Stand and Salute Nvidia, Then Trade It This Way

Another blowout quarter. Strong guidance. Again. An increased dividend. A ten for one stock split.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Mightiest of Them All...

All hail, for the greatest company of the modern era, the beast of modern day tech, the driver for the economy for the next many years has reported. Stand and salute.

I Was Made For lovin' You

I was made for lovin' you, baby

You were made for lovin' me

And I can't get enough of you, baby

Can you get enough of me?

- Stanley, Child, Poncia - KISS, 1979

The Setting

Markets had tread on eggshells all day, trying not to get hurt ahead of the release. The FOMC Minutes read as hawkish. That upset markets a little, but the focus on what would happen after the closing bell remained as was. Oh, the news would be good for the long Nvidia NVDA crowd, and for those long stocks that might be carried along in the "pin action."

For the firms' first quarter of fiscal 2025 that ended on April 28th, Nvidia posted an adjusted EPS of $6.12 (GAAP: $5.98) on revenue of $26.044B. The adjusted and GAAP EPS prints both crushed consensus views. This, as the print for revenue generation beat expectations by close to $1.5B, while reflecting year over year growth of 262.2%. The adjustments made were made primarily for stock-based compensation expense and acquisition related costs.

The firm also announced a ten for one stock split in order to make equity investment in the firm more accessible to employees and retail investors. Those shareholders of record at the close on Thursday, June 6th, will receive nine additional shares for each one share held after the close on Friday, June 6th.

Additionally, Nvidia announced a 150% increase to the quarterly cash dividend from $0.04 per share now to $0.01 per share, post-split (or $0.10 per current share). The yield is so tiny that this is hardly worth mentioning, but it is something. Did I mention that the firm provided strong guidance as well. Quite the evening. I can't get enough of you, baby

Can you get enough of me?

Operations

While revenue generation grew 262.2% to $26.044B, the cost of that revenue increased 121.6% to $5.638B, leaving a GAAP gross profit of $20.406B (+339%). This took GAAP gross margin to 78.4% from 64.6%. for the year ago comp. On an adjusted basis, gross profit printed at $20.56B on a gross margin of 78.9%, up from 66.8%.

GAAP operating expenses increased 39.4% to $3.497B, leaving operating income of $16.909B (+690%, not a misprint) on an operating margin of 64.9%, up from the year ago comp of 29.8%. Again, these are not misprints. On an adjusted basis, operating income printed at $18.059B on an operating margin of 69.3%, up from 42.4%.

After accounting for interest, taxes, and other income/losses, GAAP net income hit the tape at $14.881B (+628.4%), while adjusted net income landed at $15.238B (+461.7%). This works out to EPS of $5.98 (GAAP) and $6.12 (adjusted).

Revenue Generation by Business Platform

- Data Center... generated sales of $22.563B, up 427% year over year, crushing expectations.

- Compute generated sales of $19.392B, up 478% year over year.

- Networking generated sales of $3.171B, up 242% year over year.

- Gaming generated sales of $2.647B, up 18% year over year, a slight beat.

- Professional Viz generated sales of $427M, up 45% year over year, but was a miss.

- Automotive generated sales of $329M, up 11% year over year., which was a beat.

- OEM & Other generated sales of $78M, up 1% year over year, a slight miss.

Guidance

For the current quarter, Nvidia guided revenue towards $28B, plus or minus 2%. Wall Street came in at about $26.5B for this number. Gross margin is expected to land at 74.8% (GAAP) or 75.5% (adjusted) give or take 50 basis points. The firm still sees full year gross margins in the mid-70's in percentage terms. Full year operating expenses are expected to grow in the low-40's in percentage terms, while the firm's effective tax rate is seen at 17%, plus or minus 1%.

On Demand

In answering questions at last night's earnings call, CEO Jensen Huang said, "We see increasing demand of Hopper through this quarter. And we expect to be -- we expect demand to outstrip supply for some time as we now transition to H200, as we transition to Blackwell. Everybody is anxious to get their infrastructure online. And the reason for that is because they're saving money and making money, and they would like to do that as soon as possible."

On China

During the call, CFO Colette Kress said, "We ramped new products designed specifically for China that don't require an export control license. Our Data Center revenue in China is down significantly from the level prior to the imposition of the new export control restrictions in October. We expect the market in China to remain very competitive going forward."

In answering a question much later in the call, CEO Jensen Huang said, "It is the case that our business in China is substantially lower than the levels of the past. And it's a lot more competitive in China now because of the limitations on our technology."

Huang added, "We continue to do our best to serve the customers in the markets there and to the best of our ability, we'll do our best. But I think overall, the comments that we made about demand outstripping supply is for the entire market and particularly so for H200 and Blackwell towards the end of the year."

Fundamentals

For the period reported, Nvidia generated operating cash flow of $15.345B, which was up 33.5% sequentially and up 427.1% from the year ago comparison. Out of that came capex spending of $369M and principal payments on property and equipment of $40M, leaving free cash flow of $14.936B. The FCF print was up 33.2% q/q and up 465.1% y/y.

