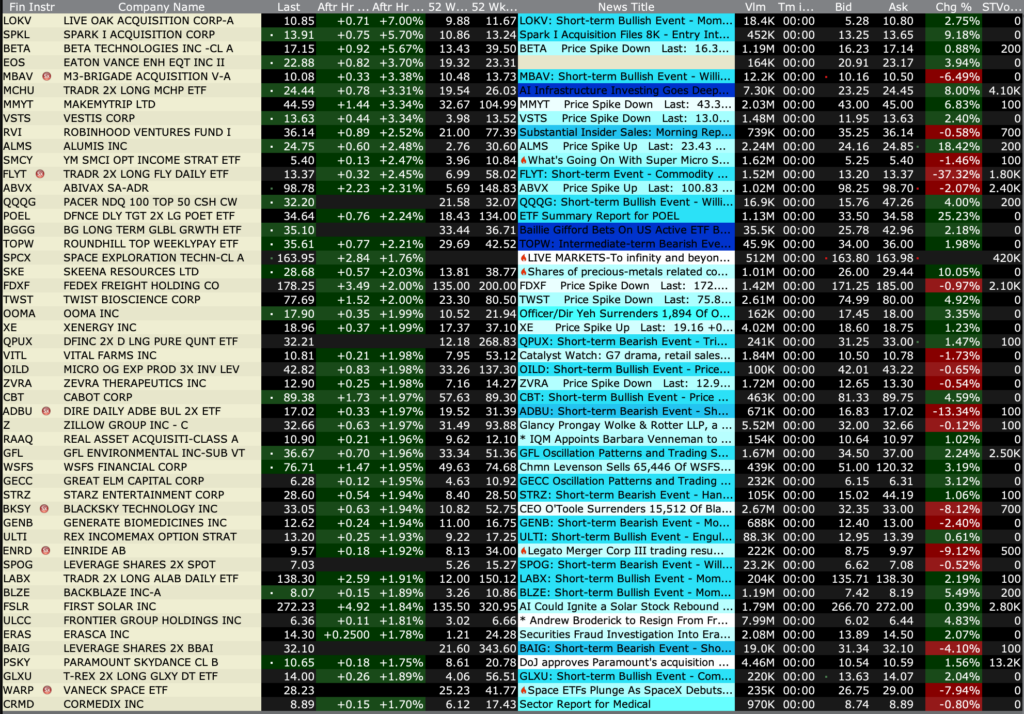

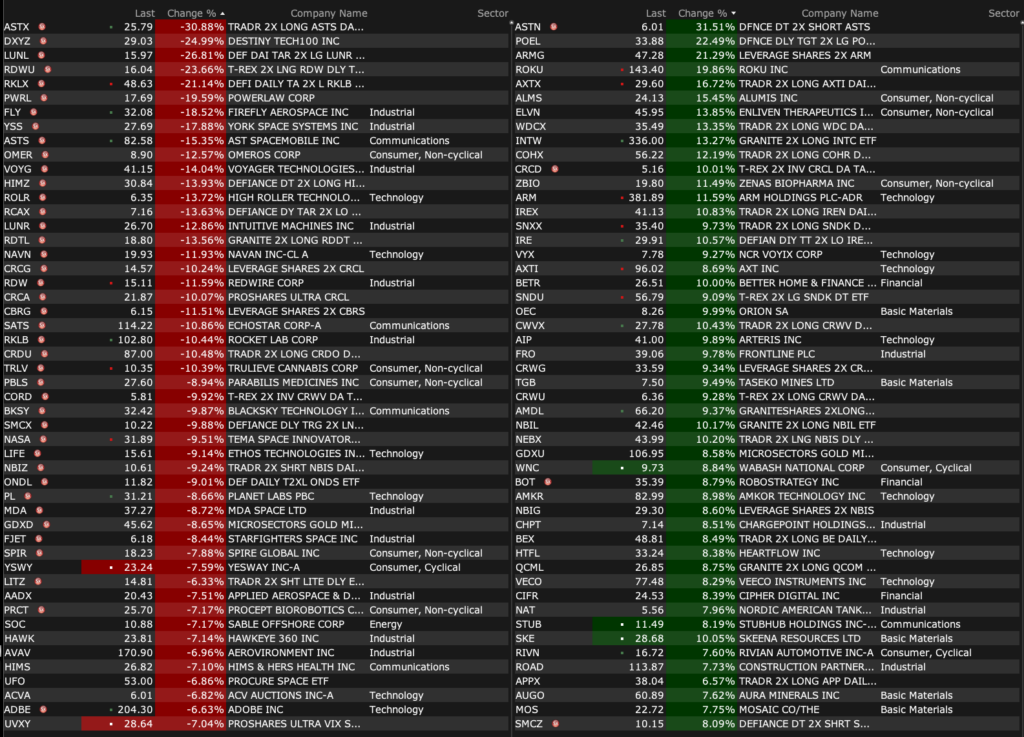

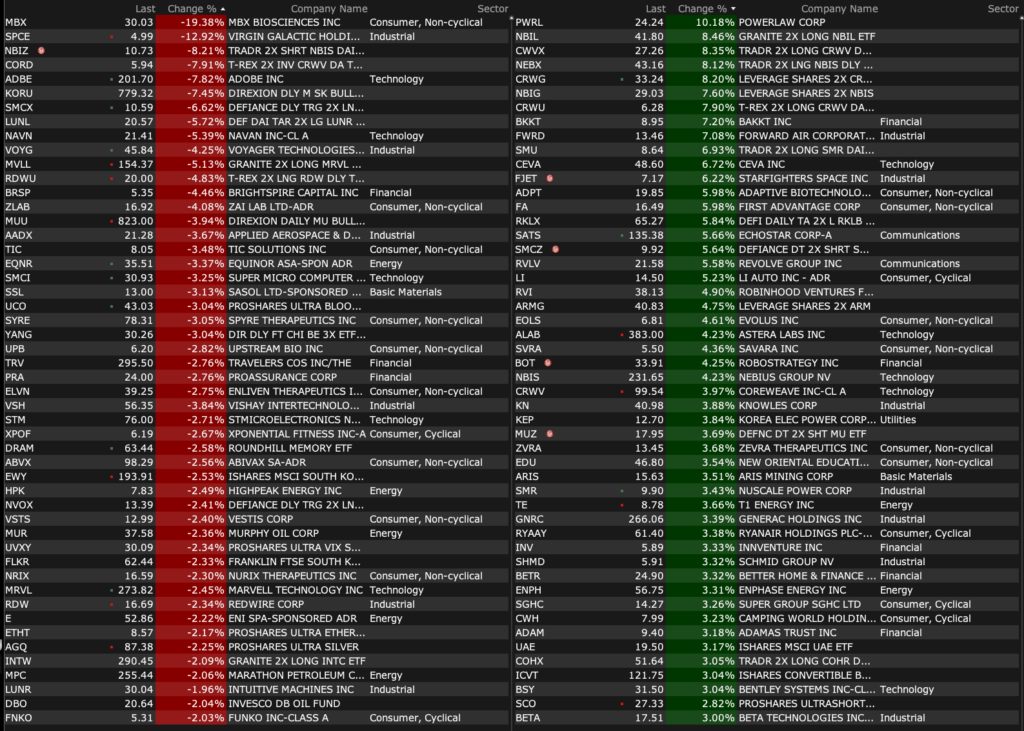

Friday’s After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 12, 2026, 4:40 PM EDT

