Tactics

I have used the afternoon rally to scale into more SPY shorts as I suspect some of the first-of-the-month money has been committed.

But still small sized.

Position: Short SPY (S)

BY Doug Kass · Jul 1, 2026, 1:02 PM EDT

I have used the afternoon rally to scale into more SPY shorts as I suspect some of the first-of-the-month money has been committed.

But still small sized.

Position: Short SPY (S)

BY Doug Kass · Jul 1, 2026, 1:02 PM EDT

Position: None

BY Doug Kass · Jul 1, 2026, 12:30 PM EDT

From Peter Boockvar:

I think Bank of Canada Governor Tiff Macklem said it best at the central bank forum on stage with peers Kevin Warsh, Christine Lagarde and Andrew Bailey. “We have to be humble in this time of uncertainty.” In other words, and I think those thoughts are shared by the others, we just have to wait and see how events play out and they won’t commit until they have to.

Specifically on the heels of the ECB rate cut, Lagarde acknowledged they were in a different place than the Fed and BoE with a deposit rate of just 2% and inflation now above that.

With respect to Warsh, he reiterated again that we won’t get any clues as to what he’ll want to do next in terms of policy (which could be different or the same as his colleagues), if anything in the coming meetings. What I’m most interested in but yet to be revealed by him is his views of the concept of the ‘neutral rate.’ Powell’s view was that he’d know what that rate is when he sees it as it is a very econometrically modeled figure. In other words, who really knows what it is. The dot plot has the long term ‘neutral rate’ view at 1% real but does Warsh have a view on that? In the meantime, markets are going to be left very much on its toes without the hand holding of the central bank.

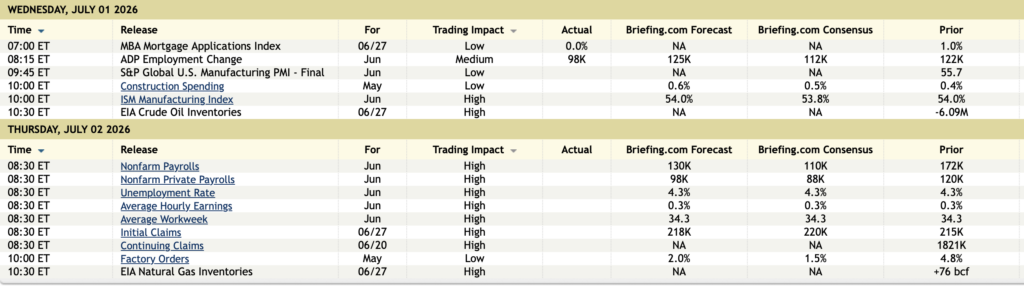

The June ISM manufacturing index fell to 53.3 from 54 and just below the estimate of little change at 53.9. New orders were still good at 56 but down a touch m/o/m. Backlogs were 50.5 vs 52.2. Inventories rose back above 50 at 51.4 for the first time since April 2025.

Likely thanks to the drop in crude prices and other commodities, prices paid fell to 73 from 82.1, though still well above the 59 it was at in January. Supplier deliveries at 57.4 were down 3.2 pts m/o/m, but still elevated. This is what was said on pricing, “The Prices Index reading is still being driven by (1) increases in steel and aluminum prices that impact the entire value chain, (2) tariffs applied to many imported goods and (3) increases in petroleum-based products as a result of the Middle East conflict. Higher prices were reported by 55.1 percent of respondents in June, down 11.2 percentage points from May’s 66.3 percent.”

Employment got closer to 50 at 49.7.

Export orders fell back under 50 at 48.5, down 2.1 pts m/o/m.

Breadth softened a touch with 14 industries of 18 seeing expansion vs 16 in May.

Bottom line, the parts of the US manufacturing sector that are feeding into the GenAI buildout is enjoying the massive spend on it, as we know. Other parts are seeing a more mixed bag but a lift over the past few months as a pull forward of ordering has taken place after the Middle East conflict began. I’m also hearing that ahead of another possible round of tariffs is resulting in more pull forwards.

US Treasuries are little changed in response to both of the above.

