We've Got a New Price Target for Oracle After CEO Reveals Guidance

Cloud computing giant Oracle has released its financial results and we've got a new strategy that can limit potential for loss.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday evening, software giant and number-four cloud computing services provider Oracle ORCL released the firm's fiscal fourth-quarter financial results.

Cloud computing services are dominated by Amazon AMZN, Microsoft MSFT and Alphabet GOOGL. For the three-month period that ended on May 31, 2024, Oracle posted an adjusted EPS of $1.63 (GAAP EPS: $1.11) on revenue of $14.287 billion. These top- and bottom-line results both fell short of Wall Street's expectations, while the sales print was good enough for year-over-year growth of just 3.3%. This was a deceleration in annual growth both from the quarter prior as well as the similar period a year earlier. The lion's share of the adjustment was made for stock-based compensation expense, which is a GAAP operating expense. Total remaining performance obligations increased by 44% during the quarter to $98 billion, while full fiscal year 2024 revenue printed up 6% at $53 billion.

Revenue by Category

- Total cloud (IaaS + SaaS) generated revenue of $5.3 billion (+20%)

- Cloud application (SaaS) generated revenue of $3.3 billion (+10%)

- Cloud infrastructure (IaaS) generated revenue of $2 billion (+42%)

- Fusion cloud ERP (SaaS) generated revenue of $800 million (+14%)

- NetSuite cloud ERP (SaaS) generated revenue of $800 million (+19%)

Operations

As revenue grew 3.3% to $14.287 billion, within that number, cloud services and license support drove revenue of $10.234 billion (+9%), and cloud license and on-premise license generated revenue of $1.838 billion (-15%). Hardware was good for sales of $842 million (-1%), while services contributed sales of $1.373 billion (-6%).

Operating expenses totaled $9.601 billion (-1%), leaving GAAP operating income of $4.686 billion (+13%). On an adjusted basis, operating expenses came to $7.618 billion, leaving a non-GAAP operating income of $6.669 billion(+8%). Operating margin printed at a GAAP 33%, up 288 bps or an adjusted 47%, up 219 bps.

After accounting for interest, taxes and other income/losses, net income landed at a GAAP $3.143 billion (-5%) and an adjusted $4.607 billion (-1%). This works out to a GAAP EPS of $1.11 versus $1.19 from the year ago period or an adjusted $1.63 versus $1.67 for the year ago comp.

Deals

"I'm pleased to announce that we've signed another multi-cloud partnership this time with Google," CEO Safra Catz said during the call. "OCI (Oracle Cloud) and Google Cloud Network interconnect is available immediately in 10 regions, and we will be live with Oracle database at Google Cloud in September, where customers can get direct access to Oracle Database Services running on OCI, deployed in Google Cloud data centers."

"At this moment, we have 76 customer-facing cloud regions live with 47 public cloud regions around the world and another 19 being built," Catz added. "We have 11 database(s) at Azure sites live and more locations with Microsoft coming online soon. We will have 12 Oracle database(s) at Google Cloud sites live this year. We also have 13 dedicated regions live and 15 more planned. We have several national security regions and EU sovereign regions live with increasing demand for more of each."

Guidance

The guidance was provided during the conference call, so if you've been going over the press release looking for it, you won't find much. For the current quarter, Catz told us that total cloud revenue should increase between 20% to 22% in USD. Adjusted EPS is seen growing 10% to 14% in USD, landing at $1.31 to $1.35. Wall Street was looking for something around $1.32 billion on $13.4 billion in revenue, which would be sales growth of just 7%, so this is strong guidance.

For the full year coming, Oracle sees further growth in RPO and cloud infrastructure services to grow faster than 50%. On the other side of the coin, Capex spending should double this year. Beyond the coming fiscal year, Catz says that the firm remains committed to its fiscal 2026 financial goals for sales, margin and earnings growth. The firm expects to put together a complete presentation on the matter at the Oracle One World conference this September in Las Vegas.

Fundamentals

For the fiscal year reported, Oracle generated operating cash flow of $18.673 billion. Out of this number came capex spending of $6.866 billion. This left free cash flow of $11.807 billion, up 39% from a year earlier. Out of that, the firm paid shareholders $4.391 billion in cash dividends, repurchases of $1.202 billion worth of common stock for the firm's treasury, and repurchases of $2.04 billion worth of stock for tax withholding purposes related to stock-based awards.

