There's Reason to Believe in Wells Fargo Despite Selloff

The big bank saw a stock selloff in response to its latest earnings report, but I won't abandon my thesis.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Friday morning, the large banks started reporting their second quarter earnings. Long-time Sarge name Wells Fargo WFC was among those batting leadoff. The quarter looked okay. The stock sold off hard in response. Let's take a look.

For the three-month period ended June 30, 2024, Wells Fargo posted GAAP EPS of $1.33 on revenue of $20.689 billion. The top-line print showed year-over-year growth of 0.8%, beating expectations, while the bottom-line print also beat Wall Street, while comparing well to $1.25 for the year ago comparison.

Net interest income decreased 9% to $11.923 billion, which I think the market is taking rather hard. The bank blamed the decrease on "the impact of higher interest rates on funding costs, including the impact of lower deposit balances and customer migration to higher yielding deposit products in Consumer Banking, and Lending and Wealth and Investment Management."

Non-interest income was much stronger, up 19% to $8.766 billion "driven primarily by higher trading revenue in our Markets business, higher investment banking fees, an increase in asset-based fees in Wealth and Investment Management on higher market valuations, the impact from the adoption of a new accounting standard for renewable energy tax credit investments, and improved results from our venture capital investments."

In addition to those numbers, non-interest expense increased 2% to $13.293 billion, while provisions for credit losses printed at $1.236 billion, down 27.8% from the June 2023 quarter, but including a higher allowance for credit card loans. The firm did repurchase $6.1 billion worth of common stock during the second quarter bringing total repurchases for the first half up to $12 billion.

Ratios

The firm's common Equity Tier 1 ratio (CET1) improved from 10.7% to 11% as deposits contracted slightly and loans contracted close to 3.1%. The firm's return on equity (ROE) improved from 11.4% to 11.5%, while the firm's return on tangible common equity (ROTCE) stayed where it was a year ago at 13.7. While these ratios are fine, for comparison's sake, JP Morgan JPM reported a CET1 of 15.3%, an ROE of 23% and an ROTCE of 28% for the same quarter, so there is definitely room for improvement.

CEO Charlie Scharf Outlines Investments

CEO Charlie Scharf commented in the press release... “We continued to see growth in our fee-based revenue offsetting an expected decline in net interest income. The investments we have been making allowed us to take advantage of the market activity in the quarter with strong performance in investment advisory, trading, and investment banking fees. Credit performance was consistent with our expectations, commercial loan demand remained tepid, we saw growth in deposit balances in all of our businesses, and the pace of customers reallocating cash into higher yielding alternatives slowed.”

Scharf then added... "We are investing in our branch network to improve the customer experience including refurbishing branches and enhancing technology. In our commercial businesses we are investing in talent and technology to capture the opportunity inherent in our franchise including hiring a new Co-CEO of Corporate and Investment Banking.”

Segment Performance

- Consumer Banking & Lending generated revenue of $9.006 billion (-5%), producing net income of $1.777 billion (-7%), as provisions for credit losses increased 7% to $932 million. Average loan balances were down 3%, while average deposits were down 5%.

- Commercial Banking generated revenue of $3.122 billion (-7%), producing net income of $1.182 billion (-8%), as provisions for credit losses increased 12% to $29 million. Average loan balances were down 1%, while average deposits were flat.

- Corporate & Investment Banking generated revenue of $4.838 billion (+4%), producing net income of $1.785 billion (+48%), as provisions for credit losses decreased 69% to $285 million. Markets generated revenue growth of 16% as the investment bank drove revenue growth of 38%. This was offset by a 4% contraction in revenue generated by commercial real estate and a 10% contraction in the management of treasuries and associated payments. Average loan balances were down 5%, while average deposits were up 17%.

- Wealth & Investment Management generated revenue of $3.858 billion (+6%), producing net income of $484 (-1%), as provisions for credit losses dropped to $-14 million from $24 million. Average loan balances were flat, while average deposits were down 8%.

- Corporate generated revenue of $248 million (up from $30 million), producing net income/loss of $-318 million (down from $46 million), as provisions for credit losses increased to $4 million from $-144 million.

Guidance

For the full year 2024, the firm still expects net interest income to be down 7% to 9% from 2023. However, the firm currently expects the final result to be in the upper half of this range at 8% to 9%. At least some on Wall Street were looking for an improvement upon this guidance and that is hurting the stock price this morning.

Additionally, noninterest expense for the full year is now expected to end up around $54 billion, which is up from prior guidance of roughly $52.6 billion due to higher-than-expected compensation expense and an FDIC special assessment expense of $336 million.

My Thoughts

The second quarter was not a bad quarter. I think the tough guidance has more to do with Friday morning's selloff. Does this shale my thesis in the stock? No. Does this shake my confidence in Scharf? No. It does, though, put me on notice that the firm is quite capable of underperforming my expectations, even if just in the provision of guidance.

The thesis for my investment is two-pronged: One, Scharf's push to take Wells Fargo from a meat-and-potatoes, net-interest-margin-producing bank to more of an investment bank driven by fees as well. That transition seems to be underway and "so far, so good."

The second prong of my thesis is the $1.95 trillion asset cap placed on the firm in the wake of its past misdeeds under different management. The bank still has eight open consent orders in need of being corrected before the Federal Reserve might lift that cap. My feeling is that, once it looks like Wells Fargo is well on its way to reaching that goal, that this will be reflected in an appreciation in the share price. This is really why Scharf was brought in from the Bank of New York Mellon BK — to clean the place up.

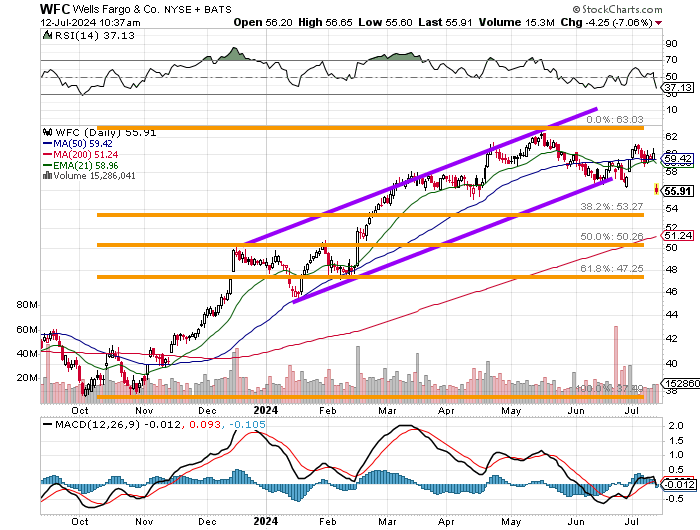

Readers will see that WFC had resided in an ascending price channel from the start of the year into June, when support cracked. Relative Ssrength is now relatively weak. The daily MACD is now bearishly postured. The stock is down about 7% for the day so far, after gapping lower overnight. My plan, as I am still up 24% on this position, but it is not a top-ten position for me, is to add carefully. This name is still, in my opinion, invisible and Scharf is still "the guy." Though it will increase my net basis, I expect to add between the current last sale and the stock's 200-day SMA. Should that line fail, there is more potential help at the "half-way back" point of the October into June rally just about $1 below that 200-day line.

At the time of publication, Guilfoyle was long WFC equity.