Unlikely Small-Cap Stock With Breakout Potential Has Emerged

A surprising small-cap name rallied with aggression amid a broad sell off last week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Yes, I know: the rotation out of mega-cap tech and into small caps. That was the weekly overview. That said, small caps sold off just like everyone else late last week. This name, however, rallied and rallied with aggression (+9%) on Friday.

I am speaking today about a shoe company. Shoes, Sarge? Really? Hear me out, gang. You know I've had a knack for finding diamonds in the rough. Not that this shoe company is going to be a "diamond," but it might just make us a few clams. We'll see.

The small-cap name is Wolverine (not the superhero) World Wide WWW. The firm designs, markets and licenses a variety of casual footwear, apparel, kids' footwear, performance outdoor, footwear, work boots and uniform shoes. Business segments include the Active Group and Work Group. The Active Group includes such brands as Merrell, Saucony (running shoes), Sweaty Betty and Chaco. The Work Group includes such brands as Wolverine, Cat Footwear, Bates, Harley-Davidson footwear and HYTEST. Other businesses outside of the two main segments would be Sperry, Keds and Hush Puppies.

The firm's businesses stretch across 170 different countries and territories through operations in the U.S., Canada the U.K. and smaller hubs in Europe and Asia. Wolverine World Wide is headquartered out of Rockford, Michigan.

The Latest News

Wolverine caught a nice upgrade from UBS analyst Mauricio Serna, who is rated at three stars (out of five) by TipRanks. Serna took WWW up to a "buy" rating from "neutral" while increasing his target price from $13 to $20. This comes less than a month after the stock had been upgraded to a "buy" by two five-star analysts.... Mitch Kummetz of Seaport Global and Sam Poser of Williams Trading. Those two, respectively, have targets of $16 and $20 on the stock.

Serna obviously sees some growth potential in Wolverine, as he along with colleague Jay Sole wrote: "We think the combination of (mid-single digit percentage) sales growth, ongoing operating margin recapture and incremental (free cash flow) deployment towards debt repayment and share repurchases should drive 14% 4-year EPS CAGR post GY 24."

Earnings and Fundamentals

Wolverine is expected to report the firm's second quarter financial results on August 7, 2024. Wall Street is looking for an adjusted EPS of $0.12, down from $0.19 for the year ago comp, but up from Q1 adjusted EPS of $0.05. The GAAP EPS is also expected to improve sequentially from $-0.19 to $0.08. Sales are seen at $411 million, which would be a significant year-over-year contraction (-29%), but also a sequential improvement (+4%).

Free cash flow has been a consistent positive on an annual basis, despite quarter-by-quarter volatility. The firm's current ratio is greater than one, but short-term debt (debt maturing in less than a year) outweighs the firm's cash balance, meaning that the firm will likely have to refinance at what will likely be higher interest rates. The firm understands that this is not optimal and is working toward reducing the overall debt-load. The firm is also managing a fairly large long-term debt-load so this will be a multi-year work in progress.

The firm does return some cash to shareholders, paying an annual dividend of $0.40 per year (in fact, the stock goes ex-dividend today) for a yield of 2.89%. The stock does, at times, repurchase shares for the treasury but has not done so in decent size since 2023. The stock trades at a below average 17-times forward-looking earnings, while roughly 13% of the float is currently held in short positions.

Technicals

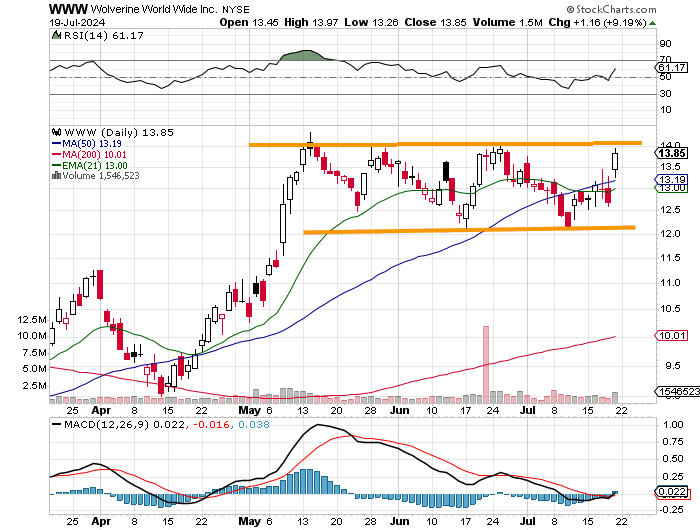

Readers will see that the shares of WWW are approaching the resistance level of a basing period of consolidation that they have been trapped in since early May. The stock has been stopped at $14 three times in a row after stopping at $14.45 in May, so we'll go with a 414 pivot. Relative strength is improving, as is the daily MACD. Both the histogram of the nine-day EMA and the 12-day EMA are now in positive territory, while the 26-day EMA (as might be expected), lags behind.

A take and hold of the $14 pivot would cement the stock's standing above all of its key moving averages and open the door to a potential target price of $17.50. Sounds like chump change? Where I come from, 25% is never considered chump change. The stock can probably be added to or initiated down to its 50-day SMA.

At the time of publication, Guilfoyle had no positions in any securities mentioned.