Investors Are Better Off Avoiding Capital One After Earnings Crush Expectation

Here's why Capital One Financial could be a trap for the bulls.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What's in your wallet?

If you went home on Thursday evening long Capital One Financial COF, the answer would be a few more dollars. After the closing bell on Thursday, Capital One Financial released the firm's third quarter financial results. For the period reported, the consumer lending/credit card giant posted an adjusted EPS of $4.51 (GAAP EPS: $4.41) on revenue of $10.014 billion. The earnings print crushed Wall Street's expectations, while the revenue number also beat and was good enough for year-over-year growth of 6.9%.

The 10-cent-per-share adjustment is largely connected to Discover DFS integration expenses. The firm would like the $35.3 billion all-stock deal, if approved by regulators, to close sometime in early 2025. Total non-interest expense increased 7%, the firm's provision for credit losses decreased by $1.4 billion to $2.5 billion. That number is brought about through net charge-offs of $2.6 billion and the release of $134 million in its loan reserve. Net interest margin was up 41 basis points to 7.11%, while the firm posted an efficiency ratio of 53.07% (52.53% adjusted) and an operating efficiency ratio of 41.95% (41.41% adjusted).

For those new to some of these terms, a bank or lender's efficiency ratio is derived by taking operating income less provisions and dividing non-interest expenses by that number. The lower, the better. Normally, you would really like to see that number below 50%, but numbers up in the 60% range are not uncommon. An operating ratio is simply expenses divided by net revenue. Below 50% is the goal.

Business Performance

Credit Card generated net revenue of $7.252 billion (+9.4%), making a $2.084 billion (+0.7%) provision for credit losses, producing income of $1.374 billion (+8.5%) after taxes. Average loans increased 2% to $154 billion. The average yield on loans outstanding is 19.66%, up from 19.02%. The 30-plus day delinquency rate is up to 4.54% from 4.32%. The level of accounts with FICO scores above 660 remains 69%.

Consumer Banking generated net revenue of $2.21 billion (-2.9%), making a $351 million (+64.8%) provision for credit losses, producing income of $403 million (-34%) after taxes. The average deposit's interest rate is 3.33%, up from 2.85%. Average loans increased 1% to $76.2 billion. Average auto loans increased 1% to $74.9 billion. The average yield on loans held is 8.88%, up from 7.97%. The 30-plus day delinquency rate is up to 6.31% from 6.27%. The level of accounts with FICO scores above 660 is 53%, up from 52%.

Commercial Banking generated net revenue of $888 million (-2.3%), making a $48 million (-58.6%) provision for credit losses, producing income of $263 million (+22.9%) after taxes. The average deposit's interest rate is 2.55%, down from 2.93%. Average loans decreased 1% to $88.1 billion. The average yield on loans held is 7.25%, up from 7.16%. The non-performing loan rate is 1.55%, up from 0.9%.

Wall Street

I have only come across five highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on COF since Thursday night. Three of the five rate the stock as a "buy" or buy-equivalent, while two analysts have a "hold" or hold-equivalent rating on COF.

The average target price across the five analysts is $167.60, with a high of $185 (John Hecht of Jefferies) and a low of $150 (David George of Robert W. Baird). The average "buy" target is $176, while the average "hold" target is $155.

My Thoughts

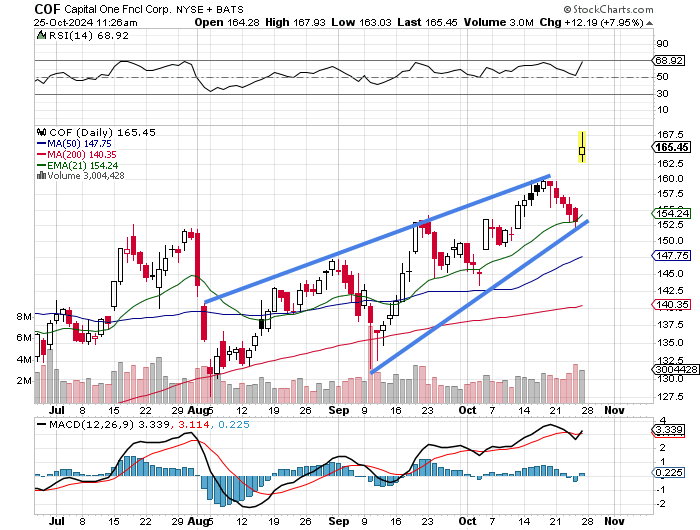

I thought the firm posted a solid quarter. Investors seem to agree. The stock is up almost 8% at mid-day, trading with a $165 handle. Yet, no one on Wall Street seems very enthused, not even the analysts who rate the stock as a "buy."

What I see is a rising-wedge pattern that has been in place since early August. The problem with that is that the stock just broke out to the upside, from a pattern associated with bearish reversals. Relative strength is spiking and the daily MACD has just gone bullish, with the 12-day EMA crossing above the 26-day EMA and the histogram of the 9-day EMA, which had just gone negative, moving back into positive territory.

The firm has done nothing wrong and is performing reasonably well. That said, the set-up going into earnings and the lack of enthusiasm on Wall Street have me thinking that I am missing something. This may be a trap for the bulls. I think I would rather be short this name, or better yet, simply take a pass, than get long on this pop.

At the time of publication, Guilfoyle had no positions in any securities mentioned.