Glancing at the balance sheet, the firm's cash position stands at $31.438B (+9.4% in just three months) and inventories stand at $5.864B. This puts current assets at $53.729B. Current liabilities add up to $15.223, including $1.25B in short-term debt. This works out to current and quick ratios of 3.53 and 3.14, which is just absurdly strong for any firm, but especially for a firm this size.

Total assets amount to $77.072B, including goodwill and intangibles of $5.439B. At 7% of total assets, this is of no concern to fundamental analysts. Total liabilities less equity comes to $27.93B, including another $8.46B in long-term debt. For those about to ask, the firm could pay off its entire debt-load out of cash and get more than $2B back in change. This is one heck of a balance sheet.

Fun Facts

In terms of market cap versus GDP, Nvidia would be the eight largest nation in the world. Nvidia is now also larger than Amazon AMZN and Walmart WMT combined. Looked at another way, Nvidia is now larger than 20 Boeing's BA.

Wall Street

This was a little bit of work. After weeding out all of the sub-four star sell side analysts with opinions on NVDA, I have found 31 highly rated (4+ stars at TipRanks) sell-side analyst who reacted to last night's release. After allowing for changes, among our 31, we have 29 "buy" or buy-equivalent ratings and two "hold" or hold equivalent ratings. Two of our "buys" chose not to set target prices, so that leaves 29 of those to work with.

The average target price across the 29 analysts was $1,199.66 with a high of $1,400 (CJ Muse of Cantor Fitzgerald) and a low of $900 (Gil Luria of DA Davidson). Once removing those two as potential outliers, the average target across the other 27 rises to $1,203.33. The average "buy" target came to $1,218.15.

My Thoughts

What's not to like? I wish I never sold any. I am still long the name, but when I think about it, every time NVDA hit one of my target prices and I sold some shares, though I profited nicely and one should never question that, I probably should never have sold any.

That is crazy. It's almost enough to cause one to cast a long successful code of discipline aside. Don't even be tempted to go there. While allowing discipline to relax in a name like this would work out, that is unique. A loss of discipline, I am certain would cost me more somewhere else at some other time.

Another blowout quarter by Nvidia. Strong guidance. Again. An increased dividend. A ten for one stock split. No lack of demand even out on the horizon. Last night, Huang referred to his customers, otherwise known as "big tech" to be early in their buildouts. They'll be waiting on the coming Blackwell platform while still buying the H100 and H200 in bulk if they can.

The margins are outstanding, cash flows are simply amazing, and the quality of the balance sheet is simply next level. Will there be competition? Yes. Even if that competition is seen as one step behind? Yes.

I told you last week that I had started to rebuild my long position in Advanced Micro Devices AMD. Yes, I think AMD is a winner here, even if only on Nvidia's coattails. You can like Coke KO and Pepsi PEP.

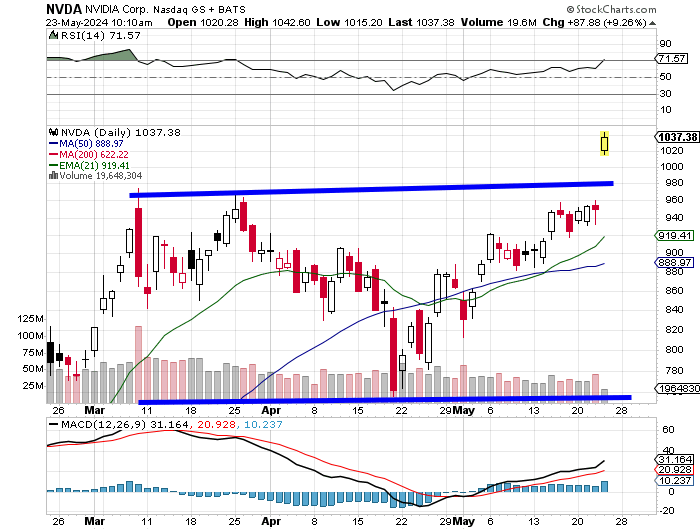

In yesterday's column we spoke about the basing period of consolidation that NVDA had been stuck in since early March. We gave you a $94 pivot that has now been triggered. Yes, there is a new gap that would need a $960 tick to fill. Probably not soon, but one never knows.

Today is the day of Nvidia's latest breakout. Relative strength is even stronger now, and has run up against potentially short-term overbought territory, while the daily MACD (moving average convergence divergence) is reflecting it most bullish look since early 2024.

Nvidia

- Target Price: $1125

- Pivot Pint: $974

- Add: From 21-day EMA (exponential moving average) down to 50-day SMA (simple moving average) (currently $919 down to $888)

- Panic: Break of April low ($756)

At the time of publication, Stephen Guilfoyle was long NFLX, AMZN, AMD equity.