Here were the broad respondent comments and reflects hopes but realism with the pace of business activity and the challenges being faced:

BY Doug Kass · Jul 1, 2026, 12:15 PM EDT

One month ago Kimberly-Clark (KMB) traded at $93 and is now nearly $111/share.

I have reduced my weighting to very small.

Position: Long KMB (VS)

BY Doug Kass · Jul 1, 2026, 12:01 PM EDT

Dan Nathan interviews Rosie on his Risk Reversal podcast.

Run, don’t walk to watch this valuable hour-long interview.

Let’s go to the tape!

David Rosenberg: “There Are No More Bears Left” In This Market

Position: None

BY Doug Kass · Jul 1, 2026, 11:55 AM EDT

I put out more SPY shorts at $749.24

Position: SPY (S)

BY Doug Kass · Jul 1, 2026, 11:45 AM EDT

Position: None

BY Doug Kass · Jul 1, 2026, 11:40 AM EDT

The Nasdaq has become “a tale of two cities” with haves and have-nots.

That relationship shifts daily.

As such, it is getting too hard to trade.

For the foreseeable future I will be concentrating on shoring the S&P index.

I am no longer short QQQ.

Position: Short SPY (VS)

BY Doug Kass · Jul 1, 2026, 11:30 AM EDT

With S&P cash +11 handles, I am back shorting SPY at $748.22.

Position: Short SPY (VS)

BY Doug Kass · Jul 1, 2026, 11:25 AM EDT

Another leg lower for momentum, high beta tech (part of my short basket).

I am sticking with the remainder of the basket even though some of the drops have been dramatic:

Today’s Selected Price Changes in Short Basket

* SNDK (SNDK) -$255

* CAT (CAT) -$58

* CRWV (CRWV) -$15

* INTC (INTC) -$11

* MU (MU) -$98

Position: Short Basket

BY Doug Kass · Jul 1, 2026, 11:10 AM EDT

Sometime in the next six months cannabis equities will become meme stocks.