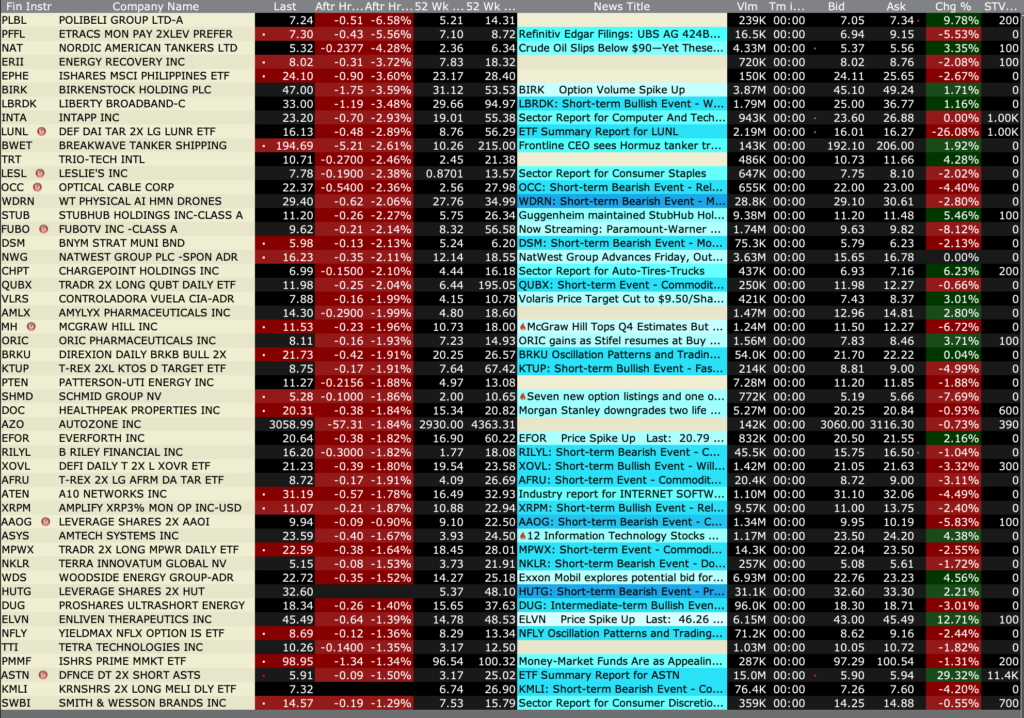

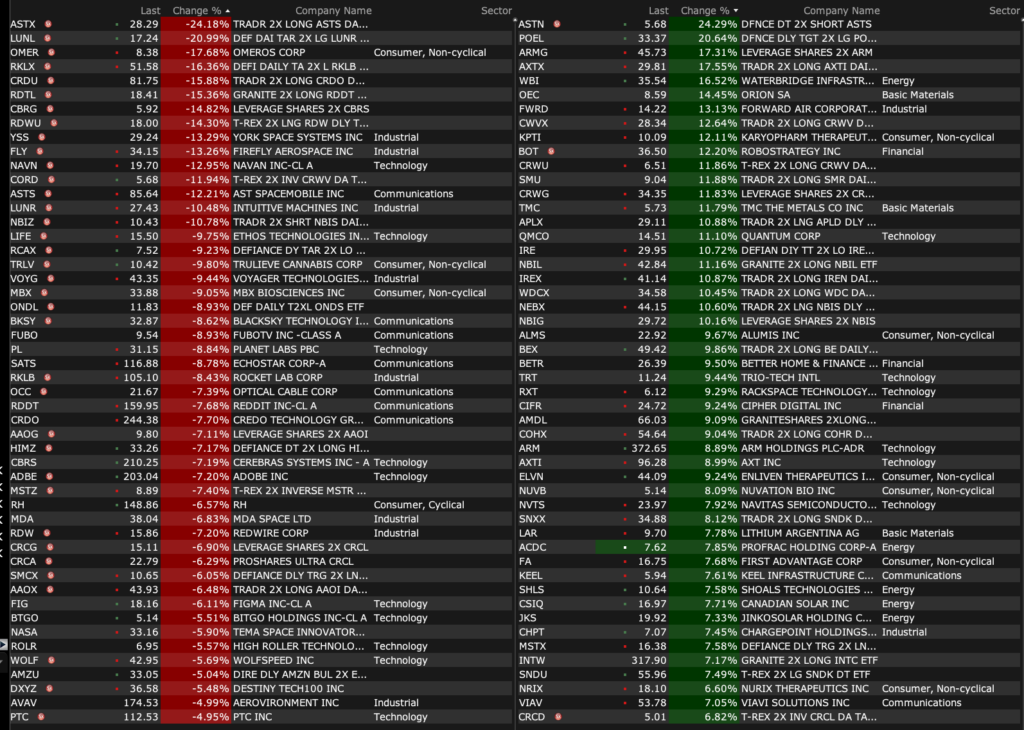

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 12, 2026, 4:40 PM EDT

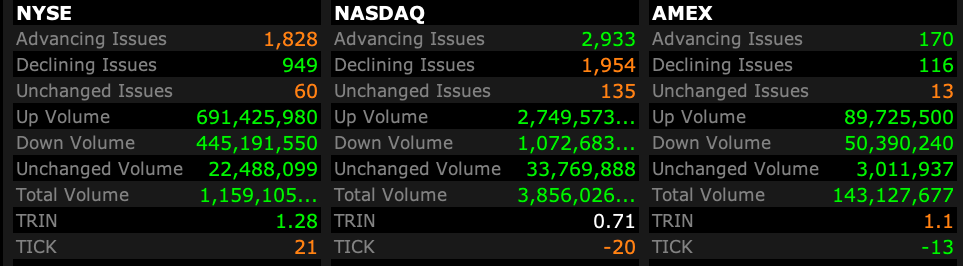

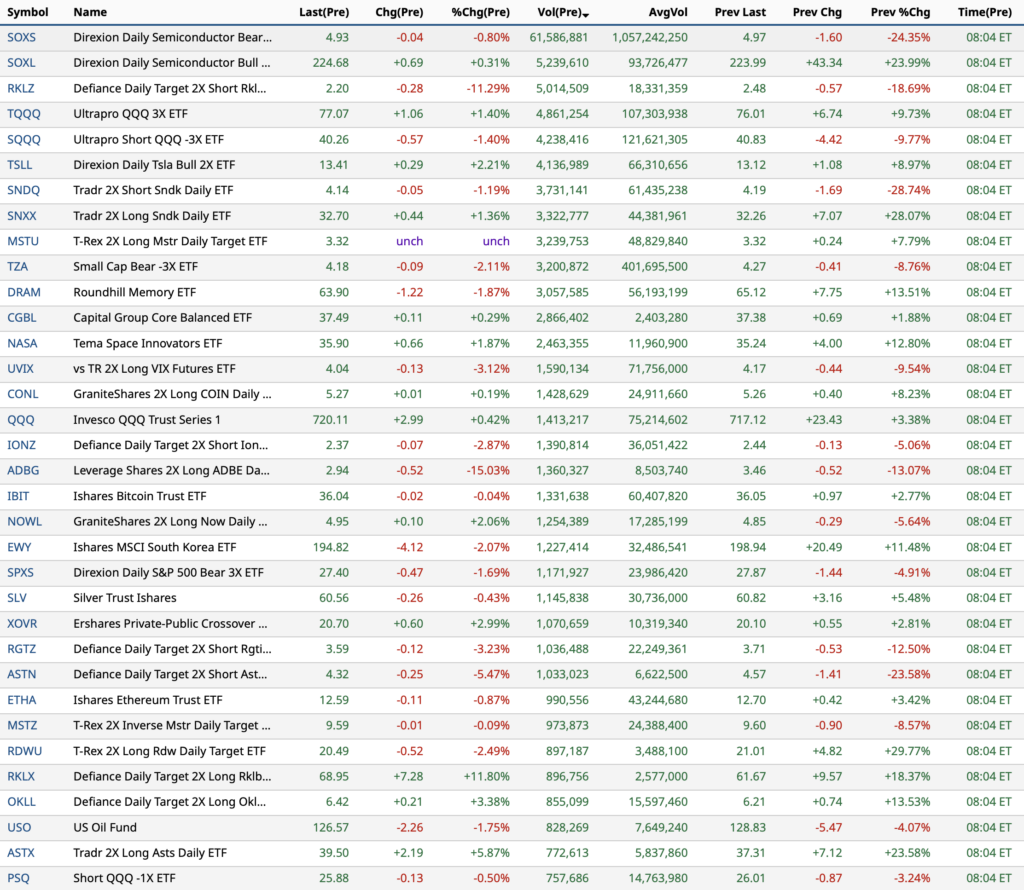

Closing Volume

– NYSE volume 10% below its one-month average

– NASDAQ volume 7% above its one-month average

– VIX index: down 9.31% to 17.63

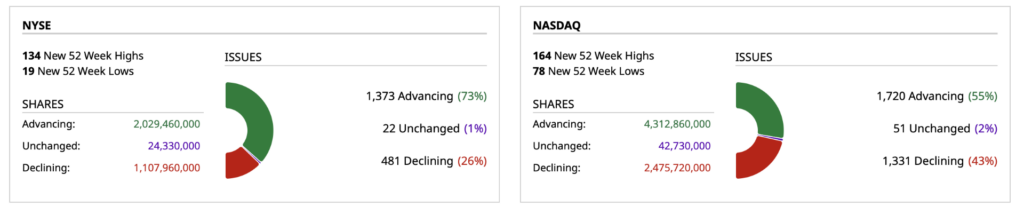

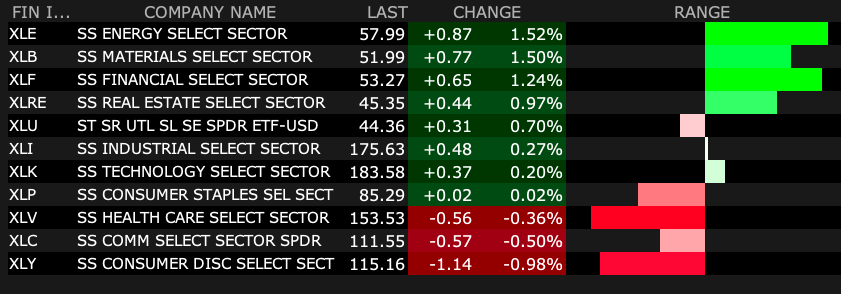

Breadth

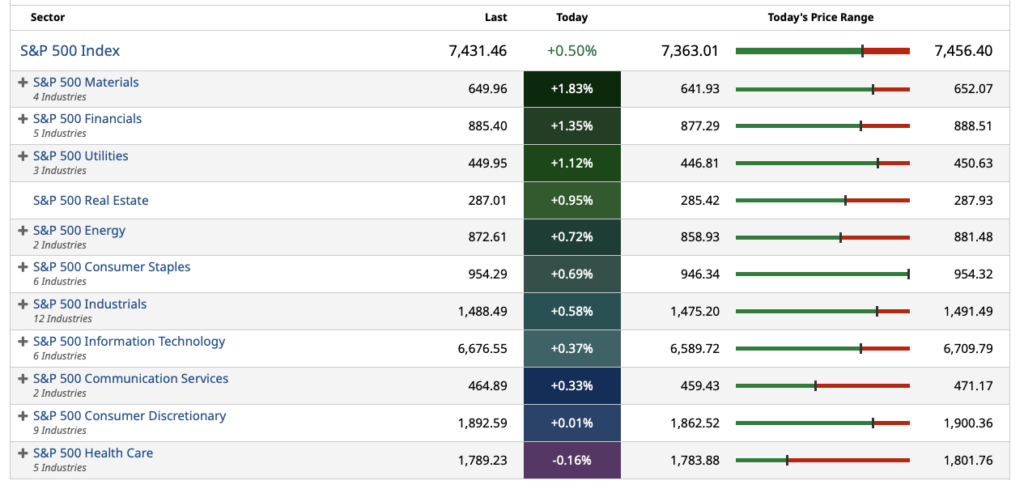

S&P 500 Sectors

% Movers

Position: None

BY Doug Kass · Jun 12, 2026, 4:28 PM EDT

I re-shorted Tesla (TSLA) at $401.99.

Position: Short TSLA (VS)

BY Doug Kass · Jun 12, 2026, 3:05 PM EDT

Now that the SpaceX (SPCX) IPO has occurred I am back shorting the beneficiaries of that transaction:

* GS $1067.89

* &MS $215.15

Position: Short GS (VS), MS (VS)

BY Doug Kass · Jun 12, 2026, 2:55 PM EDT

With S&P cash +35 handles I have, once again, created a short package of high-octane (beta) equities.

I recently put on the same package and took a very quick profit.

My current expectations are based on a longer timeframe.

Position: Short SPY (VS), Spec Package

BY Doug Kass · Jun 12, 2026, 2:45 PM EDT

From Peter Boockvar:

Positives,

1) Congrats to Elon Musk and team for building a business that has led to the biggest IPO on record.

