Here's What's Better Than Throwing Money at Airbnb Right Now

What does Leap Day and Easter have to do with Q2 guidance?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Executing at a high level. Guidance that fails to impress. The share price makes like a pea rolling off of a table. This is that story.

Airbnb ABNB released the firm's first quarter financial results on Wednesday afternoon. For the three-month period ended March 31st, Airbnb posted a GAAP EPS of $0.41, easily beating expectations, on revenue of $2.142B. Not only did the sales print beat Wall Street, but it was also good for annual growth of 18%. The pace of that revenue growth was in line with what the firm has regularly produced over the three quarters prior and a slight acceleration from Q4 2023.

Within these numbers, performance was driven by 9.5% growth in Nights and Experiences booked to 11.5M. This, in turn, produced a 12% increase in gross booking value (GBV) as well as a "modest" increase in average daily rate (ADR).

What also boosted these Q1 numbers, but impacted forward guidance, was the early Easter (moved from Q2 to Q1), and the inclusion of a "leap day" in Q1. Adjusted EBITDA did improve an impressive 62% to $424M relative to the comparable quarter a year ago.

Operations

You already know that revenue generation ramped 18% to $2.142B. Total costs and expenses increased 12% to $2.041B. This left the firm's operating income/loss at $101M, up from $-5M. That was good for an operating margin of 4.7%, up from negative territory. After accounting interest, taxes, and other income and expenses, net income printed at $264M (+125%, for real). This works out to a GAAP EPS of $0.41, up from $0.18 for the year ago comp.

Outlook

For the current quarter, Airbnb is projecting revenue generation of $2.68B to $2.74B, which would be good for year over year growth of 8% to 10%. This was taken negatively by the market as Wall Street was looking for $2.74B, and this would be a clear y/y deceleration in sales growth from the four quarters prior. On top of Easter and Leap Day, the firm mentions FX headwinds as a third reason for this expected underperformance.

The firm does see robust demand for the upcoming summer season as international events such as the Olympics and the Euro Cup should drive cross-border travel. Revenue growth is expected to accelerate sequentially from the current quarter into Q3.

For the current quarter, growth in nights booked should be in line with Q1, and ADR for the period is expected to rise modestly. Adjusted Q2 EBITDA is seen as flat to up on a nominal basis, but down on a margin basis relative to the year ago comps. The expected margin compression will come at the hands of the Easter shift - hearing a lot about that - and increased marketing expenses.

Fundamentals

For the quarter reported, Airbnb generated operating cash flow of $1.923B. Out of this came just $14M in Capex spending. This left a whopping free cash flow of $1.909B. Out of this number, the firm repurchased $750M shares of common stock for its treasury and moved the rest into cash.

Glancing at the balance sheet, Airbnb ended the period with a cash position of $11.093B and current assets of $20.393B. Current liabilities add up to $14.139B, including $2.434 in unearned fees, but no shorter-term debt. That leaves Airbnb with a strong current ratio of 1.44, and if adjusted for unearned fees (that are not a financial obligation), this ratio rises to 1.74.

Total assets amount to $24.537B, including just $786M in goodwill and other intangibles. At 3% of total assets, this is no issue at all. Total liabilities less equity comes to $16.641B, which does include long-term debt of $1.992B. The firm could pay this off out of pocket more than five times over if need be. This is a good example of a well-constructed, solid balance sheet.

Wall Street

Since these earnings were released, I have come across 19 highly rated (4+ stars at TipRanks) that have opined on ABNB. Among these 19 analysts, we have quite a divergence in opinion. We have four "buy" or buy-equivalent ratings, 12 "hold" or hold-equivalent ratings and three outright "sell" or sell-equivalent ratings. Three of these "holds" did not set targets, so we are working with 16 of those.

The average target price across the remaining 16 sell-side analysts is $153.19 with a high of $200 (James Lee of Mizuho Securities) and a low of $120 (Brian Nowak of Morgan Stanley). Once we omit those two as potential outliers, the average target price across the other 14 analysts drops to $152.21.

Because I can hear you asking, the average "buy" target is an even $183, the average "hold" target is $149.11, and the average "sell" target is $125.67.

My Thoughts

The execution is solid. I am not thrilled about how many times the firm brought up Easter falling in Q1 this year and Leap Day as excuses for less than fantastic Q2 guidance. That's problematic. Easter is the holiest day on the Christian calendar, but it falls on a Sunday. I am somewhat religious.

While spring break happens every year and spring travel revolves around spring break, I don't know anyone who travels or takes time off based on where Easter falls on the calendar unless their kids are in Catholic school, which is not a high percentage of students. Leap Day is one day every four years. Get over it.

So, the guidance for sharply reduced Q2 growth from what the firm has experienced for years, is in my opinion, for real. Looking out over the rest of the year, Wall Street is looking for year over year growth rates of 13%, 12% and then 10% to round things up. What? Are they moving Easter or some other "travel" holiday four times this year? I missed that memo.

Fundamentally, the books look good. The firm is profitable, cash flows are strong, and the balance sheet is close to exceptional. The question becomes, does a good business that produces solid cash flow, but whose growth is decelerating, still deserve to trade at 36 times forward looking sales? The answer is... probably not.

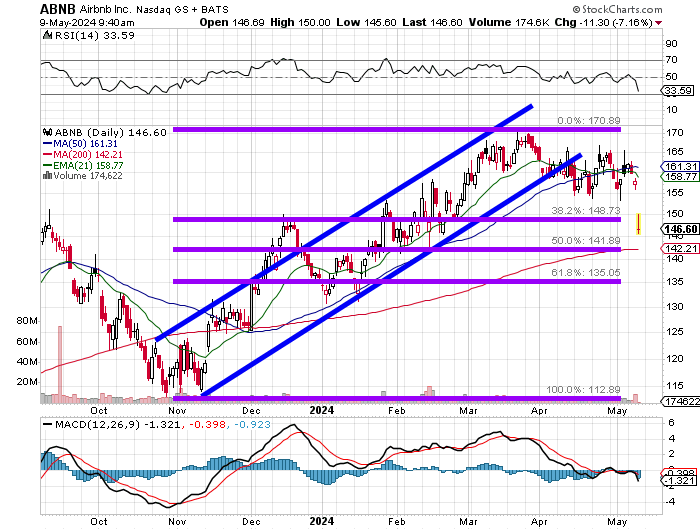

Readers will see that ABNB had been in an ascending price channel that lasted from late October to late March, before going into a basing period of consolidation.

We see that today, the stock broke through the $153 support for that base. Relative strength has gone south as have all three components of the daily MACD (moving average convergence divergence). The stock broke through the 38.2% Fibonacci retracement level of the entire October through March rally this morning and is currently trying to regain that level.

Personally, I would not be surprised to see the stock in the coming days move towards the "half-way back" point at $142, especially as that line is currently running concurrently with the stock's 200-day SMA (simple moving average).

I would not at this time consider an entry trade on the long side until I see that spot tested. For those interested, the June 21st $145 puts are currently paying a rough $5.40. Even if the trader does get tagged and has to eat the shares, that would be a net basis of $139.60. In my opinion, better than throwing a bunch of money at the equity right now.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.