With Renewed Focus, AT&T's Stock Low Seems to Be in the Rearview

There are still issues with the telecommunications giant but things are improving.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I have been avoiding AT&T T in my portfolio for so long, I probably could not guess the year that the stock held a slot in one of my actively-managed portfolios. Are times changing? The stock certainly is.

AT&T reported the firm's third quarter financial results early on Wednesday morning. Coming in, the stock was up 60% from its cycle low in July 2022. So, yes, at least some investors are indeed coming home to Ma Bell.

For the third fiscal quarter, AT&T posted an adjusted EPS of $0.60 (GAAP EPS: $-0.03) on revenue of $30.213 billion. The adjusted-EPS print beat Wall Street by a few cents despite being down a few cents from the year-ago period. The revenue number fell a touch short of expectations, while reflecting a year-over-year contraction of 0.5%. Adjustments were made mostly for restructuring costs and impairments as well as a small amount for the amortization of DIRECTV.

During the quarter, AT&T realized a net 403,000 post-paid wireless phone adds with an expected industry leading phone churn of 0.78%. This is one reason that we have seen early support for the shares. Mobility service revenues were up 4% to $16.5 billion. Fiber net adds amounted to more than 200,000 for a 19th-consecutive quarter. Broadband revenues were up 6.4% to $2.8 billion.

Operations

Broken out, that $30.213 billion revenue number comes to $25.134 billion (+0.1%) from services provided and $5.079 billion from equipment (-3%) leases and sales. Costs and expenses associated with equipment, administrative and selling or general all contracted. Depreciation and amortization were up more than 8%. That left GAAP operating expenses at $28.097 billion (+14.4%) and GAAP operating income at $2.116 billion (-63.4%). After making adjustments to operating expenses, the firm's adjusted operating income printed at $6.512 billion (down small).

After accounting for interest, other income and taxes, GAAP net income loss attributable to common shareholders printed at just $-226 million, down from $3.444 billion a year ago. This works out to $-0.03 per share. Adjustments add $4.527 billion to that GAAP loss, leading to an adjusted EPS of $0.60.

Fundamentals

For the third quarter, AT&T generated operating cash flow of $10.235 billion. Add to that, $342 million in distributions from DIRECTV. Out of that sum came capex spending of $5.302 billion and $180 million for vendor financing. This left free cash flow of $5.095 billion. Out of that number, the firm paid out $3.057 billion in cash dividends to shareholders.

Turning to the balance sheet, AT&T ended the period with a cash position of $2.586 billion and inventories of $2.529 billion. This puts current assets at $29.799 billion, the bulk in prepaid assets. Current liabilities ended the quarter at $40.658 billion. Debt due within a year amounted to $2.637 billion, while accounts payable came to nearly $32 billion. That puts the firm's current and quick ratios at 0.73 and 0.67, respectively. Not exactly the stuff of champions. For those new to balance sheets, we like to see these ratios or at least the current ratio at 1.0 or higher, so this is not a balance sheet that any fundamental investor would consider strong, or really even acceptable.

Total assets amount to $393.719 billion, including $68.688 billion in goodwill and other intangibles. At 17% of total assets, that at least, is not a problem. Total liabilities less equity comes to $277.437 billion, including a stunning $126.375 billion in long-term debt. Yes, both the current and total debt-loads are daunting. The firm will likely have to roll over at least a portion of its short-term debt at prevailing interest rates.

Given that AT&T is a cash flow beast, the firm should be making every effort to work on reducing that debt load and they are. I understand that maintaining the dividend at this level ($1.11 per share per year, yielding 5.1%) is important to both the firm and its shareholders, so I am not suggesting cutting that dividend further at this time. The firm has cut its debt load by more than $9 billion since the start of the year.

Guidance

For the firm's full year, AT&T is projecting wireless service growth of about 3%, broadband revenue growth of more than 7%, adjusted EBITDA growth of roughly 3%, and free cash flow in between $17 billion and $18 billion. Adjusted EPS is seen at $2.15 to $2.25, which is in line with Wall Street's consensus view of $2.20.

My Thoughts

The business seems solid. The distractions of the past have been jettisoned. AT&T appears to be focused on its core business and its core business alone. That is a real positive. The balance sheet is fairly awful, but it has been for years. At least current management recognizes this and is serious about working on correcting this over time. Wall Street appears to have recognized that AT&T is now investable. I think I can go that far myself at this point.

I don't love it, but I do think the low for this stock is in the rear-view mirror, and a patient investor could build a medium-sized long position in this stock as a revenue provider as one anchor to an otherwise diversified portfolio.

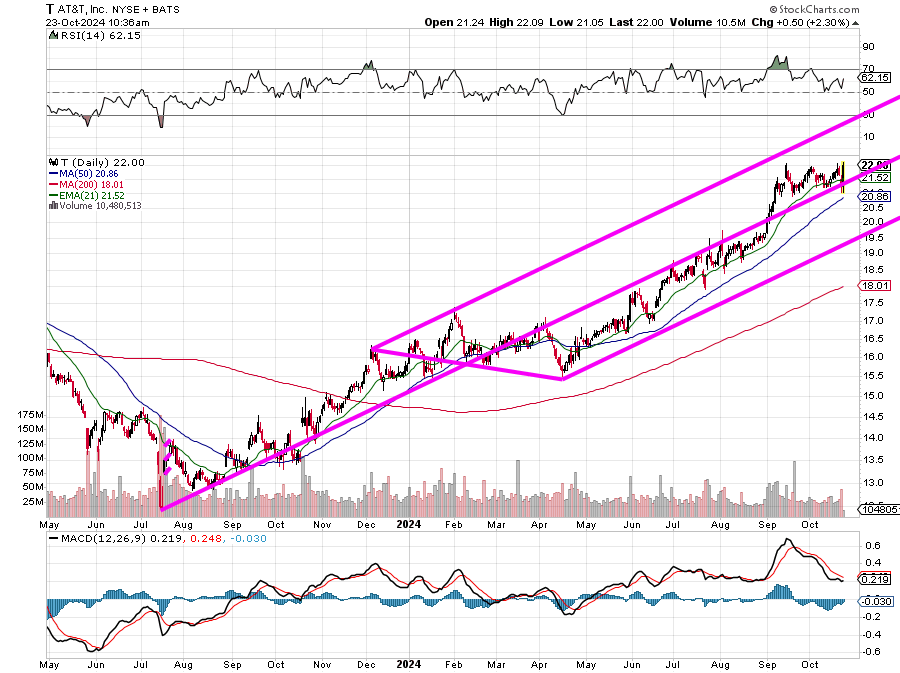

The rise in share price of AT&T since July 2022 is almost perfectly defined by this Andres' pitchfork model. The shares were feeling around the central trendline coming to earnings and the response from Wall Street seems to have helped the shares hold that level.

I would prefer to initiate these shares on a down day, perhaps if they test their 50-day SMA from above in coming days, but I no longer discourage investment in this stock and if I were already long it, I would not be taking profits just yet. It may not seem like much from here, but its still a 10% move. I think this stock sees $25-plus before it goes anywhere near that 200-day SMA, which would be the real panic point in my opinion.

At the time of publication, Guilfoyle had no positions in any securities mentioned.