Who the Heck Is Ardmore Shipping?

There's a lot for investors to love about the small-cap maritime shipping company.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Have you heard of Ardmore Shipping ASC?

You may not have. Ardmore Shipping is a small-cap, global maritime shipping company headquartered in Bermuda and listed at the New York Stock Exchange. Ardmore's business is the ownership and operation of product and chemical tankers in worldwide trade. The company provided seaborne transportation of petroleum and chemical products to oil majors, national oil companies, oil and chemical traders and chemical companies with a fleet of 25 mid-sized tankers. The firm has the global network to support its seafarers and deliver shipping services to its customers.

Have You Seen Shipping Prices?

Earlier this week, CNBC reported that ocean freight rates could approach COVID-era peak pricing and potentially remain elevated into 2025. According to CNBC, spot ocean freight prices from the far east to the U.S. west coast have "popped" some 36% to 41% month over month. Last week, Sea-Intelligence issued a note projecting that Asia to Europe spot prices could surpass $20,000 with the increase in nautical miles shipped as many lines still need to avoid the Red Sea. Last week, Hellenic Shipping News reported that the tanker market is not only likely to remain quite profitable into the medium-term but perhaps out into and beyond the year 2030.

In his musings this morning, Bleakley's Peter Boockvar wrote: "The Shanghai to Rotterdam route saw the box price rise another $455 week over week to $7,322, higher for a 10th-straight week."

That's up 144% over that 10-week time frame. Boockvar also wrote that the Shanghai to Los Angeles route saw an increase of $232 over last week to $6,673. This was an eighth-straight weekly increase as that price has roughly doubled over two months.

Just an FYI: These cargo prices are higher as are air cargo prices. While the Fed and other economists talk about getting core services inflation under control and how consumer level inflation will continue to work its way toward the Fed's 2% target, few seem to understand that rising shipping prices likely spell the end of benign goods inflation and that this will offset gains against inflation made elsewhere.

Earnings

Back in early May, Ardmore Shipping reported the firm's first quarter financial results. The firm posted a GAAP of $0.92 on revenue of $106.3 million. Both of those numbers beat Wall Street, but revenue generation did contract by 10.1% year over year. The firm also increased its quarterly dividend to $0.31 at that time from $0.21. The stock soared in response. As of this morning, ASC yields 5.5%.

The firm is expected to report its second quarter in late July. Expectations are for GAAP EPS of $0.91 on revenue of anywhere between $74 million and $93 million as there are only five analysts covering the stock and there really is no true consensus.

Fundamentals

Over the trailing 12 months (as of the March quarter), Ardmore generated operating cash flow of $152 million. Out of that came capex spending of $33.2 million, which left free cash flow of $118.8 million. The firm did not repurchase any stock for its treasury but did pay out $37.5 million in cash dividends to shareholders.

As of that March quarter, Ardmore had a cash position of $48.6 million on the books, with inventories of $11.6 million and current assets of $143.9 million. Current liabilities add up to $73.7 million — that includes no short-term debt. These numbers are good enough for current and quick ratios of 1.95 and 1.79, which is really strong for a firm in this business, never mind a small-cap.

Total assets amount to $740.1 million. The firm claims no intangible value, which is appreciated. Total liabilities less equity comes to just $99.1 million, including $23.1 million in long-term debt. Given that the firm has enough of a cash position to pay this debt-load twice over, this balance sheet is a serious strength.

Last Week...

Peter M.E. Christensen, who is a five-star rated analyst at Cleaves Securities, reiterated his "buy" rating on ASC with a $27 target price. That was an increase from $24 and would be up 19.4% from the last sale I saw as I type.

My Thoughts

I like a lot of what I see: Business that will benefit from inflation. Nice cash flows. Strong balance sheet. Handsome dividend. Profitable, without doing all sorts of adjustments.

This is an impressive firm, and despite its recent earnings/dividend related pop, still trades at just eight times forward-looking earnings. Oh, and debt is not a problem. Nicely run operation.

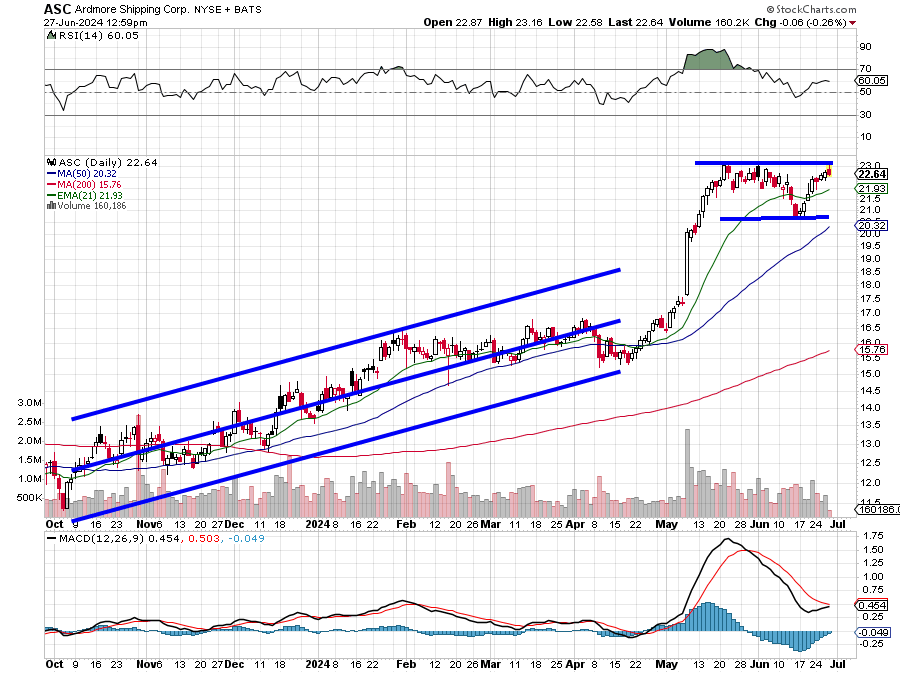

Readers will see that ASC had already been in an ascending price channel from last October into early May, when it popped. That run is over, and the stock has gone into a basing period of consolidation, which it is trying to break out of right now. Relative strength is close to neutral, but the daily MACD looks like it could reposture bullishly in the near-term future. The histogram of the nine-day EMA appears just about ready to go positive, while the 12-day EMA appears close to attempting a crossover of the 26-day EMA. I think this is a stock I could invest in for at least the medium-term. I'll wait until this piece is public information before taking action.

- Target Price: $28

- Pivot: $23.50

- Add: close to 21-day EMA ($22-ish)

- Panic: Loss of 50-day SMA ($20-ish)

At the time of publication, Guilfoyle had no positions in any securities mentioned.