Home Depot Can Right the Ship Without Touching Its Dividend

Even after a concerning financial report, the home improvement giant can still do what needs to be done.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Home Depot HD has reported and it wasn't that pretty.

On Tuesday morning, ahead of Walmart WMT and July Retail Sales later this week, Home Depot reported the firm's second quarter financial performance. The look we got at the condition of the U.S. consumer, from this take, would have to be seen as troubling. For the three-month period ended July 28, 2024, Home Depot posted an adjusted EPS of $4.67 or GAAP EPS of $4.40 on revenue of $43.175 billion.

These top- and bottom-line results both beat Wall Street's expectations, while the sales number showed year-over-year growth of 0.6%. Total revenue includes approximately six weeks of sales related to the recent acquisition of SRS Distribution Inc. Some of the nitty gritty is a bit rough to look at.

Comparable sales decreased 3.3% firm-wide versus expectations for -2.4%. Comparable U.S. sales were down 3.6% versus expectations for -2.6%. Customer transactions were down 1.8% to 451 million, as the average ticket was down 1.35 to $88.90. Sales per square foot dropped 3.6% to $660.17.

The CEO

President and CEO Ted Decker commented in the press release: "The underlying long-term fundamentals supporting home improvement demand are strong."

Then, Decker lowered the boom: "During the quarter, higher interest rates and greater macro-economic uncertainty pressured consumer demand more broadly, resulting in weaker spend across home improvement projects. However, the team continued to navigate this unique environment while executing at a high level."

Operations

While revenue was growing 0.6%, even with some help from an acquisition, the cost of sales remained flat, leaving a gross profit of $14.416 billion (+1.8%) as gross margin improved from 32.9% to 33.4%. Operating expenses increased 4.1% to $7.882 billion, which left an operating income of $6.534 billion (-0.8%). Operating margin dropped from 15.4% for the year-ago period to 15.1%. After accounting for interest and taxes, net income dropped 1.1% from $4.659 billion to $4.561 billion. This works out to $4.60 per fully diluted share, down from $4.65 a year ago.

Guidance

For the full year, the firm expects total sales to increase between 2.5% and 3.5% including a 53rd week that should pad the number by a rough $2.3 billion. The SRS acquisition is expected to add about $6.4 billion to the total.

Comp sales are seen decreasing by 3% to 4% from fiscal 2023. Comp sales of -3% would imply a consumer demand environment consistent with the first six months of this fiscal year. However, comp sales are not currently on a trajectory to meet the low end of that range. A 4% decrease implies incremental pressure on consumer demand. The firm had previously guided towards a decline of just 1%.

Beyond those projected comparisons, gross margin is seen up around 33.5%, while operating margin is seen down around 13.5% to 13.6%. The firm had issued previous guidance for a full year operating margin of 14.1%. Adjusted EPS is seen decreasing between 1% and 3% on a 53-week basis.

Fundamentals

For the first six months of the fiscal year, Home Depot has generated an operating cash flow of $10.906 billion. Out of that number came capex spending of $1.566 billion, leaving free cash flow of $9.24 billion, so the firm is still a free cash flow beast. Out of that number came the repurchase of $649 million worth of common stock and cash dividend payments of $4.46 billion to shareholders.

For the period reported, Home Depot ran with a cash position of $1.613 billion and merchandise inventories of $23.06 billion. That put current assets at $32.273 billion. Current liabilities add up to $28.123 billion including short-term debt of $2.527 billion and accrued installments of $1.339 billion on the firm's long-term debt.

That leaves the firm with a current ratio of 1.15, which passes muster. Obviously, the quick ratio would be awful, but we tend to cut retailers some slack on their quick ratios given the inventory-centric nature of the business. What is sub-optimal here is the paltry cash position and the almost $3 billion in debt that will have to be repaid or refinanced within 12 months. This is where that free cash flow is going to be key, and why it was important for the firm to stop repurchasing shares. This is do-able, but management has to stay disciplined.

Total assets amount to $96.846 billion including $28.628 billion in goodwill and other intangibles. At 29% of total assets, this is high enough to keep an eye on, but not high enough to impact current opinion on the stock. Total liabilities less equity comes to $92.426 billion. This includes another $51.869 billion in long-term debt. As we said, good thing this firm is a cash flow beast because it's going to need to be.

My Thoughts

The debt-load is daunting, and the cash balance is somewhat depleted. That said, the firm still prints cash and can do what it needs to do as long as it doesn't do anything stupid. This can be done (in my opinion) without touching the $9 annual dividend which yields a healthy 2.6%. The balance sheet certainly is not the strength of this firm fundamentally, as the cash flows are. Certainly not a lost cause. The stock trades at nearly 23-times forward-looking earnings and may have to be retried down 21-times or so. I know that I would not pay 23-times in a slowing economic environment for a debt-heavy, consumer-dependent firm.

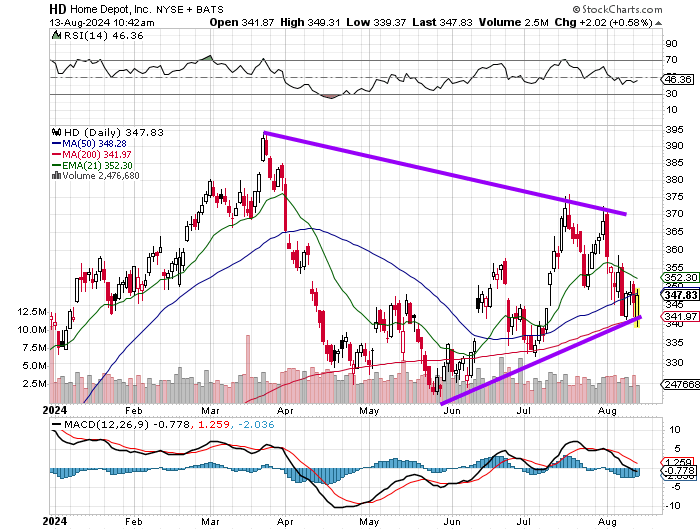

What I think I see here is a still-under-developed symmetrical triangle. The triangle would have to close, if I am correct, to create an explosive outcome one way or the other. The shares are trading higher since the opening bell and would need to trade higher than this to keep the triangle in play. For a trade, that's fine. I already told you that for fundamental reasons, I do not currently see HD as an investment.

Relative strength is neutral. The daily MACD has a bearish setup to it. The shares are fighting to hold their 50-day SMA after testing their 200-day SMA. If that can be done, the swing traders may have enough juice to go after the 21-day EMA.

A trader, respectful of the range, but with considerable tolerance for risk could go out a couple of weeks to August 30, 2024 expiration and sell a $340 put and a $370 call for a rough $6. To cap the risk the same trader could purchase a $330 put and a $380 call for less than $3.

At the time of publication, Guilfoyle was long WMT equity.