Keep Your Head on a Swivel, This Stock Presents Two-Way Risk for Investors

Watch out for the squeeze.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Beleaguered Medical Properties Trust MPW is trading sharply higher Monday in the wake of the REIT's announcement of the sale of its majority interest in five Utah hospitals. The sale of a 75% interest in these hospitals was made to a joint venture for $886M. MPW did retain a minority (25%) interest.

The joint venture also provided additional non-recourse secured funding of $190M in cash to MPW. Proceeds from these transactions will be used to reduce debt as well as for general corporate purposes.

This news comes almost directly on the heels of a deal that closed last Tuesday where MPW sold five medical properties to Prime Healthcare for a total of $350M in the form of cash ($250M) and an interest-bearing mortgage note ($100M) maturing in nine months. For four more facilities, the two firms agreed to a new 20-year lease that includes for Prime a $260M option to buy.

MPW Needed the Money

As of the end of fiscal 2023, over the prior 12 months, MPW generated a net loss of $556.1M and operating cash flow of $505.8M. On top of that, the REIT brought in a net $517.6 in cash flow from investing. Out of this number, MPW smartly paid down $988.2M in long-term debt.

Probably not so smartly, the REIT still paid out $615.4M in cash dividends to shareholders. MPW announced the next installment of its dividend payments Monday morning, which is adding to this pop in the share price.

Looking at the balance sheet, MPW had ended the year with very little cash on hand, just $250M. It had $10.999B in real estate assets, whose valuation is obviously subject to the will of the marketplace for commercial real estate. Against that, it had $133.5M in current debt and another $9.930.8B in long-term debt.

Earnings

MPW has had its problems. Year-over-year revenue generation decreased for nine consecutive quarters until the December quarter, where it grew thanks to some sales of properties.

For the first quarter (no reporting date), MPW is expected to be profitable, but on decreased revenue generation.

My Thoughts

The value of this REIT relies on the value of its real estate assets. This number is only running about $1B ahead of its total debt-load and that's the stated value of those assets.

Though medical facilities may not be as empty as some office buildings I have been in recently, rents for professional space are coming in, even in gentrified areas of New York, just to keep tenants from leaving.

I do not trust Monday's pop.

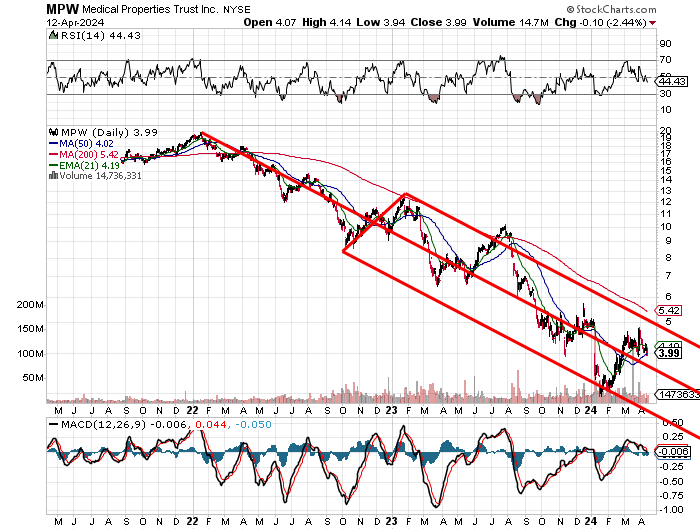

My thoughts are that MPW is a sale as it approaches the upper trendline of the above Pitchfork model and then up the 200-day simple moving average (SMA). The hitch here though is, and this is what the long and wrong crowd have to hope for, is that 48% of the entire float is held in short positions.

This stock is definitely a candidate for a short squeeze, so if one is in the name, be aware, especially after an earnings date is announced. This stock truly presents two-way risk for investors.

At the time of publication, Guilfoyle had no positions in any securities mentioned.