Is It Showtime for Paramount Global Buyers?

With Sony and Apollo reportedly in talks about a potential joint bid, here's what I think about the risk/reward proposition.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Is it time to buy Paramount Global PARA?

Looks like somebody already thought of that. No, Paramount Global does not trade below $10 per share, but it does trade close enough. No, Paramount Global is not a small-cap. With a market cap of under $7.5B, this company would be defined as a mid-cap, which we sort of quasi-cover in this space at times.

What Paramount is not, is a large-cap, major corporation, so being it almost trades at less than $10 and is not near being considered a large-cap, we will go there.

The stock is up about 12% Friday after the New York Times reported on Thursday that Sony Pictures Entertainment has been talking with Apollo Global Management APO about putting together a joint bid to acquire Paramount.

Last we heard, Paramount was possibly in discussions with SkyDance Media about potentially merging operations. Apollo, readers might recall, had previously made a cash offer for Paramount said to be worth up to $26B, and that was before Sony got involved. Remember, $26B is a lot for a company the marketplace values at less than $7.5B.

Paramount Is...

Kind of a mess, but with excellent brands and properties. What's inside includes Paramount Pictures, Republic Pictures, CBS News, CBS Sports, BET, MTV, and VH1. The list goes on to include Nickelodeon, Showtime, TV Land, Paramount+, Paramount Network and CMT. The crown jewels of the streaming service are the many series that reside under the Star Trek banner.

The company is set to report first-quarter earnings the week after next. Expectations are for adjusted earnings per share of $0.36 (GAAP loss per share of roughly $0.50) on revenue of $7.7B, which would show year-over-year growth of more than 6%.

Free cash flow over the 2023 calendar year amounted to just $56M. That sounds small and it is, but it was an improvement from -$500M for 2022. The company did take more than $2.3B in programming charges during the 2023 year.

As for the balance sheet, as of December, which is the most recent data we have, Paramount had a cash position of $2.46B and current assets of $12.7B. That measured up fairly well against current liabilities of $9.656B, leaving it with a current ratio of 1.32. Total assets amounted to $53.543B, of which about 34% was intangible. Total liabilities less equity came to $30.493B, which does include 414.6B in long-term debt.

The company has a decent enough balance sheet to meet short to medium-term obligations. The long-term debt-load is heavy. Cash flows would have to be improved upon prior to tackling that obstacle.

Paramount has not been an aggressive purchaser of its own stock in years so that's not a problem. The $389M in cash paid out as dividends last year would probably have to be reduced should it not dance with a new corporate partner any time soon.

My Thoughts

The business could make money if it can get out of its own way or if someone else ran the business. Cash flows have to improve and long-term the balance sheet would have to be better managed, but it's not awful in the short term.

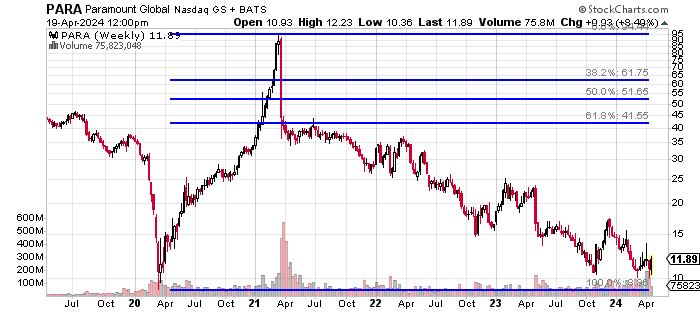

Readers will see on the weekly chart, above, that PARA has retraced almost its entire early 2020 to early 2021 rally that took the stock from about $10 per share to more than $101 per share.

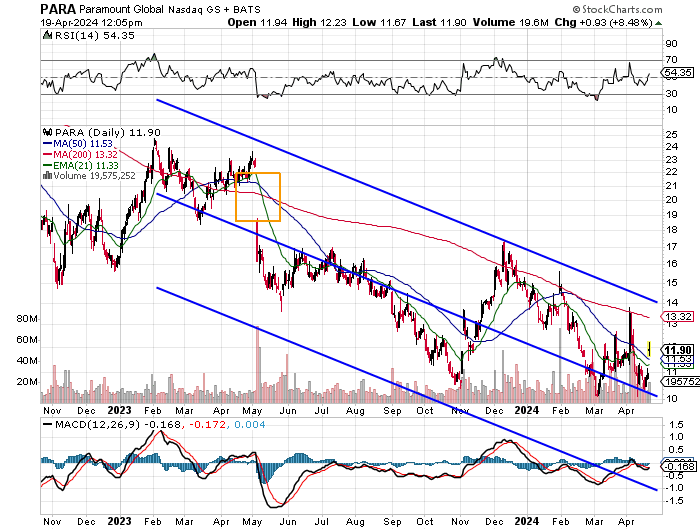

Switching over to the daily chart, readers will note that though PARA has been mired in a long downtrend, there seems to have been a floor put in at the $10 level. Now, if nothing happens with the company's suitors, this likely turns into a descending triangle. That's generally bearish, even if both relative strength and the daily Moving Average Convergence Divergence (MACD) are starting to look better.

That said, even up today, if Sony and Apollo do make a joint move on the stock, I don't think shareholders will be able to ask for much, but could profit, which has been tough of late in this market environment. A 200-day simple moving average (SMA) at $13.32 as a pivot would have me targeting $16.50 or so. That's reasonable. Even conservative if numbers like $26B were being thrown around.

If the whole ball of wax falls through, 15% of the float is still being held in short positions. There will be a bid. Somewhere. I think the risk/reward proposition is now worth it for some long-side speculation in this name.

I'll be entering once this piece is public.

At the time of publication, Guilfoyle had no positions in any securities mentioned.