Positions: Long Cannabis

BY Doug Kass · Jul 1, 2026, 10:59 AM EDT

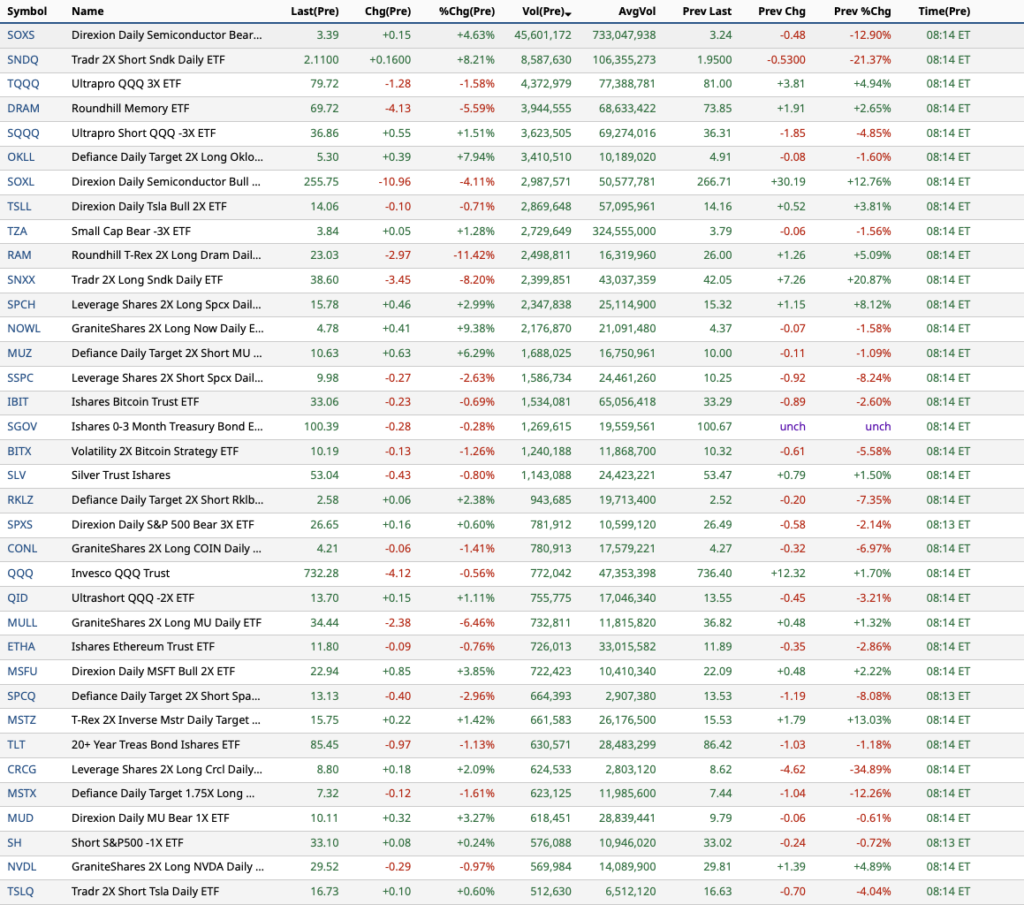

I have 14 longs and 24 shorts in my hedge fund’s portfolio currently.

BY Doug Kass · Jul 1, 2026, 10:45 AM EDT

PPermaUnsure

3m ago

I’ve always found it strange that some people think it’s wrong to identify fundamental problems before they cause harm. If a doctor identifies cancer while it’s at an early stage, people don’t laugh at him and say “you’re early, and early is the same as being wrong.” Instead, the doctor is praised. Identifying the existence of a cancer and predicting the time that the cancer will kill the patient are two completely different things.ReplyShare

none

BY Doug Kass · Jul 1, 2026, 10:20 AM EDT

I covered one half of my high-beta high tech short basket on the whoosh lower in the Nasdaq.

Some of the decline have been dramatic (e.g (CRWV) -10%; (SNDK) (-$200) etc.

I would reshort on strength.

Positions: Short high-tech basket; VS Short SNDK VS CRWV VS

BY Doug Kass · Jul 1, 2026, 9:52 AM EDT

I neglected to mention that I took starter long positions in private equity late yesterday:

* KKR (KKR) $91.85

* BX (BX) $117.15

* APO (APO) $116.96

I plan to reshort banks/brokers as a pair trade with this long.

Positions: Long KKR VS BX VS APO VS

BY Doug Kass · Jul 1, 2026, 9:50 AM EDT

A further conspicuous decline in TLT (TLT) (-$0.77) this morning.

The equity risk premium’s discount is ever widening.

Positions: None.

BY Doug Kass · Jul 1, 2026, 9:35 AM EDT

META (META) is saying that it is building its cloud business to sell excess AI compute.

The Nasdaq and AMZN (AMZN) are moving lower on the headline.

Positions: Long AMZN VS; Short QQQ M

BY Doug Kass · Jul 1, 2026, 9:20 AM EDT

Positions: None.

BY Doug Kass · Jul 1, 2026, 9:13 AM EDT

Positions: None.

BY Doug Kass · Jul 1, 2026, 9:05 AM EDT

I covered most of my index shorts this morning:

* SPY (SPY) $744.47

* QQQ (QQQ) $729.36

I will continue to trade opportunistically until there is a clear downtrend.

I am sticking with my high beta tech basket of shorts – for now.

I plan to reshort on strength – which I expect as inflows start to come in at quarter and month’s beginning.

