ServiceNow Downgrade and Weakness Spell Opportunity

Here's why and how I'm taking advantage of the stock's situation amid Difucci 'Sell' call.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

ServiceNow NOW has long been a cloud technology and generative AI favorite on the software side. I was a fan of the name prior to Bill McDermott's appointment as chief executive in November 2019, but it was clear to see that hire as a match made for investors. McDermott's stellar performance running SAP's SAP businesses for the decade-plus prior had been well known.

Over the weekend, ServiceNow was downgraded by the highly respected analyst John Difucci of Guggenheim, who is rated five stars by TripRanks. Difucci took NOW from a "Neutral" to an outright "Sell." Difucci, remember, is ranked in the Top 30 of the 8,932 sell-side analysts tracked by that service. At this time, Difucci has set a target price of $640 on these shares that he had downgraded from "Buy" to "Neutral" this past April.

The stock has sold off sharply ahead of Monday morning's opening bell. Astute readers may have noticed that Michael Turrin of Wells Fargo reiterated his "Buy" rating on NOW this morning, while increasing his target price from $900 to $920. Why that does not appear to be having much of a positive impact on the price of the shares is Turrin's ranking, which is not at an elite level. Turrin is rated at one star out of five by TipRanks.

What Difucci and his team at Guggenheim are concerned with is not the just completed quarter of ServiceNow's performance but looking out over the rest of the year. Guggenheim believes that Q2 will look fine when those numbers are released on July 24th. However, the second half of the year could get rough. The team at Guggenheim appreciates that ServiceNow may be expecting an uptick in gen AI business through the second half of the year, but that Guggenheim's own field work implies that this increased subscription business may be pushed out into 2025. Guggenheim sees ServiceNow partner checks as still positive, but less so than what they consider usual.

My Sale, Looking to Earnings

Just so we are clear. I sold some ServiceNow stock about three weeks ago. Great sale. Or so I thought. The stock went higher. I am still long the shares of this name. It's still a Top 10 holding of mine, it would have been neck and neck with CrowdStrike CRWD and Microsoft MSFT for the No. 1 position had I not reduced that exposure. Should I buy back at least some of the shares that I sold now that NOW will experience a dip in price? That's exactly what I'm wondering. It looks like Palantir Technologies PLTR will experience a nice opening, so I can camouflage this hit to my profit/loss ratio and not really "see" it if I don't want to.

Second-quarter earnings land after the closing bell on July 24. Wall Street is looking for an adjusted earnings per share of $2.84 on revenue of $2.6 billion. That would work out to earnings growth of 19.8% on revenue growth of roughly 21.4%. This would be in line with, to slightly above the firm's trends over the past year.

What will be scrutinized will be any updates made to Now's full year guidance for subscription revenue of $10.56 billion to $10.575 billion, operating margin of 29% and free cash flow margin of 31%. Any downside moderation made to those projections will reinforce what the Guggenheim team is seeing and will not be taken well by investors. Interestingly, of the 27 analysts I can find that cover this stock, 12 have increased their second-quarter estimates, while 15 have decreased their estimates. Keep in mind, that NOW often reacts either negatively or not at all upon earning releases before what has been upside momentum for some time now, re-manifests itself within a few days.

Where's the Chart, NOW?

Yes, Difucci is one of the best in the business. So is Derrick Wood of TD Cowen, though, and he still has NOW at a "Buy" with a target price of $870. Is the stock expensive? Yes, indeed it does seem so. At 60-times forward looking earnings, 17 times sales and 20 times book, NOW would appear expensive. Then again, that price/earnings to growth ratio of 2.72 is impressive. Less than 1.5% of the float is currently held in short positions. While that removes a potential group of buyers, ultimately, almost 91% of that float is held by institutions in long positions. That's impressive.

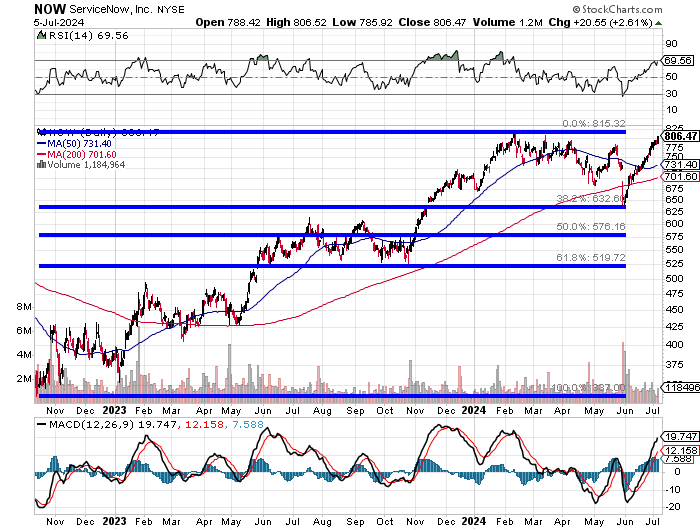

Readers will see that NOW rallied from October 2022 into early 2024. At that point, the stock went into a basing period of consolidation where resistance has been found in the same area several times and support at the 38.2% Fibonacci retracement level of that almost year-and-a-half-long rally. Let's zoom in...

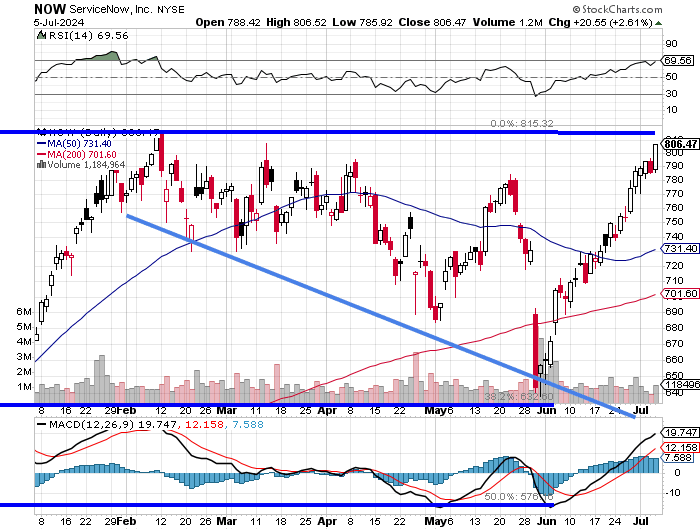

Readers will now see that within that base is what we call a "right-angled descending broadening wedge." This is recognized as a pattern of bullish reversal. Basically, this is an inverted ascending triangle. Both the flat line and descending trendline must be touched more than once. We have that here. Does this pattern ever fail? All patterns fail. This one though is thought to break-out to the upside far more often than to the downside.

In short, yes, I do intend to add at least a portion of what I had already sold now that the last sale will likely 4% hit or so. Just a bit, though. I am going to leave room for error, and room to add on momentum upon such an upside breakout.

ServiceNow Strategy

Target Price: $895

Pivot: $815

Add 1: $780 area or below on this weakness.

Add 2: At or just above pivot upon a breakout.

Panic: Break of 50-day SMA (currently $702).

At the time of publication, Guilfoyle was long NOW, CRWD, MSFT, PLTR equity.