UPS Is Still a Better Company Than FedEx: Here's When to Trade It

The balance sheet is not fortress-like but it gets a passing grade.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I think it's good news if on Tuesday you're long United Parcel Service UPS. The stock was trading lower after having traded higher. I admittedly have no position in UPS nor in rival FedEx FDX as I had not seen these stocks as strong plays in an economy I had expected to weaken.

Did the economy weaken? Not according to GDP. Definitely, according to GDI and many other metrics. Regardless, I was right to have stayed away from UPS despite the fact that I am a long-time fan of CEO Carol Tome who rose to fame as the CFO at Home Depot HD. Tome was considered to be one of the great CFOs in American business while at Home Depot.

United Parcel Service will host the firm's Investor and Analyst conference today (Tuesday) at the firm's hub in Louisville, Kentucky. A webcast of the day's events will be made available at the firm's website. During today's conference, UPS will highlight the firm's strategic initiatives going forward that will be meant to drive incremental growth. The firm will also illustrate its path toward a reduced cost structure.

The firm has put into print a number of financial targets for the year 2026. For that year, UPS is targeting consolidated revenue generation of $108B to $114B. For the sake of comparison, consensus view for the firm's revenue for 2024 is for a little more than $93B and for 2025, about $97.5B.

The firm sees an adjusted operating margin of 13%. For the fourth quarter of 2023, UPS posted an adjusted operating margin of 11.2%. The firm is targeting domestic package segment adjusted operating margin of more than 12% and international package segment adjusted operating margin of between 18% and 19%. Free cash flow is seen at $17B to $18B for 2026. For 2023, free cash flow amounted to $5.08B. Finally, the firm would like to peg capital spending for 2026 at 5.5% of revenue generation.

The Current Quarter

UPS is set to report its first quarter financial results in about a month. Currently, expectations are for a GAAP EPS of about $1.54 or an adjusted EPS of $1.58 on revenue of $22.15B. This would compare, not all that well with year ago comparisons of $1.57 on $23.01B. 28 of 29 analysts (of all ratings) that I can find that cover the stock have reduced their projections for adjusted profitability for this quarter since the quarter started. So, an upside surprise would be nice, but we're not holding our breath.

At the moment, UPS trades at less than 19 times forward looking earnings, which is less than the S&P 500, but considerably more than FedEx's 13 times. In my opinion, UPS is a better company than FedEx, but do not underestimate Raj Subramaniam as CEO. For the first time in a long time, both UPS and FDX have formidable CEOs. UPS also pays shareholders an impressive $6.52 per share per year just to stick around. That's a dividend yield of 4.16% that may not matter to traders. Definitely matters to investors.

UPS ended up shelling out $5.372B in maintaining that dividend over the past twelve months. As long as that's just a portion of free cash flow, that makes sense. The firm also spent $2.25B repurchasing its own shares. I would say that this expenditure could be put on hold in order to reduce debt or invest a higher percentage of free cash in the business. Tome seems to have figured this out for herself though as none of that $2,25B was in the fourth quarter.

Balance Sheet

As of year's end, UPS had a cash position of $6.072B and inventories of $935M, making for current assets of $19.413B. Current liabilities added up to $17.676B, which included $3.244B in shorter-term debt. That left the firm at that time with a current ratio of 1.09 and a quick ratio of 1.05. Not fortress-like, but at least a passing grade.

Total assets amount to $70.857B of which little more than 10% is in the form of goodwill and other intangibles, which is acceptable. Total liabilities less equity comes to $53.543B. That includes another $18.548B in debt labeled as longer-term. The firm has a lot of debt, but not so much that it cannot be serviced and even reduced through the maintenance of elevated free cash flows. We know that this is a stated goal of the firm.

The Stock

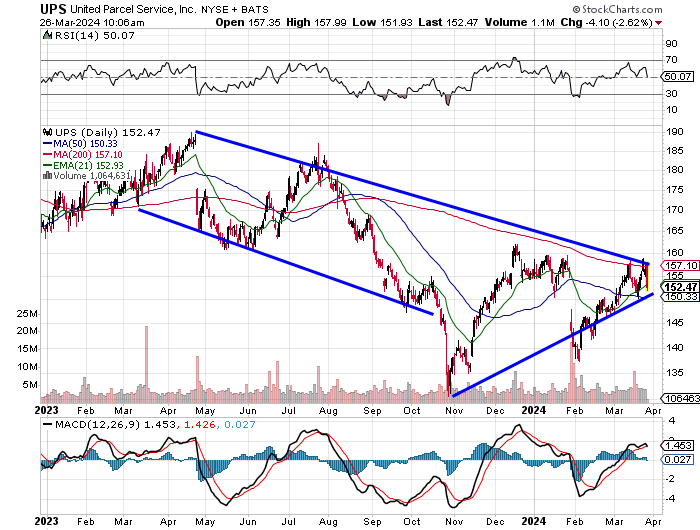

Readers will see that UPS has been making lower highs since last spring. Up until October, the stock had also been making lower lows, forming a descending price channel. What do we know about descending price channels? They end up (after a while sometimes) looking like patterns of bullish reversal. From November up to the present, UPS has been making higher lows while continuing to make lower highs.

That makes what we have seen since October a symmetrical triangle. What do we know about symmetrical triangles? They often end up closing and taking the stock into an explosive move one way or the other. Is today that event? Are next month's earnings?

What do I think? The stock has just pierced its 21-day EMA (exponential moving average) to the downside. I'm watching the 50-day SMA (simple moving average). Support there, I think I may nibble. Retake the 21-day line? I may nibble there. Lose the 50-day line? Then I'm out of here, because the stock would be likely to make a lower low in that case.

For those looking to play those earnings, the UPS $150 April 26th puts are currently worth about $3.50. If one does get tagged, the long position's net basis would be $146.50. Not bad for a stock trading with a $152 handle today.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.