Here's Where I'd Trade Peloton Shares

The exercise brand is popping after a disclosure revealed David Einhorn's position, but is there opportunity for profit?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Anyone else notice that pandemic-era darling Peloton Interactive PTON is popping on Thursday morning?

As I set about typing out this piece, the shares are up something like 7.8%. Before that heartbeat in your chest skips a beat, understand that this means that the stock is up a rough $0.22. That said, who doesn't like working up a sweat? Who doesn't like feeling spent after a solid session of intense physical exercise?

The reason behind Peloton's Thursday run is that the name showed up on DME Capital's Form 13-F. Hedge fund veteran David Einhorn is the name behind DME Capital, and that fund apparently acquired 6.8 million shares of PTON during the second quarter of this year. DME, as of June 30, 2024 anyway, was one of Peloton Interactive's 15 largest shareholders.

This is not necessarily new news, as it had previously been reported by the financial press that Einhorn had been investing in the workout equipment and streaming service provider.

Twice in One Week

This is the second time this week that Peloton made my news feed. On Tuesday, it was announced that Peloton had entered into a partnership with Alphabet's GOOGL Google Fitbit to offer premium members access to premium online classes.

Fitbit's premium members will be able to take exercise classes on Peloton's streaming platform with at least some classes available to these Fitbit users that are only otherwise available to Peloton's premium members. That was a mouthful, but I think you get what I'm trying to say. Peloton members will also receive special offers to purchase a Google Pixel Watch and/or a Fitbit Charge 6 as part of the agreement. For those scratching their heads, Alphabet acquired Fitbit back in 2019.

Earnings

Peloton is set to report the firm's fiscal fourth quarter results a week from Thursday, on August 22, 2024. Consensus is for the firm to report a GAAP EPS of $-0.17 on revenue of $628 million. This would compare to $-0.68 on $642 million for the year-ago comparison while reflecting a year-over-year sales contraction of about 2%. This will likely be a 13th consecutive quarter of negative earnings and a tenth consecutive quarter of year-over-year revenue contraction. That said, the pace of that contraction is slowing, and there is just a smidge of sales growth projected for the current (not the about to be reported) quarter. The firm is crawling closer, though not that close to profitability as well.

Race Against Time?

The fundamentals are not good. Obviously. That said, management has set itself up to last for as long as possible, while waiting either for the business to improve significantly or for a white knight to show up. For the trailing 12 months ended this past March, Peloton generated operating cash flow of $-154.2 million and free cash flow of $-185.8 million. The 12 month prior to that, it was uglier. Operating cash flow of $-387.6 million and free cash flow of $-470 million. The year before that? Don't ask. Free cash flow for that period came to almost $-2.4 billion with a "B."

At that same time, Peloton held a cash position of $794.5 million and inventories of $354.4 million. Are those inventories worth that number? I have my doubts. The firm has intelligently pushed its entire debt load into the distant future, so there is no need for any new refinancing anytime soon. The long-term debt load is a bit on the daunting side at $1.682 billion. The firm did have $101.3 million in deferred revenue on the books at that time. Maybe that took care of some of those inventories.

Tangible book value as of last March, ran at $-1.75 per share, so the shares, cheap as they were, were not inexpensive.

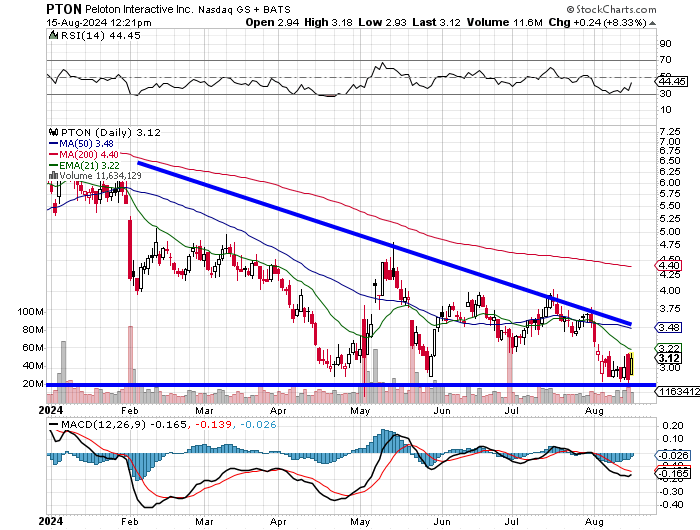

Readers can see that the shares have continued to come in this year. The daily MACD is still bearish, but relative strength has meandered its way back up to a "neutral" stance. The overbearing technical pattern present is a descending triangle, which is bearish in nature, but I have seen on rare occasions, the expected breakdown show up as a breakout.

Understand This

I do not think this stock is investable, but apparently Einhorn does. The chance that he knows more about this company than I do is greater than the chance that I know more about this company than he does.

This name is a purely speculative play, meaning that it's risky, an investor might lose their principal investment. All of it. Is PTON trade-able? Yes, I think it is and will be for at least a while. Would I chase the stock today? No, let the keyword reading algorithms do that. They are responding to news that was not really new.

That said, after the algos have had their fill, I think I'd be willing to trade the shares from the long side starting at $2.90. I would suggest a short position on this pop, but 22% of the entire float is already held in short positions. The possibility of a squeeze is just too great. That's another reason to extend a wee bit of risk this way on the long side, but on a "down" day.

At the time of publication, Guilfoyle had no positions in any securities mentioned.