Who the Heck Is Privia Health and Why Is the Stock Up Big?

The business is growing. The balance sheet is spectacular. There is definitely something here to see. And there's a 'thin blue line' that could determine if it turns into something else.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Privia Health Group PRVA calls itself a technology-driven, national physician-enablement company. What does that mean? Let us try to explain.

The Arlington, Virginia-based company collaborates with medical groups, health plans and health systems. The Privia Platform, powered by the firm's own technology, aims to enhance physician practices, improve patient experiences and help doctors deliver care in both in-person and virtual settings.

The platform is an end-to-end, cloud-based solution that integrates both native and third-party applications into an interface and workflow management optimizer that runs across the full continuum of differing reimbursement arrangements. The platform will support multiple provider types, enable operations at scale, and deliver patient-centric care, qualify metrics and reduce costs.

Privia also provides management services to each medical group that signs on through a local management services organization.

Why Is the Stock Up Wednesday?

At last glance, PRVA is trading near an $17 handle, up more than 7% for the session Wednesday. I haven't found a good reason just yet. Just noticed that the shares were performing towards the top of the S&P SmallCap 600 today.

I did see that throughout May, a certain director purchased rights on five different days. I have also seen that back on May 30 analyst Michael Ha, who is not highly rated at TipRanks, initiated coverage of the name with an "outperform" (buy-equivalent) with a $23 target price, saying that “We believe Managed Care is structurally well positioned to drive sustainably attractive long-term growth, margin expansion and multiple expansion beyond historical levels.”

The short answer, though, is that I don't know why the stock is up Wednesday. Around 8% of the float is held in short positions. That's not nothing, but this is not a short squeeze.

Earnings

Back in early May, Privia posted first-quarter earnings of $0.18 per share (adjusted) on revenue of $415.2 million. Those top and bottom-line numbers both beat Wall Street expectations.

While revenue grew 7.5%, gross profit was up 12.5%, but operating income and net income were down significantly on a GAAP basis. Adjusted, net income showed growth of 16.6%. More than half of the adjustment made was made for total stock-based compensation expense.

The firm is expected to report its fiscal second-quarter numbers in early August. Currently the Street is looking for adjusted EPS of $0.17 on revenue of about $412 million. That would be good for year-over-year growth of more than 22% if realized.

Privia has posted adjusted EPS of $0.51 for fiscal 2022, $0.65 for fiscal 2023, is expected to earn $0.70 for this year and $0.78 for next year, so the steady growth has been and is expected to be there.

Balance Sheet

As of the end of March, Privia had a cash position of $351.136 million and current assets of $728.14 million. Current liabilities add up to $403.798 million, leaving the firm with a current ratio of 1.80, which more than passes muster. There is no short-term debt on the balance sheet.

Total assets amount to $1.032 billion. Of that, $245.56 million is in the form of goodwill or other intangibles. At 24% of total assets, this is high enough to keep an eye on, but not high enough to get nervous just yet.

Total liabilities less equity comes to just $408.762 million (not a misprint). The firm has no long-term debt on the balance sheet either. This is a spectacular balance sheet for a small-cap or for any cap.

My Thoughts

The business is growing. The balance sheet is strong. There is definitely something here to see.

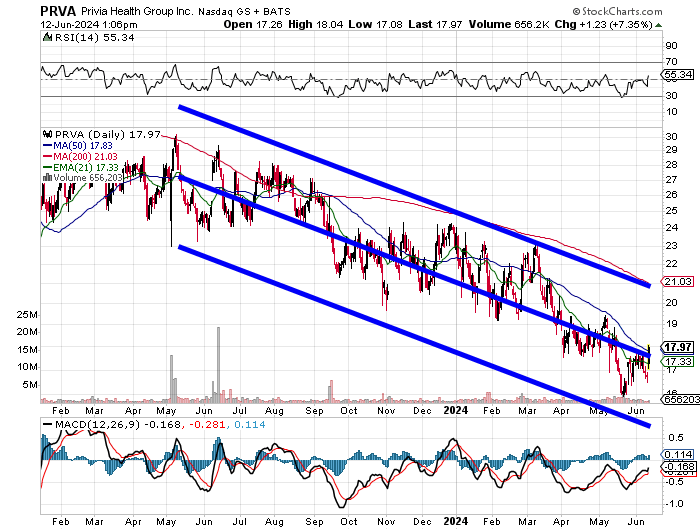

Readers will see below that PRVA has been mired in a more than one-year long descending price channel:

I would not jump on board this name Wednesday, up around 7%. I will say this though. I will be watching to see if that 50-day simple moving average (SMA) holds. If the stock holds the 50-day line, which is currently $17.83, then we may have ourselves a ballgame.

The short-term target would be the 200-day SMA at $21 but let's not get ahead of ourselves. First, we see if the stock holds that thin blue line. This may be where the descending price channel finally turns into something else.

More Stocks Under $10:

- I've Got My Eyes on an Apparel Group After Surprise Profit Report

- This Iconic Retail Chain Got Rocked, But Absurd Yield Is Still Possible

- Time to Get Fired Up About Rocket Lab

At the time of publication, Guilfoyle had no positions in any securities mentioned.