An Option Strategy for a Small-Cap Healthcare Name

Several insiders purchased just over 180,000 shares in total during mid-May, always a nice vote of confidence.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equities continue to trade right at all-time highs despite a number of key challenges including a recent surge of inflation pressures, a bifurcated market and economy as well as extreme valuation levels viewed by a variety of historical metrics.

Finding bargains in this market feels as challenging as finding birdie opportunities at Shinnecock. However, this just means an investor just has to put more effort into separating the wheat from the chaff.

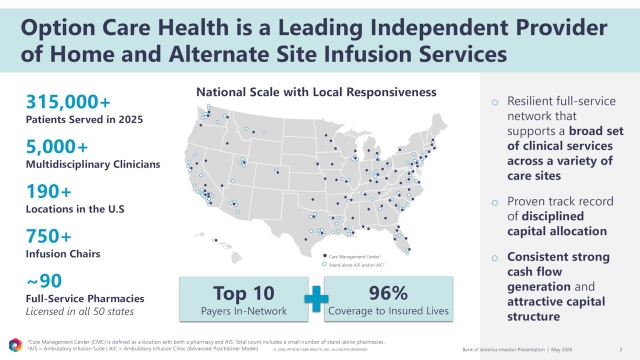

In today’s article, I highlight a small-cap name that sports a reasonable valuation within an overbought market. The name of the company is Option Care Health, Inc (OPCH).

This is a provider of home and alternative site infusion services, as well as other ancillary post-acute care to patients through various facilities in over 40 states. The company treated over 300,000 individuals in 2025 and delivered some 2.5 million transfusions. The stock currently trades around $22.00 a share and sports an approximate market capitalization of $3.4 billion.

This is not a market that gets much attention in the financial press, but it is considerable. The domestic infusion market is roughly $100 billion annually. Home and alternate site infusion capabilities representing approximately one-quarter of that opportunity and is benefiting from the aging of the U.S. population. This sizable niche of the market is projected to grow in the high single digits annually through at least the end of this decade.

Option Care has approximately one quarter of the domestic home infusion market. Nearly 90% of its FY2025 revenue was derived from commercial payers it should be noted. Option Care has grown both organically and via a series of small strategic “bolt on” purchases in recent years. Since 2021, management has done seven of these types of acquisition for a total outlay of just over $300 million.

The shares of Option Care Health are down some 30% in 2026. This decline has largely been due to its top infusion med (Stelara) losing patent exclusivity, which lowered reference price and reimbursement dynamics. Of note, no therapy in the company’s broad product portfolio accounted for more than 4% of overall profit in FY2025. Management did lower FY2026 guidance from $5.9 billion to $5.73 billion.

The pullback in the stock has brought in some recent insider buying in the shares. Several insiders purchased just over 180,000 shares in total during mid-May, always a nice vote of confidence. The company’s balance sheet is in good shape, and it has $675 million left on an existing stock repurchase agreement.

The current analyst firm consensus has Option Care Health growing profits by the mid-teens in both FY2026 and FY2027 to $1.45 a share and $1.67 a share, respectively. That values the stock at reasonable 15 times this year’s profits and puts it with a PEG ratio of just over one. I can make this valuation cheaper via the following option strategy.

Option Strategy:

Here is how one can establish a position in OPCH using a covered call strategy. Selecting the December $20 call strikes, fashion a covered call order with a net debit in the $17.50 to $18.00 a share range (net stock price – option premium). This strategy delivers downside protection of almost 20% across the trade expiration with nearly 13% upside potential even if the stock trades down 10% over the option duration.

At the time of publication, Jensen was long OPCH.