Two Walmarts Are Better Than One

Walmart stock hits another all-time high. Here’s why it can go even higher.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I had a mild disagreement with a colleague over Walmart WMT and its liftoff to a new all-time high.

Here’s his argument: At over 30x earnings, Walmart shares are overvalued. The company’s growth rate is around 5%. It’s just one of many stocks that have been carried to unprecedented and unjustifiable heights due to funds piling into large-cap names.

He’s not wrong. When most of us look at Walmart, we see a slow-growing behemoth.

However, it might be helpful to think of Walmart as two separate companies.

One Walmart — the Walmart everyone knows — consists of brick and mortar stores. Growth here isn’t spectacular, but with many consumers trading down to cheaper goods due to inflation, this version of Walmart should hold its own against its competitors. .

This part of the company isn't terribly exciting, but it is the world’s largest retailer, and that familiarity alone creates a competitive advantage. Let’s call it Walmart1.

The second, lesser-known version of Walmart only exists online. It’s the world’s second largest online retailer, behind only Amazon AMZN.

Despite its size, this company is growing at a roaring 22% clip, much faster than Amazon. That growth has accelerated in recent quarters. Let’s dub this company Walmart2.

If the U.S. economy goes into recession, Walmart1 should perform well. The company is famous for low prices. Walmart1 sells many basic products that consumers will continue to purchase regardless of the state of the economy.

Walmart2, which exists only online, enjoys all the positive qualities of Walmart1. There’s an obvious advantage of lower overhead, but perhaps the biggest factor in Walmart2’s favor is its potential for growth.

Last year, Amazon racked up a total of $412 billion in ecommerce revenue. Meanwhile, Walmart topped $100 billion in annual ecommerce sales in fiscal 2023. It was the first time Walmart (in this case, Walmart2) topped the $100 billion mark.

Not only is Walmart2 growing rapidly, it exists in a sector that is also growing rapidly.

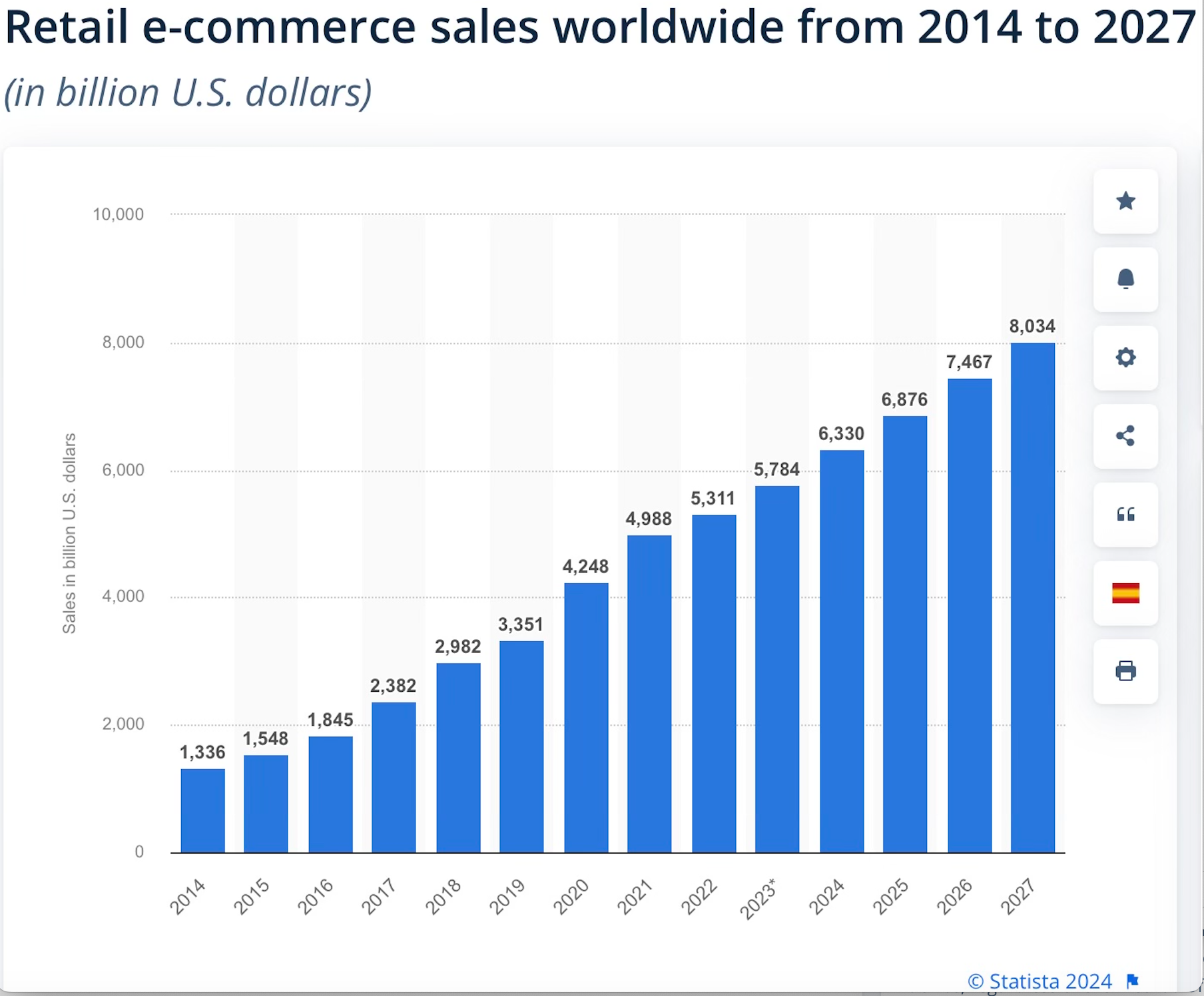

E-commerce sales in 2023 hit an estimated record $5.8 trillion. That figure is expected to top $8 trillion by 2027, according to statista.com. That represents a gain of about 39%.

There isn’t much to say about Walmart’s chart, other than that it’s a steady winner. Walmart’s 50-day (blue) and 200-day (red) moving averages demonstrate the stock’s steady, upward trajectory.

Walmart gained 6.58% on Thursday. Year-to-date, the stock has gained 20%. Walmart has gained 37.9% over the past year, and 94.3% over the past five years.

Like my friend, many folks are dismissive of Walmart, because they only see one side of the company. They see the big blue stand-alone store, and they forget that there's more to Walmart's story.

It's an easy mistake to make. The exciting side of Walmart is easy to miss, but it's the incredible potential of that side of the company that should continue to make this stock a winner.

At the time of publication, Ponsi was long WMT.