Why I'm Interested in a Long Position on Palo Alto Networks

The cybersecurity software firm is being warmly received by Wall Street after reporting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Monday evening, cybersecurity software provider Palo Alto Networks (PANW) released the firm's fiscal fourth quarter financial results and those results were warmly received by Wall Street overnight.

For the three-month period ended July 31, 2024, Palo Alto posted an adjusted EPS of $1.51 (GAAP EPS: $1.01) on revenue of $2.19 billion.

These top- and bottom-line results managed to beat Wall Street's expectations, while that sales number reflected year-over-year growth of 12.1%. The total adjustment made was made primarily for share-based compensation expense offset to a significant degree by smaller tax-related adjustments.

Next-Generation Security ARR grew 43% year over year to $4.2 billion, while remaining performance obligation increased 20% year over year to $12.7 billion.

The CEO

CEO Nikesh Arora commented in the press release: " "We finished off the year with strong execution on our platformization strategy in Q4. As we look forward to fiscal year 2025 and beyond, we are focused on scaling our Next-Generation Security business through continued innovation and execution."

The CFO

CFO Dipak Golechha also commented in the press release: "Our top-line strength showed through in our remaining performance obligation and Next-Generation Security ARR. At the same time we successfully balanced profitable growth, as our non-GAAP operating margins increased by more than 300 basis points for the year with strong cash generation, marking one of the best years for Palo Alto Networks."

Operations

As mentioned above, for the period, revenue grew 12.1% to $2,19 billion. Within that total, Subscription & Support driven revenue increased 18.2% to $1.709 billion, and product driven revenue decreased 5.1% to $480.5 million. The cost of this revenue increased 13.2% to $573.7 million, leaving gross profit of $1.616 billion (+11.7%) as gross profit decreased from 74.1% to 73.8%.

Operating expenses grew 15.4% to $1.377 billion, leaving GAAP operating income at $238.4 million (-6%) as GAAP operating margin dropped from 12.1% to 10.7%. On an adjusted basis, operating income was up 6% as operating margin dropped from 28.4% to 26.9%. After accounting for interest, taxes and other income.

GAAP net income printed at $357.7 million (+57.1%), which works out to $1.01 per fully diluted share, up from the year-ago comp of $0.64. Once adjusted, that EPS works out to $1.51 per diluted share, up from $1.44 for the same period a year ago.

Guidance

For the current quarter (Q1, F2025), Palo Alto is projecting total revenue of $2.1 billion to $2.13 billion, which at the midpoint is above the $2.1 billion that Wall Street had in mind and would be good for growth of 12% to 13%. Remaining performance obligation is seen in between $12.4 billion to $12.5 billion, which is a little light, as next Generation ARR is expected to land in between $4.33 billion and $4.38 billion, which is well above the consensus view for $4.32 billion. Adjusted EPS for the quarter is seen at $1.47 to $1.49, also well above expectations for $1.43.

For the full fiscal year (2025), total revenue is seen at $9.1 billion to $9.15 billion, which is also better at the midpoint than expectations for $9.11. This range would be good for growth of 13% to 14%. Remaining performance obligation is expected to print at $15.2 billion to $15.3 billion, still below expectations for $15.7 billion. Next-Generation ARR is seen at $5.42 billion to $5.47 billion. Wall Street was down around $5.28 billion on this number. Adjusted EPS is projected to end the year in a range spanning from $6.18 to $6.31, which at the midpoint is much better than the $6.19 that Wall Street had in mind. The firm also sees a full year free cash flow margin of 37% to 38%.

Fundamentals

For the quarter reported, Palo Alto generated operating cash flow of $512.7 million. Out of that number came $47.4 million in capex spending, leaving free cash flow of $465.3 million. PANW did not return capital to shareholders this past quarter.

