Ulta Beauty Suddenly Ain't So Beautiful: How to Trade It

The quarterly results were fine. The guidance provided? Not so much.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Hair care, cosmetics and salon services giant Ulta Beauty ULTA released the firm's fiscal fourth quarter results on Thursday evening. The results were fine. The guidance provided? Not so much.

For the three-month period ended February 3rd, Ulta Beauty posted a GAAP EPS of $8.08 on revenue of $3.554B. These top and bottom-line numbers both beat Wall Street's expectations, while the sales print was good enough for year over year growth of 10.1%.

Comp sales were up 2.5% from the year ago comp, which was a sharp drop off from the year ago growth of 15.6% from the comparable period two years ago. This 2.5% increase (which fell short of expectations for 3% growth) was composed of a 4.5% increase in total transactions, but a 1.9% contraction in average ticket size, which if there is nothing wrong with the company, is an obvious sign of consumer distress.

Operations

As revenue increased 10.1%, the cost of those sales grew 9.9% to $2.214B. This left a gross profit of $1.341B (+10.6%) on a gross margin of 37.7%, up from 37.6%. Normal operating expenses increased 7.6% to $820.4M. After tacking on $3.1M in pre-opening expenses, operating income printed at $517.1M (+15.7%) as operating margin improved from 13.9% to 14.5%. After accounting for interest and taxes, net income landed at $394.4M (+15.9%), which is how we get to $8.08 per diluted share.

Guidance

For the full fiscal year 2024, Ulta is expecting to generate $11.7B to $11.8B, with Wall Street looking for $11.7B. That was conservative ($11.7B would amount to growth of just 4.4%), but okay. The real kick in the pants came from expectations for comp sales of 4% to 5%, down from 5.7% for the past year and for operating margin of 14% to 14.3%, down from 15% for the past full year.

This would all lead to full year GAAP EPS of $26.20 to $27.00. That brings not only the mid-point of the range, but the high end of said range below the $27.05 or so that analysts had been looking for.

Fundamentals

For the full year, Ulta generated operating cash flow of $1.476B. Out of this number came Capex spending of $435.3M, leaving free cash flow of $1.041B, down 10.9% from the year prior. Out of that number, the firm repurchased $995.7M worth of common shares for the corporate treasury. Ulta does not pay its shareholders a dividend.

It should be noted that earlier this week, Ulta's board of directors approved a new share repurchase authorization of $2B, replacing the old authorization that was down to less than $100M. This new authorization has no expiration date, but the firm did project repurchasing about $1B worth of stock or half of this authorization during this fiscal year.

Turning to the balance sheet, Ulta ended the period with a cash position of $766.6M and inventories of $1.742B (+8.7% y/y). This puts current assets at $2.837B. Current liabilities add up to $1.658B including no short-term debt and $436.6M in deferred revenue. That puts the firm's current ratio at a robust 1.71 and once adjusted for deferred revenues... an even more impressive 2.32.

Now, we don't generally hold retailers to the same standards for quick ratios as other types of businesses. That said, Ulta's inventories are up rather significantly from a year ago, and in this environment, could have trouble retaining stated valuation. Ulta's quick ratio now stands at 0.66 an if adjusted for deferred revenue... 0.89. Even with increased inventories, these ratios are not bad at all for a large retailer.

Total assets amount to $5.707B, including just inconsequential entries for goodwill and other intangibles. Total liabilities less equity comes to $3.428B, that includes plenty of leases, but no long-term debt whatsoever. This balance sheet, outside of the growing size of its merchandise inventories, is golden.

Wall Street

Since these earnings were released last night, I have come across 12 highly rated (4+ stars at TipRanks) analysts that have opined on ULTA. Among the 12 analysts, there are nine "buy" or buy-equivalent ratings and 3 "hold" or hold-equivalent ratings. One of the "buys" did not set a target price, so we are working with just 11 of those.

The average target price across these 11 analysts after allowing for changes is $604.09 with a high of $665 (Korinne Wolfmeyer of Piper Sandler) and a low of $540 (Anthony Chukumba of Loop Capital). Once omitting those two as potential outliers, the average target across the remaining nine analysts rises just slightly to $604.44. For those interested, the average "buy" target was $620.63, while the average "hold" target was an even $560.

Opinion

Performance has been consistently outstanding for this retailer that for so long seemed immune to the issues that other retailers often face. Now, suddenly, Ulta Beauty seems very unsure of itself, and Wall Street is punishing that lack of confidence.

The cash flows are in slight decline, but still quite robust. I thought the authorization for another huge buyback was a little misplaced. Sure, it is still considered returning capital to shareholders, but what if half of that authorization was instead targeted at cash dividends instead of buybacks?

That would make the shares more attractive and maybe this morning's beat-down for the stock would be less severe. The balance sheet is in great shape overall.

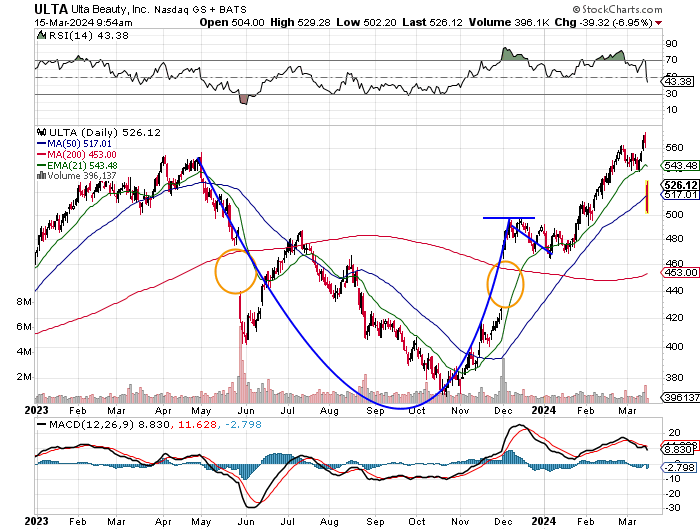

I have not been in nor have I covered ULTA in quite some time, so I don't have a recent chart in my inventory to update for you. So, we start from scratch.

Readers will see that ULTA created a cup with handle pattern that stretched from last April into year's end, developing a pivot point at $497. That put the stock's target in my opinion at $571, which the stock exceeded ($574 high) on Thursday before selling off ahead of earnings.

Folks, plain and simple, this stock has done everything that in my opinion, it was supposed to do technically speaking. Shareholders were even given a chance to reduce exposure at target.

What's happening today, is the loss of the profit takers and the swing traders who may in many cases be the same folks. There has been a decent enough battle at least in the early going at the 50-day SMA (simple moving average), which means that the professional money is not so sure they want out. That's possibly quite positive.

If I were long these shares, I would reduce upon the loss of that 50-day line, with an intent to repurchase later on at a lower price. The 200-day SMA is probably too much to ask for.

That said, $450 puts expiring in three months (June 21st) are still worth about $6 and that might not be such a bad sale. The investor either pockets $6 or ends up long at a net $444, for a stock still trading at $527. A risk averse trader could turn the sale of that put into a bear put spread and buy protection at a lower strike price with the same expiration date in order to control the downside.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.