domestic Chinese story. Weakening the home currency ahead of the BRICS meeting in October is interesting as well. Could be something up somebody's sleeve there. While we intentionally debase our own currency, we would be partially to blame if something significant in the way of a changed currency exchange equilibrium arises.

It was a rather light week for U.S. macro, with the exception of August Durable Goods Orders and August Income and Outlays. I find that the PCE rarely either surprises or causes the stir across the marketplace that the CPI can provoke.

The Fed was out in force. Still, nobody has intelligently explained the aggression in the new trajectory for U.S. monetary policy. This does lead me to believe that maybe they know something we don't know and aren't telling. OK, we're going to "recalibrate" our way down to a terminal Fed Funds Rate below 3%. Gotcha. Whether the economy needs it or not. Gotcha. Even if inflation is still high enough to hurt people. I know, gotcha.

Oh, on the geopolitical front, China's focus on its economy could maybe take its focus off of Taiwan for the short-term and that would be a good thing. However, there are enough problem areas still growing. Last week, Russian President Vladimir Putin revealed changes to Russia's nuclear doctrine. What Putin did was lower the "official" or unofficial bar for nuclear "retaliation." What he was doing was warning the U.S. and other NATO powers that have been aiding Ukraine with both funds and military hardware that could potentially be used offensively on Russian soil.

In addition to that, Israel has responded to rocket attacks on the northern part of the country by Hezbollah, from Lebanon, by responding. First it was the exploding pagers and walkie talkies. Then it was actual strikes inside Beirut that killed Hezbollah's leader Hassan Nasrallah. This is likely to cause an angry reaction not only in Lebanon, but also in Iran, which is where funding for both Hezbollah and Hamas as well as other terrorist groups is believed to come from.

Monday Morning

Chinese stocks traded even higher, though the rest of the planet was slow to play along this time. The Shanghai Composite gained more than 8% on Monday on top of a 13% gain last week, while the Hang Seng Index tacked a 3% gain onto last week's 13% run. There is talk (but no new announcement yet) of more stimulus on the way in addition to measures announced last week by the PBOC and fiscal pledges made last week by the politburo.

It appears that Israel's war continued to expand on Sunday into Monday as that nation launched new airstrikes inside of Lebanon as well as on Houthi targets inside of Yemen. Houthi rebels, also funded by Iran, had been launching attacks on Israel in support of both Hamas and Hezbollah.

In a move that some may find alarming, the Pentagon released a statement where (Defense) "Secretary Austin stressed that the United States is determined to prevent Iran and Iranian-backed partners and proxies from exploiting the situation or expanding the conflict." The statement added "The United States retains the capability to deploy forces on short notice."

Marketplace

Last week was quite the week. While gold, silver and Bitcoin pressed higher, and Treasury yields continued to "normalize," the U.S. dollar weakened.

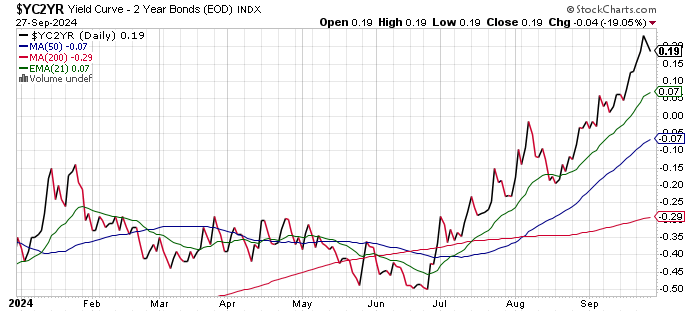

Readers will see that the spread between the yields of the U.S. 2-Year Note and U.S. 10-Year Note continued to expand. This spread went out at +19 basis points on Friday afternoon:

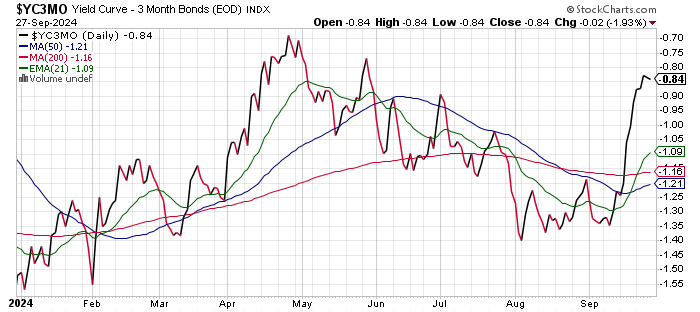

This was good for a gain of six basis points versus last Friday's close. Even the spread between the yields of the 10-Year Note and the 3-Month T-Bill, which has been a stubbornly inverted spread, made some progress:

That spread improved to -84 basis points from -92 basis points in one week's time. It was a generally good week for equities, but not a great one. The S&P 500 did make three new highs last week before going out on a slightly negative note (on reduced trading volume).

