Here's a Small-Cap Name With Short Potential

Bearish strategies have emerged for a small-cap stock that distributes some well-known brands.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Three years ago, the stock of Newell Brands NWL traded at $30 a share. Last night, the stock closed at $6.84. That's a 77% beatdown over 36 months. Not pretty. They do say that every dog has its day. Friday might just be that day for Newell Brands.

But just who is Newell Brands?

You know the names well and probably make use of many of them on a fairly regular basis: Graco, Coleman, Oster, Rubbermaid, Yankee Candle, Sharpie, Paper Mate, Elmer's, Mr. Coffee, Sunbeam. The list goes on. I use Sharpie highlighters and Paper Mate pens every day at work. I have a Coleman lantern next to my bed in case we lose power. My wife has a bunch of Yankee Candle products scattered around the house for the same purpose.

On Friday morning, Newell Brands posted a Q2 adjusted EPS of $0.36 (GAAP EPS: $0.11) on revenue of $2.033 billion. That adjusted bottom-line number beat Wall Street by a wide margin. However, the top-line print reflected a year-over-year contraction of 7.8% while falling short of consensus view. The adjustments made were made primarily for acquisition amortization purposes.

Expanding Margin

The firm has been able to optimize costs and mitigate a tough environment for demand globally. Second quarter adjusted gross margin improved 490 basis points to 34.8%, as adjusted operating margin improved 170 basis points to 10.8%.

CFO Mark Erceg commented on the matter in the press release using GAAP data: "Second quarter reported gross margin increased by 590 basis points versus last year, which builds on the 110, 360 and 380 basis point expansions that occurred during the three sequential quarters that preceded it, respectively. The rapid and dramatic improvement we have delivered in gross margin ties directly back to the development and implementation of our new strategy and has allowed us to invest more in advertising and critical front-end commercial capabilities, while also expanding reported operating margins."

Guidance

For the current quarter, Newell (my hands keep trying to type "Rubbermaid") is projecting a net sales decline of 6% to 4% and a core sales decline of 2% to flat. The firm sees adjusted operating margin of 8.3% to 8.8% and adjusted EPS of $0.14 to $0.17. That's a little below the $0.18 to $0.20 that Wall Street was looking for.

However, the full year guidance was improved upon and has helped push the stock higher this morning. For the full year, the firm now sees a sales decline of 7% to 6%, narrowing the prior guidance of a decline of 8% to 5%. Core sales are expected to decline 4% to 3%, up from prior guidance of a decline of 6% to 3%. The firm expects to realize a full year adjusted operating margin of 8% to 8,2%, up from prior guidance of 7.8% to 8.2%, and has taken its projected adjusted EPS from $0.52 to $0.62 up to $0.60 to $0.65.

Fundamentals

For the first half of the year, Newell has generated just $64 million in operating cash flow, while capex spending has come to $112 million. That's a free cash flow of $-48 million, as opposed to the first six months of 2023 when the firm drove free cash flow of $135 million. That said, the firm had positive net income over the first six months this year, while they did not last year. The firm cut cash dividends paid to shareholders more than in half year over year to $60 million.

Turning to the balance sheet, the firm's cash position stands at $382 million, while inventories are up to $1.639 billion. That puts current assets at $3.425 billion. Current liabilities add up to $3.502 billion, including short-term debt of $983 million (+199% over six months). This leaves the firm with a current ratio of 0.98 and a quick ratio of 0.51.

Total assets are running at $12.048 billion, including goodwill and other intangibles of $5.467 billion. At 45% of total assets, that's probably about as high as I'd want to see that number. Actually, I'd like to see it lower. Total liabilities less equity comes to $8.968 billion, including longer-term debt of $4.059 billion.

This balance sheet obviously has its problems. The cash to short-term debt is an issue, especially in a negative free cash flow environment. This means that the firm will be forced to refinance some debt, probably not at friendly rates. The current ratio below 1.0 is sub-optimal to say the least. I probably am less okay with that than I am the quick ratio of more than 0.5. I mean, I think we know that the inventories will hold at least some, maybe most of their value.

