United Airlines Soars Despite Boeing Delays: Here's the Trade

Cash flows were robust. The balance sheet is decent, maybe better than decent. Guidance is solid.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday evening, United Airlines UAL released the firm's first quarter financial results.

For the three-month period ended March 31st, United Airlines posted an adjusted EPS of $-0.15 (GAAP EPS: $-0.38) on revenue of $12.539B. As tough as those numbers might appear to the human eye. beauty is in the eye of the beholder. A lot of folks beheld United Airlines overnight and still are beholding now.

Both the top and adjusted bottom line results beat Wall Street's expectations. Between that and the guidance provided, Wall Street is suddenly fired up about UAL. Additionally, the firm informed in the press release, that if not for the negative impact of the grounding of the Boeing BA 737 Max 9 aircraft, which came to about $200M, the firm would have recorded a surprise profit for the quarter.

For the quarter reported, capacity was up 9.1% from the year ago period. The firm also achieved the second best on-time first quarter departure ratio in the firm's history. Additionally, the firm achieved the second best on-time average departure and arrival ratios among US airlines for the second straight quarter.

UAL also set the record for the highest Q1 consolidated seat factor ever at 84.1%, with March setting a March record. Seat factor for those who do not know, is the number of revenue passenger miles divided by the available seat miles. Lastly, the firm set the company record during the quarter for the greatest number of days carrying more than 500K people every in a first quarter at 16.

Operations

Passenger driven revenue, which is more than 90% of the business, expanded 10.1% year over year, as cargo driven revenue contracted 1.8%. As overall revenue grew 9.7%, GAAP operating expenses increased 8.4% to $12.44B on an operating margin of 0.8%. Fuel costs in particular decreased 6.9%, though employee compensation increased 18.4%. This left GAAP operating income of $99M, up from $-43M for the year ago comparison. Adjusted operating income increased to $112M from last year's $-29M.

After accounting for interest, taxes and unrealized investments, the firm was left with a GAAP net income/loss of $-124M, which works out to $-0.38 per share. Once adjusted, net loss printed at $-50M versus the year ago comp of $-207M. This works out to the $-0.15 per share that you probably saw in this morning's headlines.

Guidance

For the current quarter, United is projecting an adjusted EPS of $3.75 to $4.25, which easily beat Wall Street projections, pulling the low end of the range above consensus view that was for about $3.71. The firm also reiterated prior full year guidance for an adjusted EPS of $9.00 to $11.00. This took the midpoint of the range well above Wall Street's expectations that were for a rough $9.43 or so.

Additionally, United cut the firm's expectations for aircraft delivery this year to just 61 new narrow body planes from the 101 that had been projected at the start of the new year. United removed the Boeing 737 Max 10 from its forward-looking fleet plan and will convert some of those Max 10's into Max 9's. as well as lease more aircraft from Airbus EADSF in 2026 and 2027.

Fundamentals

For the quarter, United generated an operating cash flow of $2.847B. Out of that number came $1.366B in Capex spending, leaving free cash flow of $1.481B, which was up 34.7% from Q1 2023. The firm did not return cash to shareholders during the quarter but did pay down more than $5B in long-term debt.

Turning to the balance sheet, UAL ended the period with a cash position of $13.992B and current assets including aircraft replacement parts of $18.696B. Current liabilities add up to $24.764B including $3.958B in shorter-term debt. Now, this leaves the firm with a current ratio of 0.76, which is fairly awful.

However, among the listings under current liabilities is $9.601B in advance ticket sales. I believe that tech firms call this unearned revenue and unearned revenue is not a true financial obligation. Therefore, once we adjust United's current ratio for these ticket sales, the current ratio rises to 1.23, and that number does pass muster.

Total assets amount to $71.902B including goodwill and other intangibles of $7.244B. At little more than 10% of total assets, this is no concern whatsoever. Total liabilities less equity comes to $62.714B, including long-term debt of $23.059B. Is this a great balance sheet? No. Is this a better balance sheet than I thought I was going to find when I started researching for this article? Most definitely.

Wall Street

I can only find two highly rated sell-side analysts that have opined on UAL since last night. Both are rated at five stars by TipRanks.

Stephen Trent of Citigroup reiterated both his "buy" rating and his $71 target price, writing "Overall, these results and guide could bring at least some relief to what we would characterize as the oversold situation in United's shares."

Secondly, Brandon Oglenski of Barclays reiterated both his "buy" rating on UAL as well as his $60 target price.

My Thoughts

The earnings are really better than expected. Heck, if not for Boeing's never-ending string of embarrassing debacles, this firm would have posted a profit. That said, cash flows were still robust. The balance sheet is decent, maybe better than decent. Guidance is solid.

Lastly, the firm is showing a seriousness in improving its underlying fundamentals by paying down huge chunks of debt and refraining for now from returning cash to shareholders. I like a lot of what I just wrote.

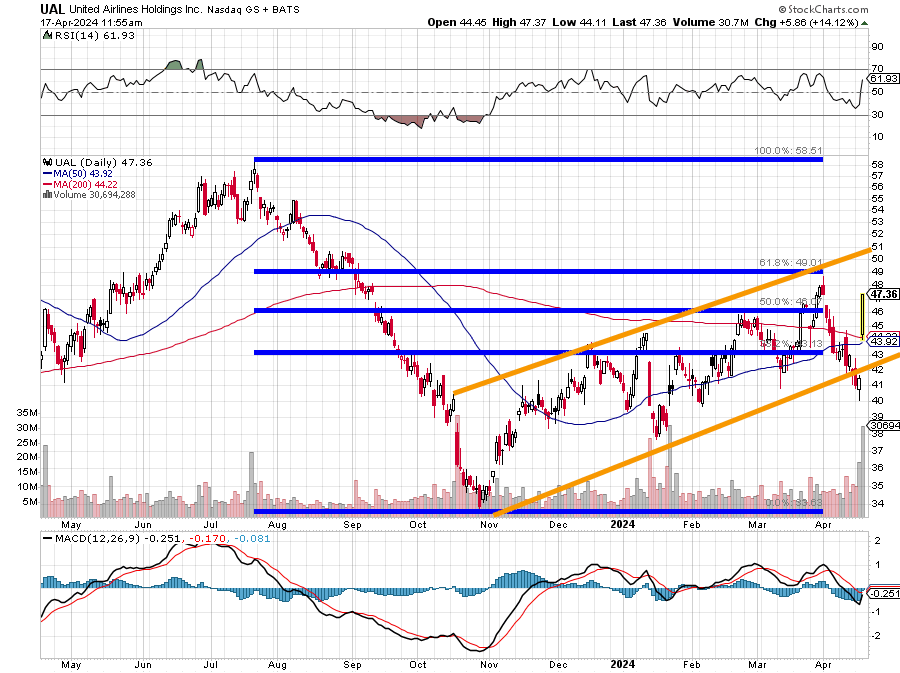

Readers will see that UAL met with resistance at a precise 61.8% Fibonacci retracement of the July 2023 through late October 2023 selloff. From that low, the stock has enjoyed trading higher in a well-defined ascending price channel.

This morning, the stock has retaken both its 50-day and 200-day SMAs (simple moving average), which will force institutional investors to increase long-side exposure. Relative strength and the stock's daily MACD (moving average convergence divergence) are suddenly less awful looking than they were on Tuesday.

My opinion is that this stock is okay to get long between the last sale and the 200-day SMA (currently $44). Should this level be treated as a pivot? We'll know if it holds because the funds stepped in and held the line.

Should that be the case, I think a fair target price would be $55, leaving plenty of room for the funds that bought today to take profits close to the upper trendline of this price channel.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.