2) Off a record low, the June UoM confidence index rose to 48.9 from 44.8 with both the Current Situation and Expectations rising m/o/m. With the dip in gasoline prices, one year inflation expectations slipped to 4.6% from 4.8% while the 5-10 yr guess fell to 3.4% from 3.9%. The employment component was little changed but hovering around the lowest level on record. Income expectations were less negative. Spending intentions were mixed, rising for vehicles after falling last month but for buying a home, it fell to the lowest since last September. For a major household appliance, it rose 1 pt off a record low. UoM said, “This measured improvement in sentiment was widespread, seen across age, education, and political party. Lower-income consumers exhibited a particularly strong sentiment increase, consistent with the fact that gasoline comprises a larger share of their budgets.” But, “Even with June’s early gains, however, views of the economy are still relatively dour. Sentiment is currently 13% below January 2026 and 19% below a year ago, as consumers remain focused on kitchen table issues. They feel burdened by the recent escalation in inflation and worry that higher inflation could remain stubborn going forward, particularly in the short run…Consumers continue to express frustration about the persistence of high prices more generally. About 57% of consumers spontaneously mentioned that high prices were eroding their personal finances, unchanged from last month and up from 36% a year ago.”

3) Not with help from lower mortgage rates as they were little changed from last week at 6.60%, purchase applications rebounded by 7.3% w/o/w after three weeks of declines. Refi’s rose 15.3% w/o/w after six weeks of declines. Months’ supply held at 4.5 while the y/o/y home price gain was 1.3%. First time buyers rose to 35% of all purchases vs 30% one year ago, a good sign.

4) While still depressed, the closing of home sales in May (most contracts likely signed in February thru April) , rose to 4.17mm from 4.04mm and above the estimate of 4.07mm.

5) From RH: “I think as we’ve moved past the peak investment cycle this year we believe our top line is going to inflect, that kind of irrelevant of what the external market does unless it really, look, if we get into a war that massively impacts the economy, the inflation, so on and so forth, it’s going to put pressure on everyone where those things happen, but we don’t need a big move in the housing market to grow. We don’t even need a move in the housing market. I’m not counting on the guidance we just gave everyone. I’m not counting on the market getting any better. I mean, the market can get worse, and I’d be surprised if we don’t beat those numbers.”

6) From Casey’s General Store: “So with respect to the consumer, I would say overall, I think consumers are hanging in there. They’re probably being a little more discerning about where they shop and how they spend their money. But we’re seeing growth across all of the income cohorts. And the way we look at that is below $50,000 a year in income is a low income, $50,000 to $100,000 a year is mid and above $100,000 is higher income. And I’d say that all three, we’re seeing growth, a little bit less so in the lower income. The other two cohorts, which is three quarters of our guest base, are spending comparably to what they’ve been spending on.”

