New Targets for Zscaler Ahead of Earnings

The cybersecurity firm is preparing to report and investors should consider this opportunity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Ready for some more high-end cybersecurity results? We've already heard from Palo Alto Networks PANW and CrowdStrike CRWD and both were well received by investors. These two names have traded back and forth, the unofficial title of "best in class" in the cybersecurity space for some time now.

Palo Alto beat Wall Street on both earnings and revenue generation, while providing fiscal 2025 guidance that was above Wall Street's expectations. CrowdStrike also beat Wall Street on both earnings and revenue, and while reducing forward looking expectations due to the infamous mass outages in July. However, those cuts were less severe than had been feared.

Cybersecurity is front and center in today's world. It is the key to everything, even cloud-based generative artificial intelligence, because if data is not secure, then everything is at risk. It had been thought that maybe one of my favorite "under the radar" cybersecurity firms, SentinelOne S had made inroads against CrowdStrike in July. Though SentinelOne reported a very solid quarter and issued solid guidance, there was no evidence that any progress had been made against its larger high-end competitor. SentinelOne has not done as well, post that release.

On Tuesday evening, one last high-end cybersecurity provider, Zscaler ZS will report for the season. There were not as many rumors (or at least I have not heard them) that Zscaler had taken market-share from CrowdStrike as there had been with SentinelOne. In one respect, that could be a negative. On the other hand, this removed one potential factor that could drive disappointment.

Expectations

For the firm's fiscal third quarter, which ended April 30, 2024, and was reported on May 30, 2024, Zscaler posted an adjusted EPS of $0.88 (GAAP EPS: $0.12) on revenue of $553.2 million. This crushed the Wall Street-wide consensus view across all three metrics, while the firm provided guidance for fiscal Q4 for revenue of $565 million to $567 million and adjusted EPS of $0.69 to $0.70. Both of those projections were above Wall Street's views at the time.

Roughly three months later, Zscaler is set to report those FQ4 numbers. The street is currently looking for an adjusted EPS print of $0.69 within a range of $0.68 to $0.76 on revenue of $567.7 million with a range of $563 million to $592 million. Prints like this would work out to (adjusted) earnings growth of almost 8% on revenue growth of about 25%.

Readers should know that ZS has beaten Wall Street for eight consecutive quarters and that since the start of the quarter, 33 of 33 sell-side analysts have increased their earnings estimates, while 31 of these analysts have also increased their revenue estimates. These analysts will be watching the above numbers closely. That's obvious, but they will also be watching for continued growth in deferred revenue as an indicator of sustained or even increased demand. At the end of that April quarter, deferred revenue stood at $1.577 billion, which was up 34% from April 2023.

Fundamentals

Operating cash flow and free cash flow printed at $108.5 million and $123.1 million, respectively, for the April quarter, which was up 18% year over year. That was good for an operating cash flow margin of 26% and a free cash flow margin of 22%.

Looking at the balance sheet, I see a fortress-like strength. The current ratio reflects a strong enough 1.75, but the reality is even better than that. As of the end of April, the cash position stood at $2.24 billion and short-term debt of less than $5 million along with long-term debt of $1.14 billion. While that means the firm could pay off its entire debt-load out of pocket almost twice over, once adjusted for deferred revenue, the above current ratio rises to a stunning 9.17. That's about as sound as balance sheets get.

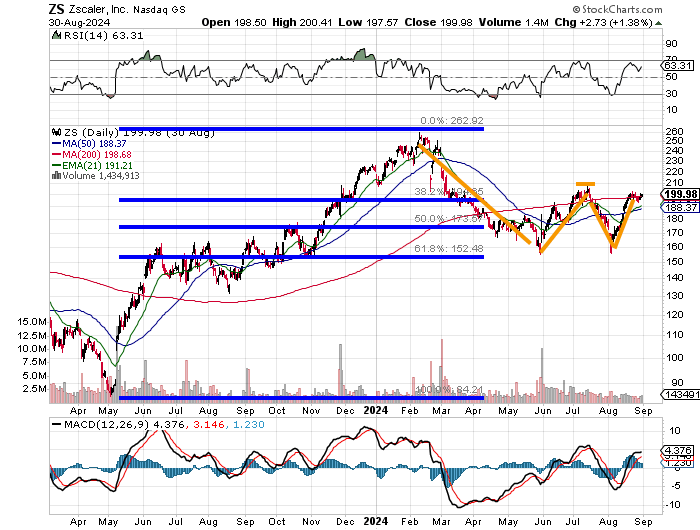

The Charts

Readers will see that ZS had rallied from early May 2023 into February 2024. From that point the stocks sold off into late May, where support was found for the first of two times at a rough 61.8% Fibonacci retracement of the already mentioned rally. Now, let's zoom in:

Now, ZS finds itself headed into earnings, with a near perfect double-bottom pattern of bullish reversal in place. The pattern runs with a pivot of $208. The stock has run sideways for a little more than a week after reaching its 200-day SMA, which may end up being more of a pivot than the one created by the midpoint of the double bottom "W" shape.

Relative strength is strong, but nowhere near being technically overbought, so there's plenty of room. On top of that, the daily MACD is postured bullishly with all three components in positive territory and with the 12-day EMA above the 26-day EMA.

Zscaler (ZS) Targets

- Pivot A: $198

- Pivot B: $208

- Target A: $237

- Target B: $249

- Add: Down to 50-day SMA (currently $188)

- Panic: Upon loss of all three key moving averages (200-day and 50-day SMAs, 21-day EMA)

At the time of publication, Guilfoyle was long CRWD, S equity.