Looking at the balance sheet, we see a cash position of $10.661 billion and current assets of $22.554 billion. Current liabilities add up to $31.544 billion, which looks awful at first. Then one realizes that $9.313 billion of this number is labeled as deferred revenue, which is not a true financial obligation. That leaves a headline current ratio of 0.72, but that does improve to a passable (barely) 1.01 once adjusted for those deferred revenues. The firm does have short-term debt of $10.605 billion on the books.

Total assets amount to $140.976 billion, including $69.12 billion worth of goodwill and other intangibles. At 49% of total assets, that is alarmingly high. I would prefer to see tangible assets comprise a greater share of the total. Total liabilities less equity comes to $131.737 billion, including another $76.264 billion in debt labeled as non-current (or longer-term). Lets' face it: this firm is saddled with a lot of debt.

Wall Street

Not surprisingly, the community of analysts are not nearly as in love with Oracle this morning as are the keyword-reading algorithms that are focusing on the deal with Alphabet. Since these earnings were released last night, I have come across 12 highly-rated (four-plus stars at TipRanks) sell-side analysts that have opened on ORCL. Among these twelve, there are seven "hold" or hold-equivalent ratings and five "buy" or buy-equivalent ratings. Two of our "holds" have not set target prices, so we are working with just ten of those.

The average target price across our remaining ten analysts is $143.30 with a high of $171 (Mark Moerdler of Bernstein) and a low of $105 (Gil Luria of DA Davidson). Once we have omitted those two as potential outliers, the average target across the other eight rises to $144.63. Because I know that you want to know, the average "buy" target is $164.20, while the average "hold" target stands at $122.40.

My Thoughts

Investors, traders and algorithms alike all seem very excited about Oracle's guidance and planned cooperation with both Microsoft and Google. Still, there's this balance sheet that should be in much better shape than it is considering the size of the business and the cash flow it generates. It is a black eye and one can easily see that a majority of sell-side analysts are simply not that impressed. Nor am I.

The stock trades at 19-times forward-looking earnings and that's not really undervalued given the fundamentals. The good news is that with some discipline and maybe pulling back on the stock-based compensation (Oracle isn't a startup, is it?), those cash flows will go a long way toward fortifying the firm's foundation. Still, we need to see that discipline that has long been missing at Oracle.

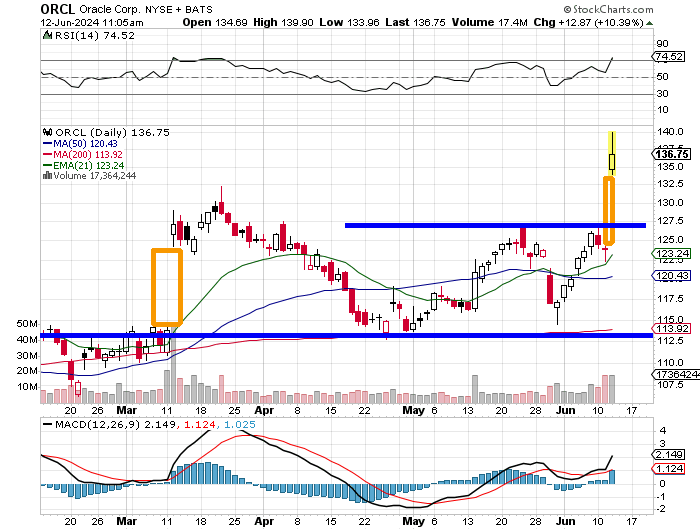

Readers will see the gap created when the firm reported fiscal third-quarter earnings back in March 2024. That gap ultimately filled. Now, suddenly, relative strength and the stock daily MACD are both greatly improved from where they were earlier in the week. My feeling is that the unfilled gap created this morning (that needs to see $125 to fill) has a very good chance of filling within a month or two. The stock can do that without even violating its 50-day or 200-day SMAs.

My instinct would be to short this move. The FOMC beach party is scheduled for Wednesday afternoon, and I do not want to stick my neck out ahead of those events. Right now, I am thinking that getting long an August 16, 2024 $140/$130 bear put spread for a net debit of roughly $3.85 is looking a lot more risk averse than actually shorting the equity today. This limits profit potential, while greatly reducing potential for loss.

At the time of publication, Guilfoyle was long AMZN and MSFT equity.