Private Credit Contagion Will Spread as Market Ventures into Uncharted Territory

When else in history have equities traded at record highs while consumer sentiment readings were at record lows?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I am really struggling right now to find another time where my portfolio was trading at all-time highs and I felt such trepidation around the overall market.

It feels like we are in uncharted territory. When else in history have equities traded at record highs while consumer sentiment readings were at record lows? And yes, profits from the S&P 500 rose an impressive 28% year-over-year in the first quarter. However, if one strips out results from the technology and energy sectors, there was little earnings growth last quarter. The trailing P/E on the S&P technology sector reflects first quarter results moving from 32x at the March 30 lows to 48x.

Market dynamics feel like they are changing significantly on several fronts right now. In 2024, the major hyperscalers delivered nearly a combined $240 billion in free cash flow. However, huge increases to capex budgets have dramatically reduced free cash flows. This is having numerous impacts. Amazon (AMZN) has slashed 30,000 corporate employees since October 2025 to support its $200 billion capex budget for this year. Oracle (ORCL) and Meta Platforms (META) have recently significantly cut their employee count for the same reason. And yes, this surge of tech spending is powering job growth across much of the economy. Massive data centers create thousands of jobs in construction and assorted industries. However, these jobs are temporary. Once built and online, a data center takes very few full-time employees to operate.

The burst of capex spending helped pushed stock buybacks down by over 60% from Big Tech in Q1. Alphabet (GOOG) repurchased nearly $120 billion of its stock in 2024 and 2025, which boosted its EPS. This week, it is raising some $80 billion via various equity tranches. Debt issuance at the hyperscalers has also surged, much of it via off-balance sheet channels like special purpose vehicles. And now the upcoming IPOs from Space Exploration Technologies Corp (SPCX), Anthropic and OpenAI will suck roughly $200 billion out of other areas of the market.

There is clear deterioration within private credit as funds continuing to “gate” quarterly investor redemption requests, boosting fears around this sector. And that crossed over to private equity for the first time this week as Swiss based Partners Group Holding AG (PGPHF) only allowed just over half of requests to be redeemed in a $8.6 billion private equity fund, triggering a sell-off in its stock on Wednesday. I expect this “contagion” to continue to spread due to the duration mismatch between assets held by these funds and the ability of investor to redeem funds quarterly. At least, in theory.

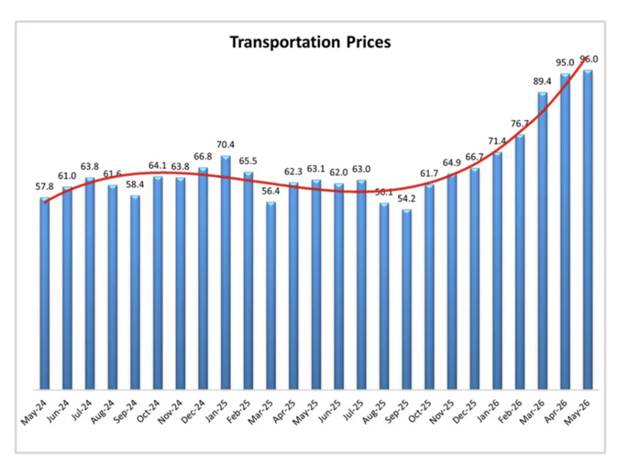

And then we have the cumulative impacts to the global economy from the effective closure of the Strait of Hormuz, which has been ongoing for over three months now. Investors continue to be way too lackadaisical around this issue. Fuel, fertilizer and transportation costs have surged this conflict commenced. A full three months of these impacts will be reflected in second quarter results, crimping profit margins in many sectors.

And a ceasefire that has held for two months seems to be fraying around the edges this week. An agreement to fully reopen this key global transit point seems like a pipe dream in the near term. In summary, the market is ignoring a lot of risks with its infatuation with all things AI, even as dynamics on other fronts are deteriorating.

At the time of publication, Jensen was long AMZN.