7) From Cracker Barrel Old Country Store: They are also benefiting from having a lower average check size relative to the industry. “In Q3, our average check was $15.85 compared to over $27 in casual dining and over $19 in family dining, underscoring our lower prices versus competitors. In fact, guests can order add-ons with us and their check will still be lower than an entree at many of our peers.” Business still fell in the quarter, with comps down 2.6%, “which included a traffic decline of 6.7%. Although traffic remained negative, we are encouraged by the gradual improvement in the underlying traffic trend. The restaurant average check increased 4.3%, including pricing of 4.4%.”

8) From JM Smucker: “Total company net sales increased 6%, driven by growth in the Coffee, Away From Home, Pet Foods, and Frozen Handheld and Spreads segments.”

9) From ABM Industries: Offering janitorial services to office buildings in particular, “the prime office recovery continues to gain traction. Although as mentioned, the market is still experiencing some softness on the West Coast. The US office leasing is approaching 2019 levels. Net absorption turned significantly positive in the first quarter, the strongest since 2020 and prime vacancy rates continue to tighten. New supply remains extremely limited with the construction pipeline nearly 90% below its 2020 peak.”

10) As fully expected, the European Central Bank raised its deposit rate to 2.25% from 2.00%. While they have chosen to not look past the higher oil price shock, they also previously took its rate down to zero on a REAL basis which was already quite aggressive. In their statement they said “The outlook remains uncertain, with upside risks for inflation and downside risks for economic growth.”

11) China reported its May trade data and note here too the likely inventory stocking mentality of those placing orders. Exports grew by 19.4% y/o/y, above the estimate of 15%. Imports jumped by 27.4%, just above the forecast of 26% growth. Their monthly trade surplus of $105 billion is still quite astonishing. About half of the growth of both imports and exports were tech related, particularly chips and computer hardware with a lot from price rather than volume. Auto exports were strong too as we know China cars are flooding other markets.

12) Some pull forward of ordering was also likely seen in the somewhat dated April trade data out of Germany where exports rose .9% y/o/y vs the estimate of down .5% while imports grew by 1.2% vs the forecast of a decline of 2%.

Negatives,

1) The May headline CPI rose .5% m/o/m as expected and by .2% at the core level which was one tenth below the forecast. The y/o/y figures of 4.2% and 2.9% were as estimated due to rounding and up from 3.8% and 2.8% respectively in April. Energy prices jumped by 3.9% in the month led by a 7% rise in gasoline prices and now higher by 23.5% y/o/y. Electricity prices in particular rose by .6% m/o/m and 5.9% y/o/y. Food prices were up by .2% m/o/m and 3.1% y/o/y. Services inflation ex energy saw prices higher by .3% m/o/m and 3.4% y/o/y led again by rents. Core goods prices were little changed again m/o/m, down one tenth and up by 1.1% y/o/y.

2) When we include the downward revision in April for the heady PPI read, the May headline figure was as expected but showing a 2nd straight month of 1.1% wholesale price increases after a .7% gain in March and .6% gains in each of January and February. The y/o/y headline gain was 6.5%, up from 5.7% in April. The core rate was higher by .4% m/o/m after a .7% increase in the month before and which followed an .8% gain in January, .4% rise in February and .2% increase in March. Core wholesale prices are up by 4.9% for a 2nd month y/o/y. Core goods prices were up .8% m/o/m and by 5.1% y/o/y with plastic resins and industrial chemicals leading this ex food and energy category. On the services side, prices were up .3% m/o/m and by 4.9% y/o/y and higher asset prices were a factor. The BLS said “Over 40% of the May advance in the index for final demand services can be traced to a 4.8% rise in prices for portfolio management.”

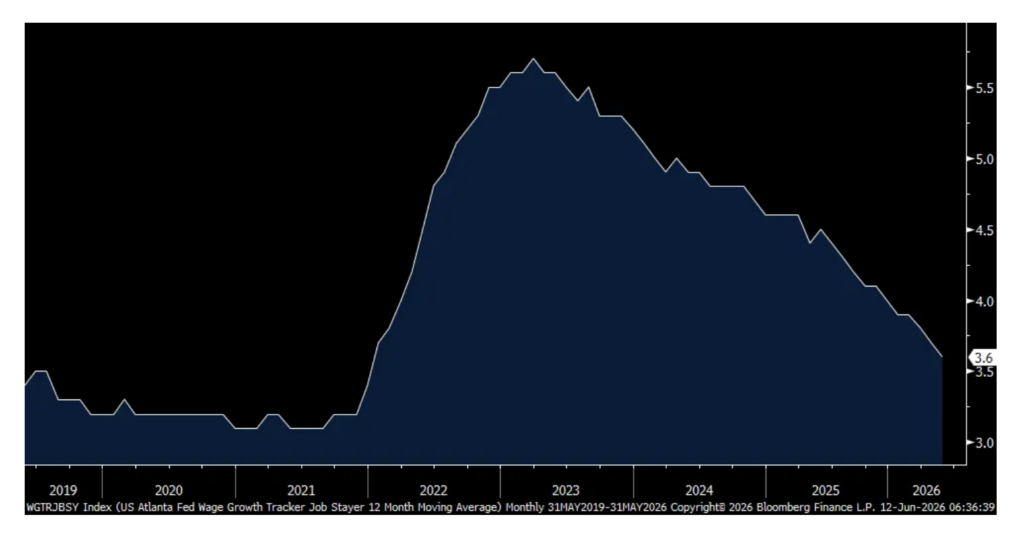

3) On the heels of seeing headline CPI for May rise 4.2% y/o/y, the Atlanta Wage Growth Tracker out yesterday showed a 3.5% y/o/y rate of growth and highlights the economic squeeze that continues on for many. For the ‘job switcher’, wages were up 4.3% y/o/y, holding the April gain. For ‘job stayers’, they were up higher by 3.6% which continues to decelerate.

4) Initial jobless claims rose 4k w/o/w to 229k and that was 9k more than anticipated. This brings up the 4 week average to 219k from 215k and while still low, is the most since February. Continuing claims rose by 24k to 1.795mm which is a 7 week high but still below the 1.9mm ish that we saw last year.

