I Just Might See a Way to Play The Children's Place

This balance sheet is one of the worst I have looked at in some time, but if you look past that, you could find a trade.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Remember The Children's Place PLCE? There used to be one in my local mall. Hasn't for a while, though. This used to be a stock that showed great promise. It was one of Jim Cramer's up and comers back in the day. He wasn't wrong. The stock marched almost straight up over the first 20 or so years of its existence, peaking in the $150s back in 2018.

The stock traded below $10 at the depths of the 2020 pandemic lockdowns and as high as $82.95 in late 2021. The stock closed at $4.90 on Tuesday night ahead of Wednesday morning's earnings release. On Wednesday, the stock gapped up on the open and not only held those gains throughout the session but punched higher. The stock closed on Wednesday afternoon at $9.10, up 85.7% on the day, but for our purposes, remains a "small cap" and remains a stock that trades under $10.

Let's see how ugly things look, but why there just might be something to ... play with here.

Earnings, Making Adjustments

For the second fiscal quarter, which ended Aug. 3, The Children's Place posted an adjusted earnings per share of $0.30 (an unadjusted loss per share of $2.51) on revenue of $319.655 million. While the top-line print fell short of expectations and reflected year-over-year contraction of 7.5%, the adjusted bottom line print beat Wall Street. By a lot. Wall Street was looking for a rough loss per share of $1.45 for that line.

The lion's share of what adds up to $2.81 per share's worth of adjustments were made for asset impairment charges related to the "Gymboree" brand name and restructuring costs. While I am tempted to get excited over this release, it is time that the stock took on its problems, and about 45% of the entire float was held in short positions coming into this release. So, we can't know just yet how much of this surge was merely a short squeeze and not organic buyers taking on or expanding long positions.

From the Press Release...

"The decrease in net sales was primarily driven by an anticipated decrease in ecommerce revenue, as the company proactively rationalized its unprofitable promotional strategies, inflated marketing spend and “free shipping” offers to significantly improve profitability, which was successful during the second quarter. These efforts not only improved the profitability of the Company’s ecommerce business, despite the lower revenue, but also benefited the brick-and-mortar channel, as the stores business experienced positive comparable store sales for the first time in ten quarters. The wholesale business also rebounded with double-digit growth after a decline in the first quarter." Comp sales decreased 7.2% overall, but the physical stores did experience positive comps.

On that strategy, interim CEO Muhammad Umair commented, "While we anticipated that these efforts would provide pressure to topline sales, we drove significant improvements in gross profit margin versus the prior year’s second quarter and sequential improvement in margin for two quarters, which is particularly important moving from the first quarter to the second quarter. In addition, we were also able to significantly decrease Adjusted SG&A expenses as we reduced payroll costs and eliminated unprofitable marketing spend, all of which has combined to show more than a $39 million improvement in Adjusted operating income despite the lower top line sales."

Operations

As sales were contracting 7.5% to $319.655 million, the cost of sales dropped 19.4% to $207.861 million. This left a gross profit of $111.794 million (+27.4%) as gross margin improved from 25.4% to 35%. Normal operating expenses decreased 14.2% to $96.065 million. Add to that depreciation and amortization of $9.505 million and those impairment charges of $28 million, and the company was left with a unadjusted operating loss of $21.776 million, up from a loss of $36.941 million. After accounting for interest, and taxes, unadjusted net loss printed at $32.114 million, up from a loss of $35.355 million.

This worked out to a an unadjusted loss per share of $2.51, up from the year-ago comp of a loss of $2.82. After applying the adjustments, net income/loss improved to $3.893 million from a loss of $26.493 million, for an adjusted EPS of $0.30, up from a loss of $2.12 a year ago.

Fundamentals: Ouch

This is not going to be pretty. Then again, what did you expect? For the quarter reported, The Children's Place generated operating cash loss of $194.687 million, down from a loss of $32.705 million for the year-ago comp. Specifics on capital spending were not made in the materials at hand.

