I'm a Rocket Man! And My Price Target Is Taking Flight

Here's what's really got Wall Street excited about Rocket Lab USA — and why the stock is part of my long-term playbook.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sarge favorite Rocket Lab USA RKLB released its second-quarter financial results on Thursday evening.

For the three-month period ended June 30, the company posted a GAAP loss per share of $0.08, beating Wall Street expectations by a penny, and revenue of $106.251 million, which landed slightly below expectations. That said, the revenue number was good for sequential growth of 15%, good for year-over-year growth of 71.2%, and good enough to be the best quarter in Rocket Lab''s history.

The stock rallied significantly overnight, and not because of its current quarter guidance, which was good, but not great. The stock is rallying due to what has been revealed about it's near to medium term future.

For starters, Rocket Lab ended the second quarter with an order backlog of $1.07 billion. The Space Systems segment stands with an order backlog of $772.6 million as was expected, while the Launch segment stands with an above consensus backlog of $294 million.

Current Quarter Guidance

For the third quarter, Rocket Lab sees revenue of $100 million to $105 million, which is a bit below the $110 million that Wall Street had in mind. Space Systems is seen contributing $79 million to $84 million, while Launch is expected to contribute a rough $21 million.

The company does see an adjusted gross margin of 30% to 32%, which would be up at the midpoint from the second quarter's adjusted gross margin of 30.7%. GAAP gross margin is projected at 25% to 27%. Adjusted EBITDA is still expected to be on the wrong side of the ledger at -$33 million to -$31 million.

CEO Sir Peter Beck

-- On The Present... "On the small launch front, Electron remains the leading small rocket globally with successful launches in the quarter for government and commercial customers, and demand for it continues to grow with 17 new launches signed so far this year. "

- On The Future... "We reached a critical milestone in the development of our new medium lift rocket Neutron, with the successful completion of the first hot fire for the Archimedes engine. Over the same period, we made significant progress in Neutron production and launch infrastructure with the scaling of engine production facilities, installation of the automated fiber placement machine that will produce Neutron’s largest carbon fiber structures, and we furthered development of Launch Complex 3 and the integration and assembly facility on site in Wallops, Virginia."

From the Call

Here is where we got where the company is really trying to go. The two quotes came from the press release. This beauty from Beck came from the call: "By owning launch and spacecraft, we're at a distinct advantage when it comes to establishing our own space capabilities or constellations. We can build and launch our own spacecraft at cost, and we don't have to wait in-line for limited launch capacity."

You caught that, right? Their own constellations, so the firm can meet the growing demand for space-driven data and space services at much lower cost.

Beck added to that thought: "We completely avoid the pain point that most constellation operators face, being at the mercy of suppliers on cost and schedule, often causing deeply disruptive delays and bringing capability online at scale." Beck added that Rocket Lab is not ready for this yet, but that's where they are headed, and that's what got Wall Street excited overnight.

Fundamentals

For the first half of 2024, Rocket Lab posted operating cash flow of -$15.6 million. Tack on capex spending of $34.5 million, and the company is left with six-month free cash flow of -$50.1 million. The company obviously does not return capital to shareholders.

Moving on to the balance sheet, Rocket Lab ended the period reported with a cash position of $496.7 million, inventories of $104.5 million and current assets of $751.8 million. Current liabilities add up to $266.4 million, including $11.3 million in installment payments to made on longer-term debt. This puts the company's current and quick ratios at 1.86 and 1.47, respectively. These are healthy enough ratios.

Total assets amount to $1.189 billion, including $135.2 million worth of goodwill and other intangibles. At just 11% of total assets, this does not raise eyebrows. Total liabilities less equity comes to $733.4 million, including $394.3 million in long-term debt, most of which is in the form of senior convertible notes.

This is a clean balance sheet. There is enough cash on hand to take care of the entire debt-load. The one concern for investors here is that with what is about $344 million worth of convertible notes outstanding, the equity could and will if things go well for the shares, be diluted.

Wall Street Weighs In

Since these earnings were released Thursday night, I have seen two highly rated (these guys are both rated at 5 stars by TipRanks) sell-side analysts opine on RKLB.