Latest Moves

Four-star rated (by TipRanks) analyst Lauren Lieberman of Barclays assigned (initiated) a "hold" rating on NWL with an $8 target price. Earlier this week, Nik Modi (five-star rated) of RBC Capital reiterated his "hold" rating and $7.50 target price on the name, while Andrea Faria Teixeira (three-star rated) of JP Morgan also reiterated a "hold" but took her target down to $7 from $8.

My Thoughts

Margins are improving. The full year guidance was a nice surprise. The fundamentals kind of stink, to be bluntly honest. The analysts did not see a good reason for the pop that the market has granted the stock today.

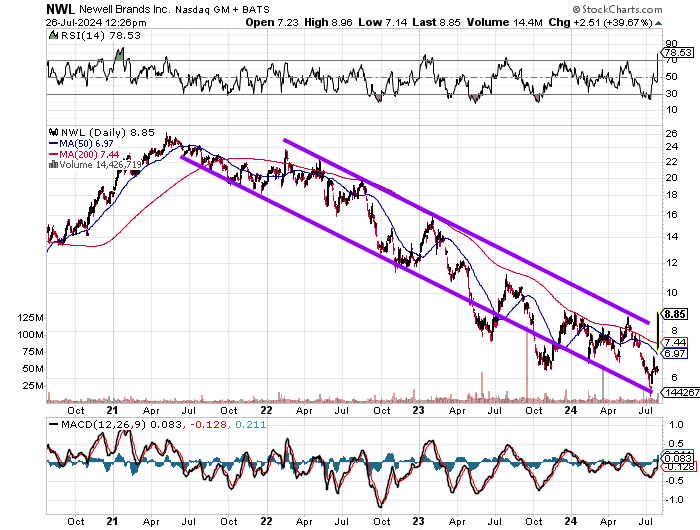

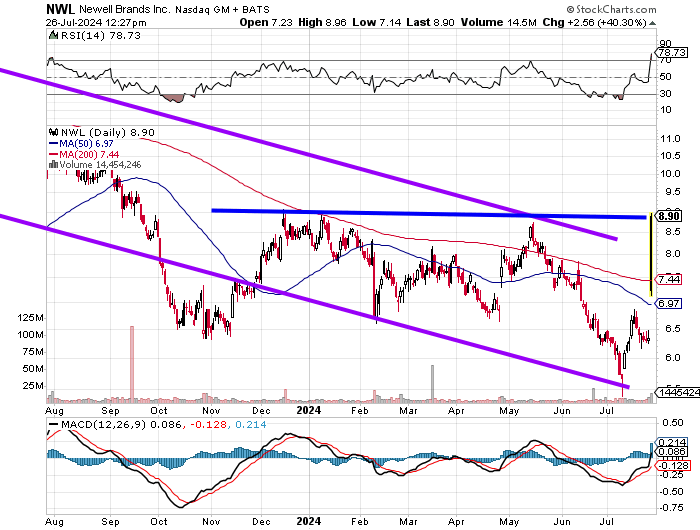

Not the best four-year chart in the world, is it? Let's zoom in.

Relative strength is suddenly in technically-overbought territory. The daily MACD is suddenly in better shape, but can you trust it? The stock gapped right over its 50-day and 200-day SMAs this morning. The chart monkeys were forced to increase exposure, exacerbating the pop. The stock is now trading close to the $9 level where it has been rejected three times since December. Is there a large institutional seller (or two) with a $9 portfolio limit on the order? Certainly, could be. Might even say it's probable.

I think I like this name as a short. The problem is that 9.8% of the entire float is currently held in short positions. I always teach that once 8% to 10% of any stock is held short, then we must be wary of the potential for a squeeze. More than 10%, we don't even think about it. That said, I have some ideas.

An Interested Bear Could (in Minimal Lots)...

- Sell short 100 shares of NWL at $8.90.

- Purchase one August 16th $9 call for $0.40.

Or

- Purchase one August 16, 2024 $9 put for $0.50, and let it ride.

Notes: Plan one leaves the trader with a short position that would NWL to see $8.50 by expiration to break even. The trade is also protected through that date at a net buy-back price of $9.40. Plan two risks $0.40 and nothing more. That trader would need the stock to fall below $8.0 by expiration.

At the time of publication, Guilfoyle had no positions in any securities mentioned.