5) The NFIB May Small Business Optimism, today they reported their full report and the headline index fell to 95.3 from 95.9 and that was the weakest since October 2024. Plans to Hire fell to the lowest since May 2020 as did Job Openings Hard to Fill. Also of note, Higher Selling Prices rose by 6 pts to the highest since March 2023. The chief economist of the NFIB highlighted the two lane economy on the corporate side, “AI investment spending has contributed to some excitement in the economy. Despite the enthusiasm around AI, the overall picture is divided. More small business owners are struggling with significant and unpredictable hikes in fuel prices, which are more challenging for small businesses to pass on to their customers compared to their larger corporate competitors.” Also, “In May 19% of small business owners reported taxes as their single most important problem, up 2 pts from April and ranking as the top issue. Reports of inflation as the single most important problem rose for the 3rd consecutive month in May. 18% of business owners cited inflation as their single most important business problem, up 2 pts from April and marking the highest reading since December 2024.”

6) From the May NY Fed’s Consumer Expectations Survey: “Perceptions…compared to a year ago deteriorated, with a larger share of households reporting a worse financial situation, marking the highest reading since January 2023, and a slightly smaller share of households reporting a better financial situation. Year-ahead expectations about households’ financial situation also deteriorated, with an increase in the net share of households expecting a worse financial condition. The net share of households expecting a better versus worse financial situation in one year is at its lowest level since October 2022.”

7) Container shipping rates continue to rise. The Shanghai to NY average 40 foot container price jumped by another 6.6% to $5,870, the highest in a year. Shanghai to LA saw its price up by 2.6% w/o/w to $4,683 after spiking by 31% last week. The Shanghai to Rotterdam route rose to the most expensive since January 2025.

8) A price war coming in the sector that is driving a large amount of economic growth and stock market performance? https://www.wsj.com/

9) From Lennar: “Our second quarter of fiscal year 2026 was defined by the same stubborn headwinds that have challenged the housing market for the past several years – persistently elevated mortgage rates, constrained affordability, and cautious consumer sentiment, exacerbated by geopolitical uncertainty creating a resurgent inflation reading of 4.2% driven by higher energy prices…Our average sales price was $371,000, reflecting approximately 12.9% in incentives, along with base price adjustments necessary to sustain volume in a market where affordability remains the defining constant.”

10) From Oracle: With CapEx needs rising even further and to help close their cash flow and large funding gaps, “we expect to raise around $40 billion in debt and equity in our fiscal year ‘27, and that includes our already announced $20 billion at the market equity issuance. We don’t anticipate raising additional debt funding in calendar year 2026.”

11) From Chewy: “Pet remains a resilient category driven by recurring non-discretionary needs and strong emotional attachment. At the same time, consumers are growing more discerning, driven in part by elevated fuel prices and broader macroeconomic pressures…we are seeing a modest level of incremental pressure on premiumization and product attach rates amongst our current customer base…We no longer believe it is prudent to embed a meaningful acceleration in consumer spending into our outlook, given the current operating environment.”

12) From JM Smucker: With respect to overall inflation, ex green coffee deflation and tariffs, “we do anticipate cost inflation of low single digits across the balance of our portfolio, and that’s largely coming through packaging, ingredients and transportation.”

13) From Campbell’s: “So base inflation before the Middle East conflict, we were looking at base inflation of around 3%. So obviously with the price of oil where it is, and look, if oil stays around $100 a barrel, we’re looking at an additional 2% to 3% inflation on top of the core 3%. Also, as you probably know, there’s a driver shortage out there that not only are we having higher diesel costs, but that is causing higher inflation from a logistics and freight perspective as well.”

14) The Bank of Canada Governor in his presser distilled the box central bankers are in quite succinctly. Tiff Macklem said “Economic weakness combined with rising inflation is a dilemma for monetary policy. Raising rates to dampen inflation could further slow the economy. Easing rates to support growth increases the risk that higher inflation becomes persistent. For now, holding the policy rate unchanged balances those risks.”

15) In order to stem both the rising inflationary pressures but also the weakness in its currency, the Bank Indonesia unexpectedly raised rates by 25 bps to 5.50%. This was NOT a scheduled meeting and they now have hiked by 75 bps since April 22nd when they last left rates unchanged.

16) China is seeing quite the spread between CPI and PPI. In May, CPI rose 1.2% y/o/y while PPI jumped by 6.3% y/o/y.

17) German factory orders were weaker than expected, falling 3.8% m/o/m vs the expected drop of 2% and March was revised down by 5 tenths to a 4.5% gain. Declines were seen in auto, electrical equipment and machinery. The economy ministry said “There are growing signs that rising energy and commodity prices, as well as significantly heightened geopolitical uncertainty, are increasingly leading to lower demand, particularly for capital goods. Against the backdrop of rising costs and uncertainties, as well as growing supply chain bottlenecks, industrial activity is likely to continue to show only modest growth in the coming months.”

Positions: None.

BY Doug Kass · Jun 12, 2026, 1:15 PM EDT

BY Doug Kass · Jun 12, 2026, 12:24 PM EDT

Position: None

BY Doug Kass · Jun 12, 2026, 11:55 AM EDT

I had guessed on Twitter that the SpaceX (SPCX) IPO would open up by about 10%.

That “forecast” is looking reasonably accurate.

I also believe the opening could coincide with a short-term market top.

Position: None

BY Doug Kass · Jun 12, 2026, 11:51 AM EDT

I moved to a large short in GRNY at $27.30.

Position: Short GRNY (L)

BY Doug Kass · Jun 12, 2026, 11:45 AM EDT

With my additional index shorts (below) I moved from very small to small sized:

* SPY $744.19

* QQQ $723.79

Position: Short SPY (S), QQQ (S)

BY Doug Kass · Jun 12, 2026, 11:40 AM EDT

I am taking half of my MSFT long off at $389.74, for a +$7 gain from a few hours ago.

