The ‘Others’ Just Can’t Catch a Bid

It’s still an either/or market with money flowing into the tech leaders, but not the others.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

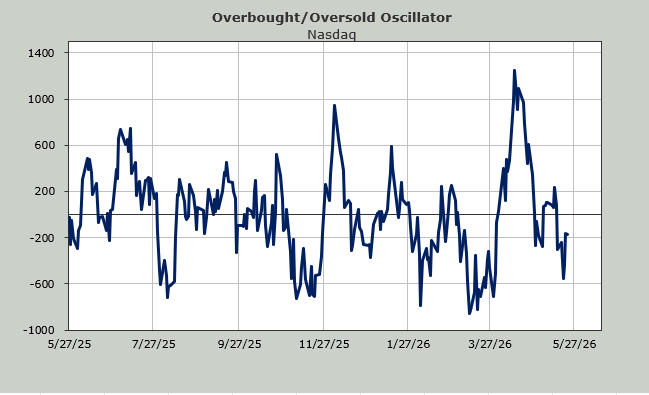

I would have thought the rally late last week that favored the others over NVIDIA would have changed the breadth indicators, but that was not the case. For example, the McClellan Summation Index is still heading down.

It is possible, even likely, that the others continue their rally on the news of a peace deal and the Summation Index turns up this week, but it goes to show you how much selling had taken place in those names over the last four weeks (since mid-April).

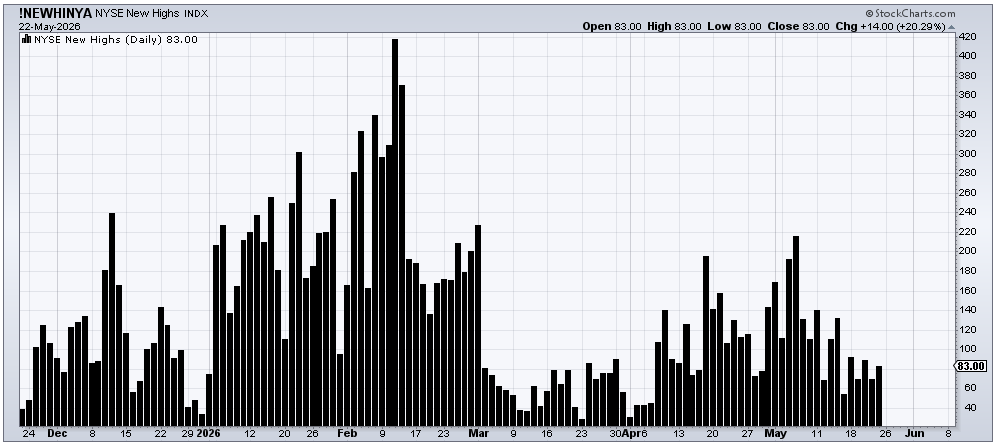

The rally also hasn’t helped the number of stocks making new highs, as that reading remains lackluster. Again, perhaps the news will help the situation, but it hasn’t done so yet.

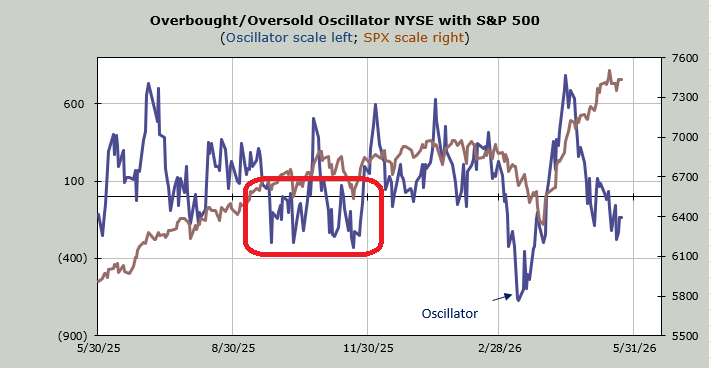

I suspect that with the Oscillator short-term oversold (notice the Oscillator hasn’t pushed upward despite three days of rallying), we’re still apt to see more of the action that we saw last fall (red box) than much else.

So that’s what did not change. Let’s focus on what has changed. Bonds rallied (even though the Daily Sentiment Index—DSI—did not get under 20), which in turn helped the hysteria from Monday die down. And the Utes rallied! In fact, the Utes were up four percent last week, bouncing right off that crummy line I drew. I think there will be some resistance as it approaches that downtrend line and all that resistance overhead, but for the time being, I remain a fan of the Utes.

The Homebuilders, using the ITB ETF, appear to have had a false breakdown as it plunged to a lower low with no follow-through and a recapture of the 88 support/resistance level.

The rally in bonds, however, has not helped the industrials or the materials. In fact, most other groups continue to do a lot of sloshing around.

Sentiment-wise, the put/call ratios continue to show folks are giddy. The Market Vane bulls (discussed in full a week ago) show folks are giddy. The Citi Panic/Euphoria Model (shown last week) is also showing Euphoria, or giddy.

The AAII folks are not bullish. The Investors’ Intelligence bulls are at 48% bulls, so they too are not extreme. The NAAIM folks have pulled back their exposure to the low 80s. And then there is the DSI.

The DSI for the VIX fell to become a teenager on Friday. Keep this in mind because last week we had consecutive days with the put/call ratio for the VIX under .20, a sign the pros are buying VIX calls more than VIX puts. We typically want to be on the side of the pros.

Typically, when the DSI for the VIX gets too low, the DSI for the market indexes (S&P and Nasdaq) is high. This time, they are currently both at 76. I have my (one good!) eye focused here because if the market rallies on news of peace, these readings of 76 could shoot to giddy in a heartbeat (85+ is giddy).

For now, I still think the market is quite complacent. Let’s see if it can cross over to giddy.