Positions: Short SPY VS QQQ VS

BY Doug Kass · Jul 1, 2026, 9:04 AM EDT

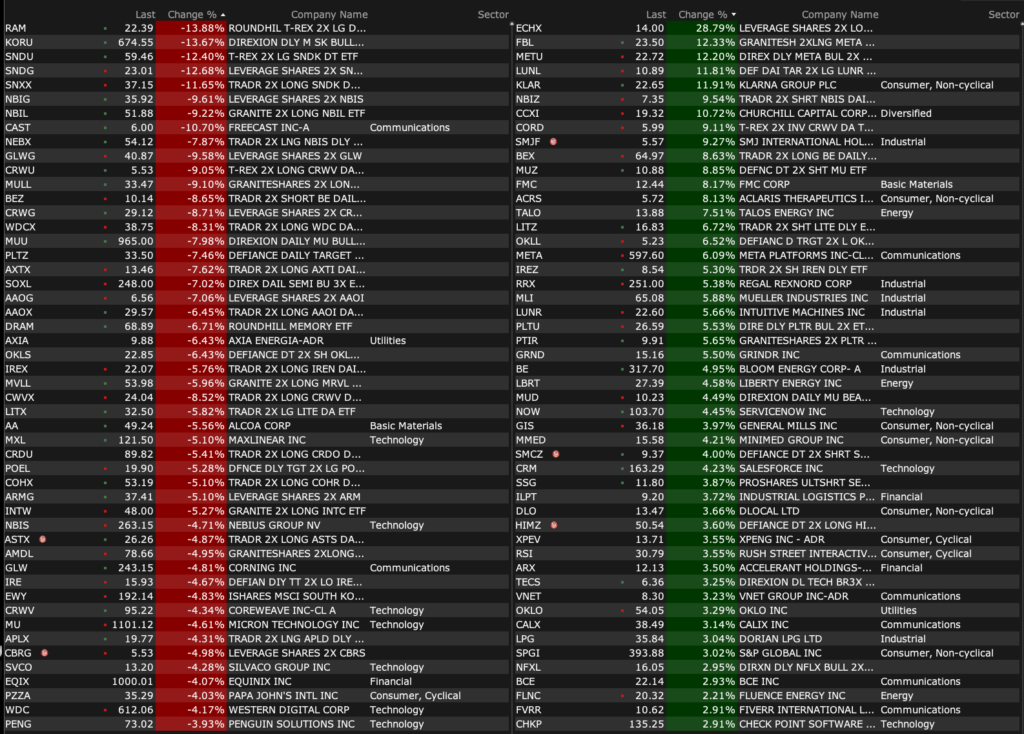

-KLAR +8.4% (Swedish court orders Google to pay SEK14.3B to one of Klarna-owned PriceRunner)

-FMC +8.3% (announces pact for $13.30/share with Tessenderlo Group worth $400M)

-BE +7.9% (expands Brookfield AI infrastructure power project financing framework to $25B from $5B)

-LUNR +6.6% (awarded NASA contract valued up to $148M)

-GRND +6.3% (Morgan Stanley Raised GRND to Overweight from Equal Weight, price target: $18)

-NOW +4.5% (Guggenheim Securities Raised NOW to Buy from Neutral, price target: $125)

-GIS +4.3% (earnings, guidance)

-OKLO +4.1% (receives DOE approval for Groves Isotope Test Reactor Documented Safety Analysis)

-CRM +3.8% (Guggenheim Securities Raised CRM to Buy from Neutral, price target: $228)

-XPEV +3.7% (June deliveries)

-MSM +2.7% (earnings, guidance)

-PLTR +2.5% (momentum)

-SSTK -32% (Getty Images plans to terminate Shutterstock merger after CMA condition requiring sale of Shutterstock editorial business)

-AA -5.4% (South 32 Ltd. divests aluminum value chain assets to Alcoa for up to $5.6B)

-SNDK -4.2% (memory weakness)

-MU -3.3% (memory weakness)

-KR -2.9% (acquires food and pharmacy retailer Giant Eagle for $1.65B)

-NIO -2.4% (June deliveries)

-CAT -2.3% (Burry short mention)

-NKE -2.1% (earnings, guidance)

Positions: None.

BY Doug Kass · Jul 1, 2026, 8:55 AM EDT

Positions: None.

BY Doug Kass · Jul 1, 2026, 8:45 AM EDT

But I caution you all that the roads on Wall Street are paved with geniuses who were right one time in a row:

Positions: None.

