Who the Heck Is Netgear and Why Is it Up Big After Settlement?

This networking technologies provider is up more than 33% following a legal settlement with TP-Link and there might be opportunity to buy.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As I put pen to paper this morning, or shall I say, "fingers to keyboard," I see that Netgear NTGR is up 33% on Thursday (so far) on earnings news, despite what looks like some tough numbers. Terrific.

You'll find that Thursday's pop is more about a legal settlement as it is about anything else. I just have one question.

Who the Heck Is Netgear?

Netgear Inc. is a San Jose, California-based provider of networking technologies and connectivity services for consumers, businesses and other providers. The firm operates through two segments. The Connected Home segment is aimed at consumers and provides high-performance, and easy to use networking solutions such as Wi-Fi 6, 6E and 7 Tri-Band, mesh systems and routers, 4G/5G mobility and subscription services.

The Netgear for Business segment provides solutions for commercial networking, wireless LAN, audio and video over Ethernet for Pro AV applications, as well as security and remote management. The firm operates in three geographic regions: the Americas; Europe, Middle East and Africa (EMEA); and Asia Pacific (APAC).

Earnings

For the firm's fiscal second quarter, which ended June 30, 2024, Netgear reported an adjusted EPS of $-0.74 (GAAP EPS: $-1.56) on revenue of $143.9 million. The adjusted bottom-line number, despite still representing a loss, did beat Wall Street by more than a nickel. The bottom-line print beat Wall Street as well, despite reflecting a year-over-year contraction of 12.6%. The adjustments made were made for the purposes of building litigation reserves, stock-based compensation and restructuring charges. Just super.

Operations

This is going to get messy. As the firm was suffering a 12.6% decrease in revenue generation to $143.9 million, the cost of revenue contracted 3.7% to $112.077 million.

This left a gross profit of $31.823 million (-34%), as gross margin dropped from 29.3% to 22.1%. Total GAAP operating expenses increased 12.6% to $78.682 million, leaving a GAAP operating income/loss of $-46.859 million, down huge from the year-ago comp of $-21.648 million. This takes the GAAP operating margin from -13.2% down to -32.6%. I kid you not.

After accounting for other income/losses and taxes, the firm's GAAP net income/loss printed at $-45.175 million, down from $-18.65 million for the year-ago period. This worked out to a GAAP EPS of $-1.56 per diluted share, down from $-0.63 a year ago. On an adjusted basis, net income/loss hit the tape at $-21.443 million, down from $-8.355 million a year ago.

Guidance

For the current quarter, Netgear sees net revenue of $170 million to $180 million, which is an increase from prior guidance of $160 million to $175 million. Both GAAP and adjusted operating margins are expected to remain quite negative.

News

Netgear has entered into a settlement agreement with TP-Link System and as per the terms of the agreement, all pending litigation between the parties will be dismissed or not further pursued. Additionally, Netgear has received a $135 million payment as consideration for the same.

Fundamentals

For the first six months of the year, Netgear generated operating cash flow of $35.635 million. Out of that came capex spending of $4.817 million, leaving free cash flow of $30.818 million. Out of that number, the firm repurchased $21.444 million worth of common stock. Netgear does not pay out cash dividends to shareholders.

Netgear ended the quarter with a cash position of $294.339 million and inventories of $188.936 million, bringing current assets to $657.572 million. Current liabilities add up to $253.028 million, including deferred revenue (not a true financial obligation) of $28.682 million and no short-term debt. That leaves the firm with current and quick ratios of 2.60 and 1.85, respectively. These are healthy numbers. Much healthier than one might expect, given the performance of the business.

Total assets amount to $754.086 million. This does include goodwill of $36.279 million, but everything else is tangible. Total liabilities less equity comes to $294.687 million. These guys have no debt on the books. This firm is very sound fundamentally below what looks like a turbulent surface.

My Thoughts

The business remains a long way from profitability. That said, cash flows are positive, and the balance sheet is extremely well-managed. Heck, the firm has a fat cash position and no debt. Unfortunately, I am not so sure that the firm is as investable as it would be if it were a bit closer to profitability. On the other hand, there was/is not much short interest in the name, so this demand for the shares is organic.

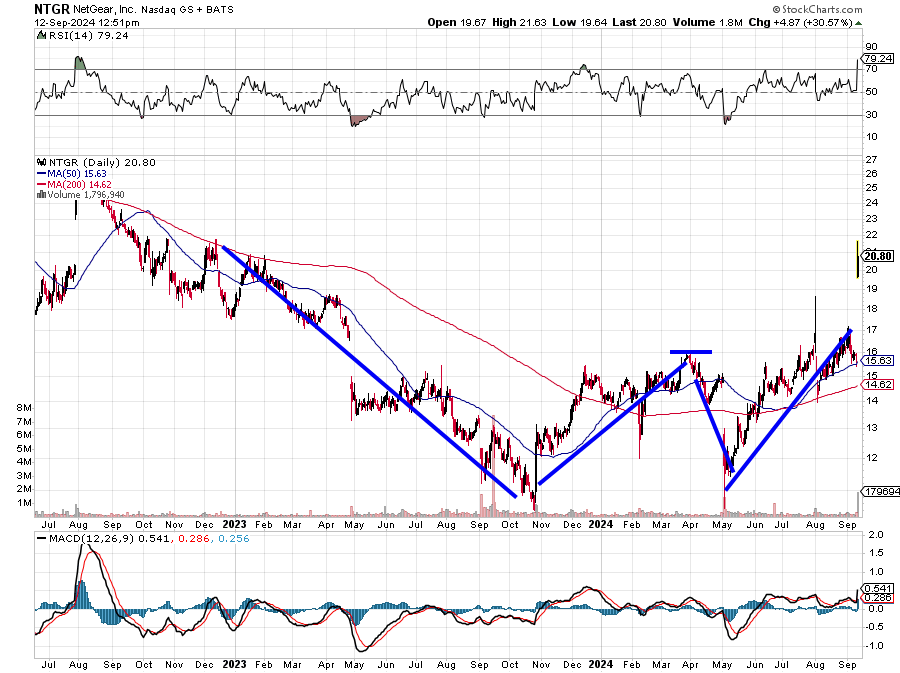

Readers will see that over a two-year period, a large double-bottom reversal pattern had formed with a $16 pivot. On Thursday morning, on the above news, NTGR broke through its pivot. If I were long the stock based on the fundamentals, my target price would be an even $20. The stock is trading just below $21. Therefore, while I am inclined to sit this one out, I would be more likely to play this name as a short-term short idea as the gap created this morning, in my opinion, will likely at least partially fill over the next few days.

At the time of publication, Guilfoyle had no positions in any securities mentioned.