- The S&P 500 gave up 0.13% on Friday to close the week up 0.62%.

- The Nasdaq Composite gave up 0.39% on Friday to close the week up 0.95%.

- The Nasdaq 100 gave up 0.53% on Friday to close the week up 1.1%.

- The Russell 2000 gained 0.67% on Friday, but still closed the week down 0.14%.

- The S&P SmallCap 600 gained 0.75% on Friday to close the week up 0.22%.

- The S&P MidCap 400 gained 0.11% on Friday to close the week up 0.51%.

- The Dow Transports gained 0.64% on Friday, to close the week up 2.74%.

- The Philly Semiconductors gave up 1.76% on Friday and still closed the week up 4.34%.

- The KBW Bank Index gained 0.12% on Friday to close the week down 0.94%.

On Friday, eight of the 11 S&P sector SPDR ETFs closed in the green, with Energy XLE way out in front at +2.04%. No other fund among the 11 gained or lost more than 1%.

For the week, seven of the 11 S&P sector SPDR ETFs closed in the green, led by Materials XLB on Chinese stimulus and on the softer U.S. dollar. Overall, cyclicals and "growthy" sectors outperformed defensive sectors for the week.

Last Week's Jump Ball?

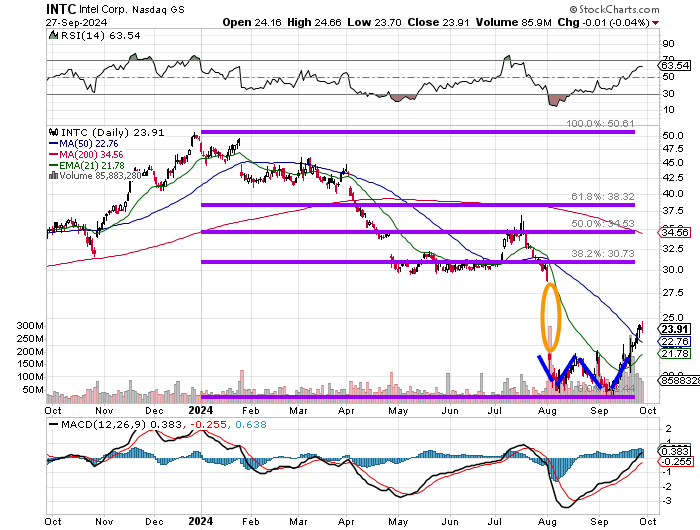

Remember the chart of Intel INTC from last week? We had discussed the deal with Amazon's AMZN AWS, the interest in the company or part of the company shown by Qualcomm QCOM and the potential investment that may have been proposed by Apollo Global Management APO.

I suggested that I was considering getting myself involved and that is what I did. I figured if so many folks think they can run Intel better than it has been running, then maybe one of them will, or maybe Intel will get its act together. The company itself has been talking about splitting the foundry business off into a semi-independent subsidiary and there has also been talk of selling more Mobileye MBLY.

I got in at an average of $22.52 last week. Will I buy more? If the stock dips. The double-bottom reversal pattern we discussed last week provided the fuel and the headlines did the rest.

INTC has now taken back its 50-day SMA (simple moving average), its reading for Relative Strength is much improved and its daily MACD (Moving Average Convergence Divergence) is not where I want it yet, but it is going the right way.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter up to growth of 3.1% (q/q, SAAR) from 2.9%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed trimmed its Q3 estimate by a hair to 2.99%, so they are pretty much in line with Atlanta. The Cleveland Fed, however, took their Q3 estimate down to growth of 1.45% from 1.61%, and the St. Louis Fed took their estimate for the third quarter down to growth of 1.41% from 1.55%, which puts them in line with Cleveland.

Just an FYI, the St. Louis Fed was the most accurate among the four models for the first quarter, while Atlanta was the most accurate for Q2.