BY Doug Kass · Jul 1, 2026, 8:28 AM EDT

Knowledge@Wharton… America at 250 America at 250: Innovations That Transformed Business – Knowledge at Wharton

Positions: None

BY Doug Kass · Jul 1, 2026, 8:04 AM EDT

I received a number of emails from subscribers who don’t understand why I refuse to discuss the constituents of my high-beta tech short basket:

* I am not making investment recommendations — I am simply showing what, in principle I am doing.

* I show my weightings (S, M, L) as an indication of my confidence level, among other factors. It also reflects the risk appetite/discipline I have incorporated in the conservative way I manage Seabreeze Partners.

* If I was to mention the names in the basket — particularly since many of the stocks move plus or minus 10% a day — it would likely be interpreted as a recommendation.

* I don’t feel most retail traders/investors should short stocks for the reasons I have discussed over the last 28 years. This is especially true of these high-beta and volatile stocks.

* When I put on an aggressive short (like this) it should indicate how bearish I am and how unfavorable I view reward vs. risk. That’s the message that I am communicating.

* Frankly it is not hard to figure out several of the constituents in my tech short basket, but I’ll leave it to your imagination.

Position: Short High-Beta Tech Basket

BY Doug Kass · Jul 1, 2026, 7:30 AM EDT

Position: None

BY Doug Kass · Jul 1, 2026, 6:30 AM EDT

* I was very active on the short side yesterday

On the last day of trading for the month and quarter, S&P futures rose as high as +65 handles in what seemed like an algo-driven markup — and closed about +41 handles (as it dropped about 20 handles in the last few minutes).

This morning S&P futures are -30 handles.

Ignored throughout Tuesday was a sharp rise in yields:

TLT low of the day, yields at the high of the day as quarter-end markups started early in the equity markets.

Position: None

BY Doug Kass · Jun 30, 2026, 1:09 PM EDT

As posted in my Diary, fearful of a quarter-end mark-up, I shorted equities more aggresssively yesterday — but on a scale higher (giving the market a wider berth) than I have in several weeks:

* Most notably, on strength and steadily through the day I moved from very small sized to small sized to medium sized index shorts (SPY and QQQ).

* I put on three tranches of my high-octane tech short basket yesterday. I can’t remember when I did so aggressively in the past but it reflects my view of the exceptionally poor reward vs. risk on the market darlings.

* I added meaningfully to my GRNY short and added to JOET short.

* On the buy side I added to PEP and PG, which should prosper in a correction.

* With the rescheduling of cannabis hearings going so well, I added to individual weed longs. The group looks like it might finally be breaking out of a range.

Position: Long PEP (S), PG (S), VRNOD (S), GLAS (S), GTBIF (S), TRLV (S), CURLD (VS); Short SPY (M), QQQ (M), GRNY (M), JOET (S), High-Beta Tech Basket

BY Doug Kass · Jul 1, 2026, 6:05 AM EDT

THE S&P Short Range Oscillator remains in a small overbought at 1.34% vs. 1.73%.

The Oscillator has basically been small overbought throughout the month of June.

Position: Short SPY (M), QQQ (N)

BY Doug Kass · Jul 1, 2026, 5:45 AM EDT

I will mention this as no one else is.... Raise your hand if you think the central bankers being interviewed by @saraeisen are smug (read: an annoying sense of superiority) with a sense of entitlement... Raise your hand if you think that attitude is unjustifed based on their Show more

BREAKING: The man who saw 2008 coming just placed his biggest bet against the AI boom, and the strangest name on his list is not a tech company at all. It is a bulldozer maker. Dr. Michael J. Burry shorted Nvidia, Applied Materials, Tesla, and the whole chip index this week. Show more

The CNBC Panelist Said What? (Issue #6) Then there is Adobe and Halftime panelist Jim Lebenthal. Jim is a bright guy, a Princeton graduate and the brother of Alexandra and the son of municipal bond legend (Lebenthal & Company's James Lebenthal ) James A. Lebenthal - Wikipedia. Show more

The CNBC Panelist Said What? (Issue #5) It seems only natural to follow up yesterday's Issue #4 (Tom Lee) with CNBC's Josh Brown - as they are likely among the most conspicuous guests and panelists on CNBC. While Tom Lee pays to deliver his calls (the worst of which was his