Make Your Own Retirement Plan

We cannot stop politicians from breaking their word. The best we can do is prepare for what is expected to unfold. That's where Roth IRAs come into play.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Government programs like Social Security sound terrific until you realize they are enormous unfunded promises which can be reneged on in the future.

That is especially true for readers like you who have likely saved a lot of money over your lifetimes.

Initially, Social Security was touted as something that would never be taxed. That went out the window years ago. Now, up to 85% of benefits paid are subject to federal taxation if you have even a relatively modest income post-retirement. Many states also tack on tax bills on the benefits you receive.

The next steps are likely:

- Bumping up the percentage of benefits taxed to 100% for those with decent later-in-life incomes.

- Means testing to see if you “need” Social Security payments, which less fortunate people cannot live without.

The fact that high earners paid Social Security the most during their working years will eventually be set aside when push comes to shove in the name of “fairness” to those who failed to provide for their own retirements.

We cannot stop politicians from breaking their word. The best we can do is prepare for what is expected to unfold. Roth IRAs are the best investment envelope ever created to allow Americans to secure their own futures without counting on receiving government checks during their post-working years.

Traditional IRAs are OK. But money accumulated in them will be taxed upon withdrawal, and at your highest marginal tax rate. That happens even if the gains made inside them would have qualified for long-term capital-gains treatment if held outside an IRA.

Roths did not exist when I first started my traditional IRA. After they were offered, I started gradually converting my old IRA into Roth status to take advantage of their tax-free forever status. Gains from capital appreciation, dividends and covered option premiums received in a Roth account are tax-free on both unrealized and realized income plus incur no federal tax when ultimately withdrawn.

They also maintain that status if inherited by a spouse. Next-generation inheritors used to be able to stretch Roth withdrawals over their expected lifetimes. That changed not long ago. Now non-spouses must clear out all funds held in an inherited Roth over no more than 10 years from the date of death.

Why did that change happen? Greedy Washington bureaucrats do not like seeing often huge sums going untaxed forever.

That is just another example of how politicians change promises made, after the fact.

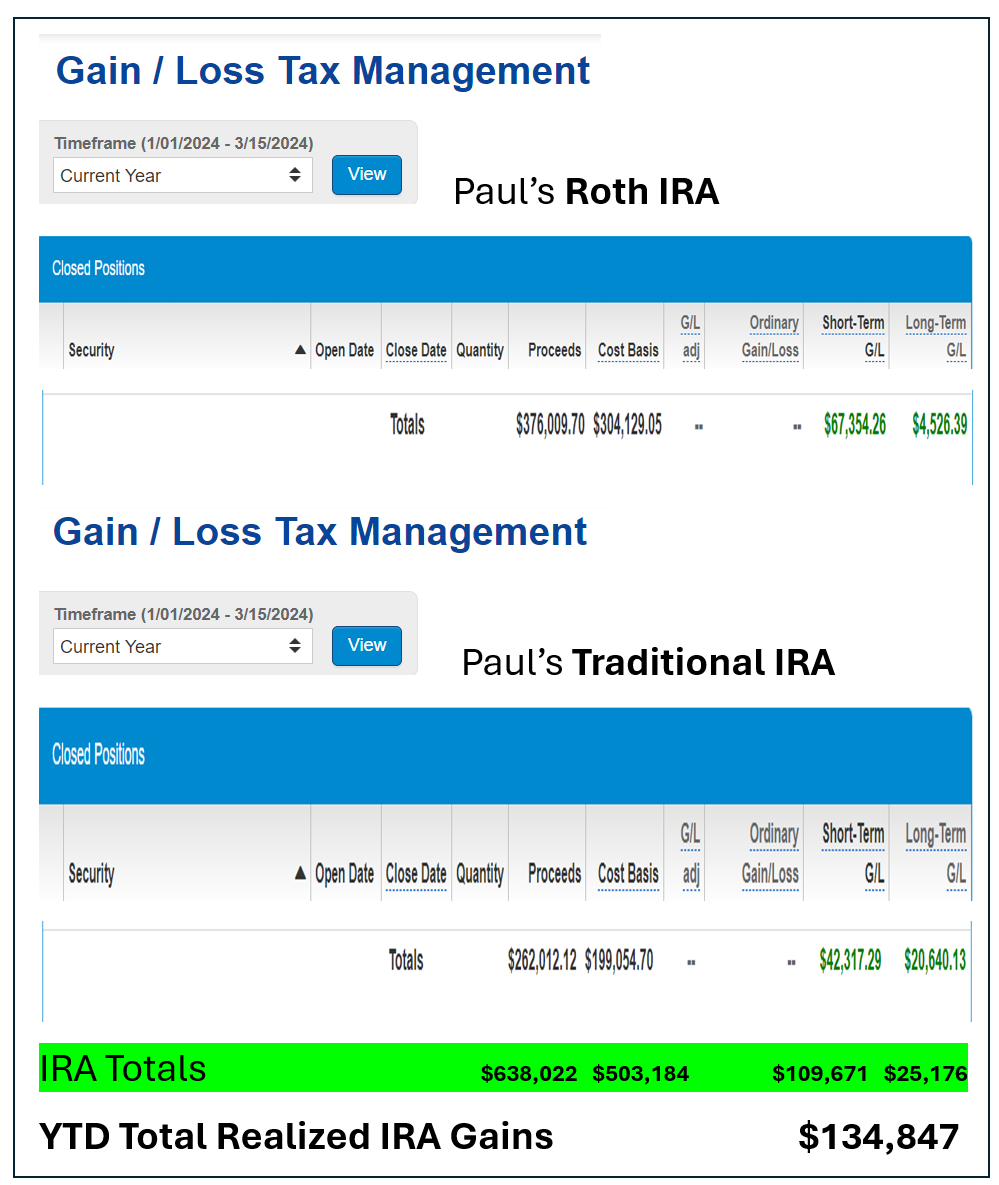

Can you really have a good income during retirement simply on your own IRA assets? You bet you can. The data below show my own realized gains for the year-to-date period period from Jan. 1, 2024 through Mar. 15, 2024.

I generated $71,881 in net gains inside my Roth IRA and an additional $62,957 in my traditional IRA.

The Roth’s profits are more valuable as they remain federally tax-free forever, even after their eventual withdrawal. The $62,957 earned in my traditional IRA are only worth their after-tax value when required minimum distributions (RMDs) force me to remove them from tax-sheltered status.

Future profits through the full-year 2024 are not knowable in advance. If they merely continue to accrue at the YTD rate, though, my full-year gains would annualize at north of $647,000.

Unless I start living a much more lavish lifestyle, that would be more than enough to ensure a financially secure future with, or without my Social Security income.

How did I manage to reach such a nice situation at age 73?

- Deferred gratification during my prime working years.

- Clockwork contributions to my IRA accounts, early in the year they were allowed, not near tax-time of the following year.

- Willingness to suffer through volatility by keeping 100% of my IRA assets in equities from day one right through the present.

Saving regularly by spending less than I earned allowed me to live a debt-free adult life. Funding retirement accounts as early in the year as possible provided the most time for tax-free, or tax-deferred compounding. Avoiding overly conservative asset classes was invaluable to accumulating significant wealth.

Investments in long-term accounts afford the luxury of ignoring often painful market pullbacks in the knowledge that the ultimate buy-and-hold returns dwarf those of cash, bonds, gold, real estate etcetera.

See my earlier article on how various asset classes performed over the long-term and you will understand why I was, and remain, all-in on stocks.

Data shown reflect account YTD numbers for realized gains for the IRAs identified. Source: TradeStation.com.