The Dilapidated Housing Market Appears to Be Building a Foundation

Explosive breakouts in mortgage lenders could signal an end to housing malaise, so here's how I'd unlock opportunities in the sector.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The National Association of Realtors released on Thursday some gloomy sales figures.

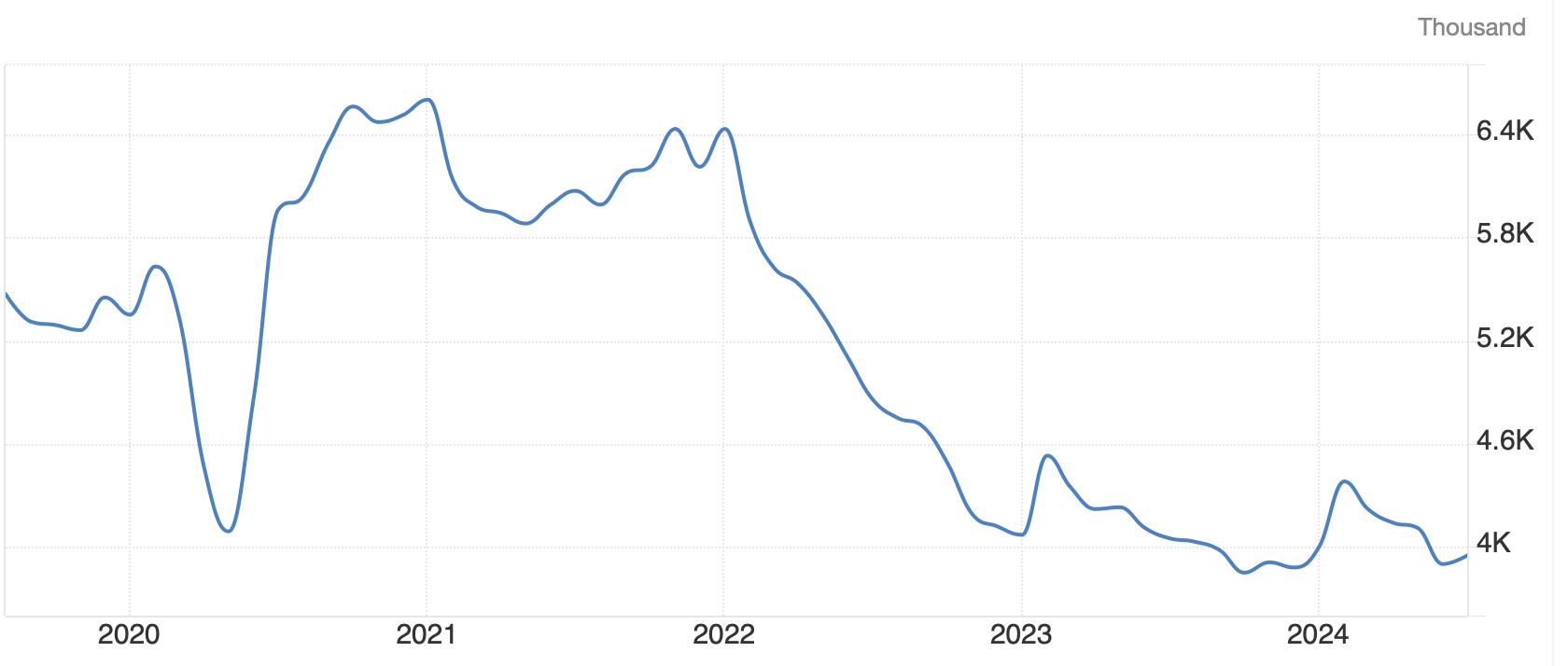

As has been the case for some time, the results were bleak. Existing homes, which make up about 85% of overall U.S. home sales, came in at an annualized rate of just 3.95 million. That figure represents a 40% decline from January 2021, when sales were pushed forward by the Covid-19 pandemic.

Real estate agents are quitting in droves. A recent article from the Washington Post indicated that up to 80% of real estate agents could leave the profession, due to slow sales and changes in commission structure.

That’s the bad news. The good news is that existing home sales may have bottomed.

As the following five-year chart demonstrates, existing home sales are no longer trending lower. Instead, sales are moving in a sideways range. This is a major improvement over the sharp downtrend that started in early 2022.

The real estate industry may be looking grim, but it’s always darkest before dawn. Real estate activity should get a boost from lower interest rates.

According to Mortgage News Daily, a 30-year fixed-rate mortgage currently has an average rate of 6.48%. In April, that rate was as high as 7.43%.

'Furthermore, the CME’s FedWatch tool now shows a 75.5% chance of a quarter-percentage point Fed rate cut on Sept. 18, and a 24.5% chance of a half-point cut.

By year end, odds favor a total cut of one-percentage point -- a full 1% -- in the Fed funds rate.

Expectations for an increase in housing sales and refinancing are already being reflected in stocks related to the real estate industry.

Shares of several mortgage lenders are ripping. UWM Holdings (UWMC), which led the U.S. with nearly 295,000 mortgages originated last year, has seen its shares jump by over 21% in the past month.

Shares of Rocket Mortgage RKT, which originated 288,000 loans in 2023, have seen a 32.4% increase over the past month.

What’s the play? Generally, I don’t like to chase stocks. Both UWM and Rocket seem overextended, but I’d consider buying either on a pullback -- especially if that pullback is due to general market softness, as opposed to industry-wide or company-specific news.

What are the right prices to pay for UWM Corp and Rocket Holdings? I'm using Fibonacci measurements to gauge entry points in the event of a pullback.

For example, a 38.2% pullback in UWMC would take the stock to about $9:

A similar pullback in Rocket Mortgage would lower that stock’s price to $18:

The caveat here is that any pullback that does occur must be due to overall market conditions. I won’t buy either name if it falls due to company-specific, or even industry-specific news. That condition is too important to ignore.

If these stocks fail to pull back to the levels I’ve indicated, that would be fine. Nobody catches every trade, and I’m not willing to sacrifice discipline or process due to fear of missing out.

At the time of publication, Ponsi had no position in any security mentioned.