From earlier:

I just bought back:

* MSFT (MSFT) $382.71

Positions: Long AMZN S MSFT S

BY Doug Kass · Jun 12, 2026, 9:47 AM EDT

Position: Long MSFT (VS)

BY Doug Kass · Jun 12, 2026, 11:25 AM EDT

– NYSE volume 13% below its one-month average;

– Nasdaq volume 6% above its one-month average;

– VIX index: down 0.36% to 19.37

Positions: None.

BY Doug Kass · Jun 12, 2026, 11:20 AM EDT

BY Doug Kass · Jun 12, 2026, 10:40 AM EDT

BY Doug Kass · Jun 12, 2026, 10:24 AM EDT

Position: none.

BY Doug Kass · Jun 12, 2026, 10:05 AM EDT

BY Doug Kass · Jun 12, 2026, 9:47 AM EDT

I covered all my index shorts on the whoosh lower:

* SPY (SPY) $738.09

* QQQ (QQQ) $713.55

Its going to be a wild and volatile day today.

I want to be opportunistc.

I want to sell strength.

Positions: None.

BY Doug Kass · Jun 12, 2026, 9:42 AM EDT

From Peter Boockvar:

It seems that the pressure on reopening fully the Hormuz Strait took on another level after hearing from the executives at Exxon and Chevron a few weeks ago when they talked at a conference about heading towards dangerous levels of inventories. And then I saw the article yesterday in the Washington Post titled “Oil Executives Warn White House That Gas Prices Will Get Worse” and which said “Oil and gas executives have warned the White House that gasoline prices could surge in coming months as fuel inventories fall to critical lows…Industry officials say they are doing everything they can to sound an alarm that prices are about to soar as the commercial and government inventories that have mitigated price rises so far are rapidly depleting, according to multiple people familiar with the conversations…Some inventories could be wiped out within weeks, the executives have warned, coinciding with the peak summer travel season.”

Unfortunately with an eventual deal though, I still don’t think we’re going to get everything we want but that’s the situation we’re in dealing with a regime like Iran. We’re just going to have to accept a deal that is not ideal it seems.

With regards to oil and gas stocks, the XLE will open less than a buck from where it stood on the February Friday before the conflict began. Believing that oil prices, after the price correction upon a deal fully runs its course, are not going back to pre-war levels and we still have the big picture challenge of slowing US production growth, we remain long the group.

A deal and full Strait reopening would be good timing for new Fed Chair Kevin Warsh as he would be able to better analyze the economic backdrop with more clarity and much less fog. I was never of the belief that the Fed should respond to the rise in oil and commodity driven inflation triggered by the war because at any moment the war could end and hopefully that’s the case now.

Today we celebrate coming to the public market of one of America’s technological wonders and one of our greatest entrepreneur’s. The reusable rocket has to be on the top 20 lists of greatest inventions in world history. The Starlink business is finally a satellite based telecommunication company that actually makes money (I remember Iridium, Globalstar, etc..). As for xAI, your guess is as good as mine on whether data centers in space can happen and if so, done in a cheaper fashion than on the ground and where a fix can take place if something breaks without sending technicians on rockets there every time. And, it’s growing more clear how competitive and costly providing cloud infrastructure is and how tough competing with Gemini, Anthropic, OpenAI and others globally is going to be. As for all the other moonshot hopes, I hope it all happens.

As for the valuation and how it trades in coming days/weeks/months, I have my popcorn out as I’ve never seen as much investor excitement to ‘get in’ than this. Speaking generally about the GenAI business, because of the hugely capital intensive nature of building out the GenAI infrastructure and likely continued high levels of maintenance CapEx, I believe the benefits in the future will more accrue to the users of the technology rather than as major profits and high returns on invested capital for the providers of it.

On the heels of seeing headline CPI for May rise 4.2% y/o/y, the Atlanta Wage Growth Tracker out yesterday showed a 3.5% y/o/y rate of growth and highlights the economic squeeze that continues on for many. For the ‘job switcher’, wages were up 4.3% y/o/y, holding the April gain. For ‘job stayers’, they were up higher by 3.6% which continues to decelerate.

Atlanta Wage Growth Tracker y/o/y

Job Switcher y/o/y

Job Stayer y/o/y

RH is always one of my favorite conference calls as CEO Gary Friedman gives us his 2 cents on things. They of course cater to the higher end consumer but have also dealt with the challenges of a tough housing market. From him:

“I think as we’ve moved past the peak investment cycle this year we believe our top line is going to inflect, that kind of irrelevant of what the external market does unless it really, look, if we get into a war that massively impacts the economy, the inflation, so on and so forth, it’s going to put pressure on everyone where those things happen, but we don’t need a big move in the housing market to grow. We don’t even need a move in the housing market. I’m not counting on the guidance we just gave everyone. I’m not counting on the market getting any better. I mean, the market can get worse, and I’d be surprised if we don’t beat those numbers.”

From Lennar who reported too and with numbers that missed expectations and they lowered their Q3 delivery guidance:

“Our second quarter of fiscal year 2026 was defined by the same stubborn headwinds that have challenged the housing market for the past several years – persistently elevated mortgage rates, constrained affordability, and cautious consumer sentiment, exacerbated by geopolitical uncertainty creating a resurgent inflation reading of 4.2% driven by higher energy prices.”

“Our average sales price was $371,000, reflecting approximately 12.9% in incentives, along with base price adjustments necessary to sustain volume in a market where affordability remains the defining constant.”

Positions: None.

BY Doug Kass · Jun 12, 2026, 9:35 AM EDT

I covered some index shorts on the sell off:

* SPY (SPY) $738.76

* QQQ (QQQ) $715.17

From earlier:

Dougie Kass

Added to Index shorts at 540AM

SPY $743.19

QQQ $721.05

Position: None

BY Doug Kass · Jun 12, 2026, 7:17 AM EDT

Positions: Short SPY S QQQ S

BY Doug Kass · Jun 12, 2026, 9:11 AM EDT

Positions: None.

