Palo Alto Flashed Buy-the-Dip Opportunity After Golden Crossover

Is it time to buy the cybersecurity name after a “standout quarter”?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday evening, cybersecurity platform provider Palo Alto Networks (PANW) released the firm’s fiscal third quarter financial results.

The Sarge-folio currently has no position in PANW, but is still long CrowdStrike (CRWD) holdings, which is a key competitor. Therefore, it is with a keen interest that we go through these numbers.

For the three-month period ended April 30, Palo Alto posted an adjusted EPS of $0.85 (GAAP EPS: -0.22) on revenue of $3.002 billion. These top- and adjusted bottom-line results both beat expectations while the sales print was good for annual growth of 31%. Adjustments were made primarily for the purposes of share-based compensation and the amortization of acquired intangible assets.

Chairman and CEO Nikesh Arora commented in the press release:

“Q3 was a standout quarter for Palo Alto Networks, with accelerating organic bookings growth as customers turn to us to secure their AI deployments at scale. The latest advancements at the AI frontier have increased the level of urgency around cybersecurity and redefined the shape of the industry for the coming years.”

CFO Dipak Golechha added:

“We are executing ahead of our M&A integration plans and improving profitability across our businesses, which keeps us firmly on track to achieve 40% adjusted free cash flow margin in FY28.”

Need to Know

- Next-Generation Security ARR for the fiscal third quarter 2026 grew 60% year over year to $8.1 billion. This includes $1.6 billion in NGS ARR from CyberArk and Chronosphere.

- Remaining performance obligation grew 36% year over year to $18.4 billion. This includes $1.8 billion from CyberArk and Chronosphere.

Operations

While revenue generation popped 31% to $3.002 billion, the cost of that revenue increased 57.4% to $974 million. This left a gross profit of $2.028 billion (+21.4%) as gross margin dropped from 73% to 67.6%. On an adjusted basis, the cost of sales increased 32% to $726 million, leaving a gross profit of $2.276 billion (+31%). This took the firm’s adjusted gross margin up to 78.8% from 78.4%.

GAAP operating expenses grew 52.4% to $2.211 billion, leaving a GAAP operating income/loss of -$156 million, down from $311 million. After accounting for interest, other income and expenses as well as taxes, GAAP net income/loss printed at -$177 million, down from $262 million. This works out to a GAAP EPS of -$0.22, which compares poorly to the year-ago comp of $0.39.

On an adjusted basis, operating income increased 30% to $814 million as operating margin dropped from 27.4% to 27.1%. This left an adjusted net income of $684 million (+21.9%). That works out to an adjusted EPS of $0.85, up from the year-ago comp of $0.80. You kids already know how I feel about adjusting for share-based compensation for mature firms that do it every single quarter. If you do it every quarter, it’s an ordinary operating expense, so stop pretending. You lost money this quarter, sport. Doesn’t make the stock a poor investment. Just stop pretending.

Guidance

For the current quarter, Palo Alto sees revenue of $3.35 billion to $3.36 billion and adjusted EPS of $0.96 to $0.98. Wall Street was looking for something like $3.28 billion and $0.94 so this guidance is a beat. Remaining performance obligation is seen at $20.9 billion to $21 billion. This also beat expectations.

For the full fiscal year, total revenue is projected at $11.42 billion to $11.43 billion, while adjusted EPS is projected at $3.77 to $3.79. Wall Street was looking for $3.69 on $11.29 billion or so. This guidance also beats Wall Street. RPO is obviously the same as the above guidance is for a fiscal fourth quarter.

Fundamentals

For the period reported, Palo Alto generated operating cash flow of $871 million. Out of that number came capex spending of $83 million. This left free cash flow of $788 million (+40.7%). The firm does not pay out a cash dividend to shareholders.

Turning to the balance sheet, Palo Alto ended the quarter with a cash position of $3.111 billion and current assets of $7.713 billion. Current liabilities add up to $9.006 billion. Out of that number, the only current debt is $160 million in convertible notes. Deferred revenue accounts for $7.113 of that total, which we do not count against our version of any company’s current ratio. That puts the firm’s “adjusted” current ratio at a muscular looking 4.07.

Total assets amount to $46.266 billion. Of that total, $29.185 billion or 63.1% is labeled as either goodwill or other intangibles. That is a bit ridiculous in my humble opinion. Total liabilities less equity comes to $18.598 billion. This includes another $1.192 billion in convertible notes, but also another $6.492 billion in deferred revenue. This is a very strong balance sheet, even if one omits a sizable portion of those “intangibles” listed under total assets. No need for the sugar coating.

Opinion

These earnings aren’t bad. I make fun of the “window dressing” where applicable, but this was not a bad quarter. Cash flows are positive and improving. The guidance is strong. The balance sheet is strong. This stock is certainly investible. Just maybe not right this minute.

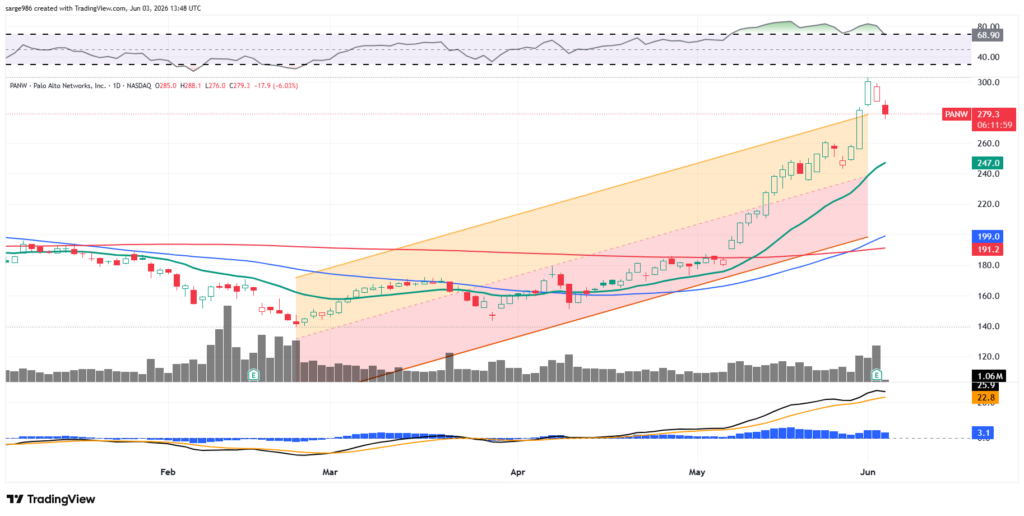

Readers will see that PANW went a bit parabolic over the two months leading into these earnings. Late last week, the stock broke above trend and has come back a bit this week. RSI is a bit extended, though that does not mean what it used to. The daily MACD is postured rather bullishly. The stock also just enjoyed a golden crossover of the 200-day SMA by the 50-day SMA.

One would think this may be a “buy the dip” opportunity, and it may be. I am definitely looking for a chance to add to my CRWD long on this “pin action” as that stock went equally parabolic. As far as PANW is concerned, I need to see if this is a head-and-shoulders pattern in the making (which would be bearish) before I commit capital.

Going out six weeks and writing a $250 put that expires on July 17 for about $7 makes more sense to me right now than laying out $282 per share for 100 shares of equity.

At the time of publication, Guilfoyle was long CRWD equity.