The retailer ended the period with a cash position of $9.573 million and inventories of $520.593 million to get current assets to $627.343 million. Current liabilities add up to $698.516 million, including $316.655 million in a revolving loan facility and $67.61 million in operating lease liabilities. This puts the current ratio at 0.89 and its quick ratio at 0.15. These ratios are well below what Wall Street usually considers to be acceptable.

Total assets amount to $921.414 million (remember including $520 million in inventories that may or may not be worth that much). There is no entry made for goodwill or other intangibles. Total liabilities less equity comes to $990.286 million, including another $165.354 million in long-term debt. This balance sheet is in tough shape.

My Thoughts

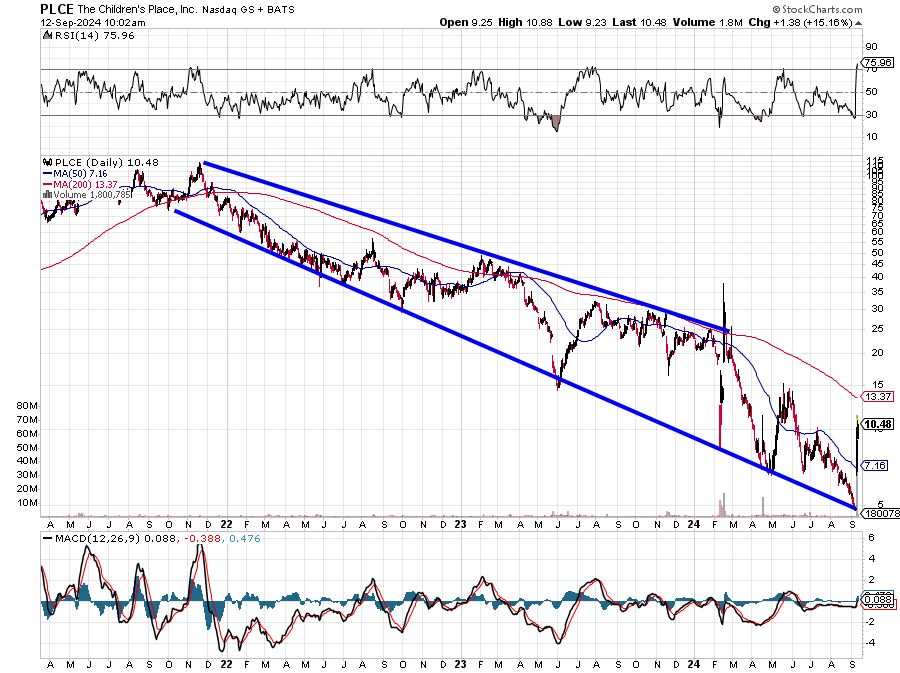

This is a really tough bandwagon to jump on. The company is still, on an unadjusted basis, losing tons of money per share. The "surprise" profitability came courtesy of sizable impairment charges. Cash flows are deeply negative. The balance sheet is one of the worst I have looked at in some time. The stock is up an additional 15% or more since the opening bell. I now see it trading above $10.

Just look at that three-year trendline of precipitously falling support. The company's reading for Relative Strength is already short-term overbought. The stock has retaken its 50-day simple moving average, but I seriously doubt very many institutions are looking to get involved here. I really do think this is a short squeeze. For a trade, if one has the risk tolerance, I guess one can do what one wants. As an investment, I would not touch this one with a 10-foot pole. It's even hard to like as a short idea with 45% of the float already there. I don't like to short stocks once that number hits 8%.

I might -- I stress "might" -- look to get long a bear put spread in this one. One idea would be to pay $1.75 for Oct. 18 $9 puts and sell Oct. 18 $7 puts for about $0.85. The net debit would be about $0.90, and the traders would be trying to win back $2 best case for 122% profit. Not a ton of risk, limited but decent potential.

At the time of publication, Guilfoyle had no position in any security mentioned.