BY Doug Kass · Jun 12, 2026, 9:10 AM EDT

Positions: None.

BY Doug Kass · Jun 12, 2026, 9:00 AM EDT

Positions: None.

BY Doug Kass · Jun 12, 2026, 8:50 AM EDT

* The rally in equities seems unjustified…

The S&P Index is now more than +7% above the level the day before the start of the Iranian conflict in late February.

The advance doesn’t make sense to me. Iran remains in control of the Strait of Hormuz, no matter what the parties agree to. Iran can easily reimpose a block as soon as the American blockade ends.

The U.S. has spent over $30 billion — eroding our already burgeoning budget — and we have sharply reduced our inventory of critical weapons systems. Arguably our President looks weak with his endless Taco behavior and boasts followed by empty threats.

Our country has alienated our European allies and weakened NATO, who Pres. Trump blasts them with never ending tariffs. He continues to threaten our allies and he is then surprised they refuse to provide aid and support when requested.

Meanwhile, the Gulf allies realize that the American umbrella doesn’t protect them and will likely force them to reconcile in some way with Iran. The market structure is breaking and destabilized with extreme volatility forming the investment background of structural instability (see my earlier post Structural Instability. )

The investing public has decided the best option available to them is stocks. A change in the bullish behavior (of buying every dip) might require a change in the perception of optimistic economic and profit growth (which I believe is closer than the consensus thinks).

As noted previously, I call on Warren Buffett’s famous “God’s Plan” thoughts and words delivered in November, 1999 near the end of the dot.com boom:

FortuneMagazine.pdf november 1999 interview

Positions: None.

BY Doug Kass · Jun 12, 2026, 8:33 AM EDT

Dougie Kass

Added to Index shorts at 540AM

SPY $743.19

QQQ $721.05

Position: None

BY Doug Kass · Jun 12, 2026, 7:17 AM EDT

The S&P Short Range Oscillator remains in neutral at -0.10 vs. -0.61.

Position: Short SPY (S), QQQ (S)

BY Doug Kass · Jun 12, 2026, 6:51 AM EDT

Position: None

BY Doug Kass · Jun 12, 2026, 6:45 AM EDT

* This morning SpaceX launches a $75 billion initial public offering, valuing the company at nearly $1.8 trillion

* Discussions of the IPO today will consume the business media as guests deliver plenty of hype and similar/redundant “talking points” but provide little substance — full of sound and fury but signifying nothing…

Over history Warren Buffett has expressed skepticism about initial public offerings.

To Warren it was unlikely that the best bargain was a brand new IPO that is heavily marketed and carries ridiculously high commissions.

Perhaps Warren Buffett’s most famous quote regarding IPOs revolves around the notion that an IPO is priced at a time of the seller’s choosing while being actively promoted by both insiders (to maximize their profits) and by Wall Street (who exist to sell products):

“An IPO is like a negotiated transaction – the seller chooses when to come public – and it’s unlikely to be a time that’s favorable to you.”

He compared IPOs to buying lottery tickets, saying:

“People win lotteries every day… You don’t want to get into a stupid game just because it’s available.”

He further said:

“The idea that a newly issued security (IPO)—brought to market at a time of the seller’s choosing and surrounded by massive hype—is the single best bargain among thousands of global businesses is absolute nonsense.

When an offering carries a ridiculous 7% commission just to incentivize salespeople, it simply cannot be the most attractive investment available.

While people easily get caught up in the excitement of a new launch, look at the reality: you have thousands of existing public companies whose prices are set by a natural auction market, free from aggressive promotion or hidden fees.

It makes no sense to buy a security precisely when an insider decides the timing is perfect to sell. Frankly, it isn’t worth spending five seconds thinking about IPOs.”

Here are some of my specific views of the SpaceX IPO (hint: we are avoiding the offering and currently considering shorting the shares on strength in the aftermarket):

Finally, from my Daily Diary on Wednesday:

The Marx Brothers respond:

BY Doug Kass · Jun 10, 2026, 7:15 AM EDT

Position: None

BY Doug Kass · Jun 12, 2026, 6:15 AM EDT

The embedded tweet could not be found…

POLYMARKET PROJECTS $174 OPENING SPACEX SHARE PRICE, IMPLYING A 29% OPENING POP.

SpaceX IPO's closing market is 53% likely to be above 2 trillion, per Polymarket:

This chart is why I'm staying away from the SpaceX IPO. Five of the most hyped IPOs of the last 15 years, and every single one collapsed after listing. - UBER lost 70% of its IPO price. - META crashed 77% from its peak. - Robin Hood fell 92%. - Coinbase fell 93%. - Rivian fell Show more

This is how you price an IPO. You don't sell what a company is. You sell what it could become. SpaceX wrote the most ambitious "could become" in SEC history. The filing claims a total addressable market of $28.5 trillion. Larger than the entire GDP of the United States. TheShow more

This week, the largest IPO in human history begins trading. SpaceX. Ticker SPCX. $135 a share. $75 billion raised. A $1.75 trillion valuation. The old record, Saudi Aramco in 2019, raised $29 billion. SpaceX more than doubles it. A view from Switzerland: $1.75 trillion is more

I had guessed on Twitter that the SpaceX IPO would open up by about ten percent ($148). (Dan Niles referenced a higher number, $180) Many on Fin TV - like Jim Cramer - were saying with confidence much higher numbers. My"forecast" is looking reasonably accurate. I also believe Show more

“An IPO is like a negotiated transaction – the seller chooses when to come public – and it’s unlikely to be a time that’s favorable to you.” - Warren Buffett "Some Advice on the SpaceX IPO From The Oracle of Omaha" -- blog tab of seabreezepartnerslp.com

So, its... God's Plan? "Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it Show more