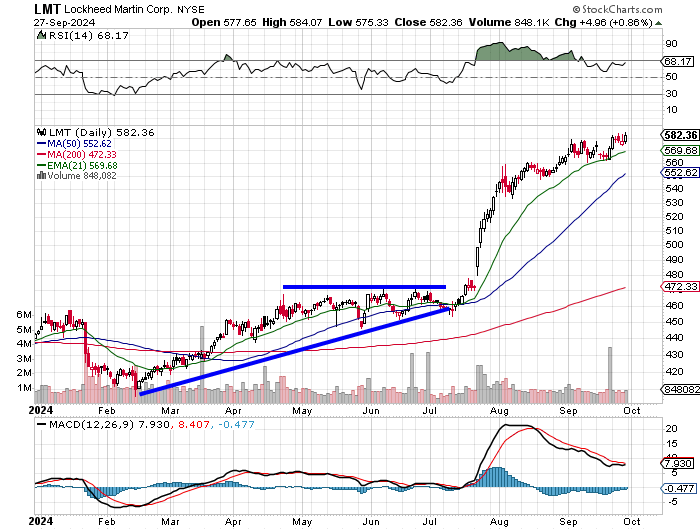

Another Large Contract for Lockheed

On Friday, Lockheed Martin LMT Missile and Fire Control was awarded a $3.23 billion firm-fixed-price, undefinitized contract action for a joint air-to-surface standoff missile and long-range anti-ship missile large lot procurement. Work is expected to be done by July 31, 2032. The contracting agency is the Air Force Life Cycle Management Center, but includes sales to the U.S. Air Force, U.S. Navy and foreign military sales to the forces of Japan, Netherlands, Finland and Poland.

Later, on Friday, Lockheed Missile and Fire Control was awarded a much smaller, but still worth mentioning $358 million firm-fixed-price undefinitized contract action to add to an existing contract for long-range anti-ship missiles. This brings that already existing contract up to $1.146 billion. That work is expected to be completed by July 31, 2028, and also includes unspecified foreign military sales.

Readers may recall that just two weeks ago, the State Department approved the sale of 32 F-35A Joint Strike Fighter Aircraft to the armed forces of Romania (part of NATO) in a deal worth a rough $7.2 billion. There is talk of Romania purchasing another lot of 16 after this deal to make three full squadrons. Deliveries are expected to begin by 2030. The F-35 is manufactured by Lockhed Martin, but spare engines are part of this deal as well. The engines are manufactured by the Pratt & Whitney unit of RTX RTX.

For those also long this name, I expect the shares to develop a basing period of consolidation at this point. Both the RSI (Relative Strength Index) and the daily MACD (Moving Average Convergence Divergence) became overly extended and are "normalizing" and a new technical pattern has not yet formed.

It would not be wrong to take some of this one off at this point and play with more house money than principal, especially as it is impossible to place a new, technically precise price target just yet. I will not be getting out of the name, but I am not planning to add here, at least not until the 50-day and 200-day SMAs (simple moving averages) play a little "catch up" relative to the last sale.

The Week Ahead

It's "jobs week" again, gang. Does anything else matter right now? Outside of the geopolitical and the political, probably not. A soft jobs report helps justify the Fed's current monetary posture. A strong report would push back on the forward-looking pace of short-term interest rate cuts.

Those numbers will be released this Friday. Before we get there, the September ISM Manufacturing and Non-Manufacturing surveys will land on Tuesday and Wednesday.

In addition to the BLS numbers, the ADP Employment Report for September will print on Wednesday. This report has been considered more accurate than the monthly BLS surveys this year by many economists.

Outside of the ISMs and the jobs data, this is not an especially busy week, economically. The Fed will be out in force yet again. I see five speakers on Tuesday and four more on Wednesday. New York Fed President John Williams is even going to speak on Friday morning. Speaking on "jobs day" used to be a big no-no for the Fed. Guess not anymore.

This will be a very light week for earnings releases. Carnival Corp. CCL will report this morning, followed by McCormick MKC and the Nike NKE release that everyone has been waiting for on Tuesday afternoon. After that, it's really just going to be Levi Strauss LEVI and Constellation Brands STZ in the spotlight on Wednesday and Thursday afternoons.

Economics (All Times Eastern)

09:45 - Chicago PMI (Sep): Expecting 46.4, Last 46.1.

10:30 - Dallas Fed Manufacturing Index (Sep): Expecting -4.5, Last -9.7.

The Fed (All Times Eastern)

08:50 - Speaker: Reserve Board Gov. Michelle Bowman.

13:55 - Speaker: Federal Reserve Chair Jerome Powell.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CCL (1.15)

At the time of publication, Guilfoyle was long INTC, AMZN and LMT equity.