Ronald Epstein of Bank of America reiterated his "buy" rating and $10 price target due to Rocket Lab's impressive revenue growth and successful advancement of current aerospace projects. Elsewhere, Erik Rasmussen of Stifel Nicolaus reiterated both his "buy" rating and $9 target price.

My Thoughts

The growth in sales is impressive. The short-term guidance is conservative, but the long-term vision is exciting. Current cash flows, like profitability are still in the future, but the balance sheet is strong, in fact very strong.

It's probably no surprise to my readers that I am long this stock and I consider it a core member of my long-term playbook along with Palantir Technologies PLTR and SoFi Technologies SOFI.

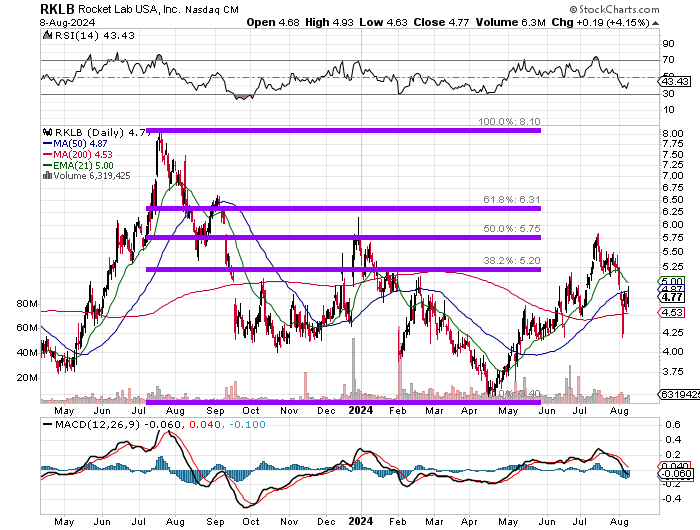

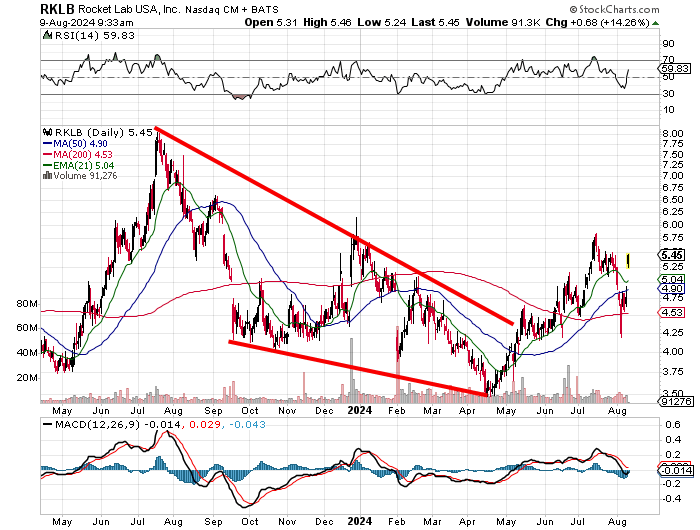

Readers will see above that the previous rally was halted at the stock's half-way back point in July (retracing the July 2023 through April 2024 selloff). I had drawn up a Pitchfork model for you that has now broken down the last time I covered this name.

I now see something else:

Rocket Lab USA had been mired in a Falling Wedge pattern during that selloff, which we all know is a pattern of bullish reversal. The stock did run into some sellers this summer but appears to have found intense support once the 200-day simple moving average (SMA) was put to the test.

The stock has now retaken not only the 200-day and 50-day lines for the portfolio managers, but the 21-day exponential moving average (EMA) for the swing crowd. This moves the pivot up to $5.85 (the July high) from $5.60.

Rocket Lab USA (RKLB)

Price Target: $7.50 (up from $7.25)

Pivot: $5.85 (up from $5.60)

Add: Down to the 50-day SMA

Panic: Loss of the 200-day SMA

At the time of publication, Guilfoyle was long RKLB equity.