Glancing at the balance sheet, Palo Alto ended the quarter with a cash position of $2.579 billion and current assets of $6.85 billion. Current liabilities add up to $7.683 billion. While this number includes short-term convertible notes of $964 million, it also includes $5.541 billion in deferred revenue. As we know, deferred revenues are not true financial obligations, but rather a tally of goods and/or services owed. This puts the firm's current ratio at 0.89 at the headline, which is misleading. Adjusted for deferred revenue, that current ratio rises to a most robust 3.19.

Total assets amount to $19.991 billion, including $3.725 billion in goodwill and other intangibles. At less than 19% of total assets, this is not of concern. Total liabilities less equity comes to $14.821 billion, including no real long-term debt, but another $5.939 billion in deferred revenue. This is one heck of a strong balance sheet.

Wall Street

Since these earnings were reported last night, I have come across 23 highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on PANW. Among these 23 analysts, after allowing for changes, there are 23 "buy" or buy-equivalent ratings and three "hold" or hold-equivalent ratings. One of the "buys" chose not to set a target price, so we are working with 22 of those.

The average target price across our 22 analysts is $387.27 with a high of $416 (Andrew Nowinski of Wells Fargo) and a low of $330 (Rob Owens of Piper Sandler). After omitting those two as possible outliers, the average target across the remaining 20 analysts rises slightly to $388.70. For those who care, the average "buy" target is $393.16, while the average "hold" target is $350.

My Thoughts

This was a solid quarter. When asked about the CrowdStrike CRWD debacle during the call, CEO Arora acknowledged that a number of CrowdStrike customers did come calling, but were so busy trying to correct the issues that new deals were not as easy to get done as one might think. He does think customers, from here on, will consider all of their extended detection and response (XDR) options when making decisions.

The guidance was excellent with the exception of the RPO both for the quarter and for the full year. That said, Next-Generation ARR is running ahead of Wall Street's expectations. Cash flows have weakened, but remain strong, and the balance sheet is a beauty. This is a good company doing a good business. I am already long CrowdStrike and SentinelOne S. Is there room for a third cyber-security stock on my pad? That's what I'm trying to figure out.

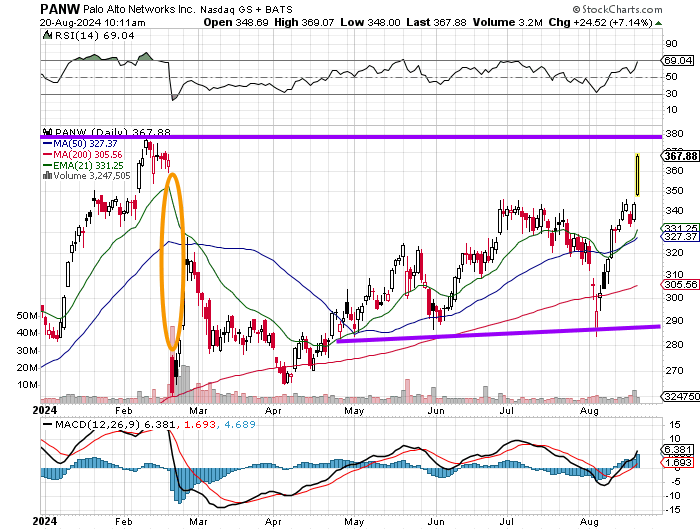

Coming out of the collapse of last February, it took PANW a couple of months to form a proper base. This morning's pop finally fills that gap that had been left open for six months. That February high of $380 is now the stock's pivot. Relative strength is improving steadily and the daily MACD is now, for a couple of weeks, postured quite bullishly for the first time in a while.

While I would not chase the shares on a 7% up day, especially when the indices are down, I once considered Palo Alto to be the best in the cybersecurity business. I had come to see CrowdStrike in that way over the past couple of years but have sized that position so as to face those earnings next week with a comfortable tolerance for risk. I would be interested in initiating a long position at starter size in PANW in either of two scenarios: Either the stock drops and tests its 50-day SMA, or rams right through pivot. A take and hold of that $380 level could unlock the door to a target as high as $435, in my opinion.

At the time of publication, Guilfoyle was long CRWD and S equity.