Giving Palo Alto Another Chance: Here Are 2 Trade Ideas

In 'best in class' cybersecurity stocks, there's CrowdStrike, SentinelOne, and now perhaps Palo Alto.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Cybersecurity giant Palo Alto Networks PANW will go to the tape with the firm's fiscal third quarter financial results on Monday evening after the closing bells at 11 Wall Street and up at Times Square.

Readers with good memories may remember that I lost some faith in Palo Alto several months ago, and moved resources out of Palo Alto, the name I had once referred to as "best in class" and beefed up my exposure to CrowdStrike CRWD. I had felt after doing as much research in the ace as I could understand that CrowdStrike had stripped Palo Alto of that title. I did get back into PANW on the post-earnings weakness in February, but that was just a short-term trade -- that worked very well, out two weeks later +12%.

I have always maintained that cybersecurity is a space where though valuations are off the chart, demand going forward will likely be inelastic, regardless of broad strength or weakness across the economy. I had always maintained three longs in cybersecurity in my investment (not trading) book.

The three have always included "best in class", a smaller firm with a good product and a shot... for me that's been SentinelOne S. Those two have worked out well. We're up more than 100% in CRWD despite the lack of progress over the past few months. We're still up 23% in S despite being well off if its winter highs.

That third spot has been rough though. Our original out in PANW was well-timed as was our short-term trade. The portion reallocated to CRWD has not hurt us. We also allocated a portion to Zscaler ZS, which we are no longer in, and that did hurt us. I have an 8% rule for a reason. Though Palantir Technologies PLTR does many things and security is in the broad array of applications for its platforms, I still consider it more big data/surveillance than frontline cybersecurity. So, here I am, still looking for a third dance partner, and here comes Palo Alto Networks, looking for another chance.

Expectations

Readers will likely recall that back on February 20th, Palo Alto posted an adjusted EPS of $1.46, a GAAP EPS of $4.89, and revenue of $1.98B for the firm's fiscal second quarter. All three metrics easily beat expectations. Remaining performance obligation had grown 22%, as adjusted operating margin grew 580 basis points from the year ago comp to 29%. All good, so one might think.

The guidance provided at the time was not what had been projected by Wall Street. For the third fiscal quarter (tonight's release), the firm projected revenue of $1.95B to $1.98B, with Wall Street looking for $2.04B at the time. Wall Street has since come down to $1.97B on that metric, which would be good for growth of a rough 14%. This would reflect Palo Alto's slowest pace of revenue growth in at least five years. That's how far I went back.

The firm guided towards FQ3 billings of $2.3B to $2.35B in February, which was well below the $2.6+B that Wall Street had in mind. Palo Alto is heavily covered. We see that over the past three months, 31 sell-side analysts reduced earnings estimates for tonight's report, while six sell-side analysts went the other way and increased estimates.

It was not just the quarter. For the full year, Palo Alto guided billings toward $10.1B to $10.2B, which was down from previous guidance of $10.7B to $10.8B. The firm knocked its revenue guidance down from $8.15B-$8.2B to $7.95B-$8B. Wall Street is currently at $7.98B on this number.

PANW also projected a full year adjusted EPS of between $5.45 and $5.55, which took the midpoint of that range below the $5.52 Wall Street consensus in February. Wall Street is at $5.51 now. Needless to say, the stock dropped 28.4% in less than 24 hours after that release and only started recovering in late April/early May.

The Backdrop

Palo Alto, whether or not a 51 times forward looking earnings valuation is justified or not, is a cash flow beast. For the quarter reported in February, Palo Alto generated operating cash flow of $690M and free cash flow of $654.8M. For the trailing twelve months, the firm has generated operating free cash flow of $3.062B and free cash flow of $2.922B. Out of that, the firm has not paid dividends and has bought back just a small amount of stock. They did pay down a significant portion of debt, which was smart.

The firm entered the quarter to be reported later with a cash position of $3.371B and a current ratio of just 0.83. This is misleading as almost 2/3 of the firm's current liabilities fall under the entry for unearned revenue, which we know is not a true financial obligation. Adjusted for unearned revenue, the firm's current ratio improved to very beefy 2.27.

The firm still has shorter-term debt of $1.822B on the books, which will have to be dealt with this year. Should the firm decide not to refinance any of that debt at today's higher interest rates, the cash is there to do that. There was, at least as of February, no long-term debt on the books.

This is a very clean balance sheet, on the doorstep of being an exceptional one. I really can't wait to see how this balance sheet has evolved tonight. It may or may not be key to note that as of the end of the previous quarter, Palo Alto Networks ran with a tangible book value of $1.69 per share, which was by far, the firm's strongest print in that space at any point in recent memory.

The problem is that PANW just is not a growth stock anymore. CrowdStrike trades at an even more gaudy 88 times forward looking earnings, but Wall Street is still looking for something close to 31% revenue growth there, not 14%. Zscaler is still trading at 55 times forward looking earnings and is expected to post revenue growth of 28%. There probably is a good fundamental reason not to buy PANW ahead of earnings, as the expected pace of growth is really just nowhere near that of its key competitors.

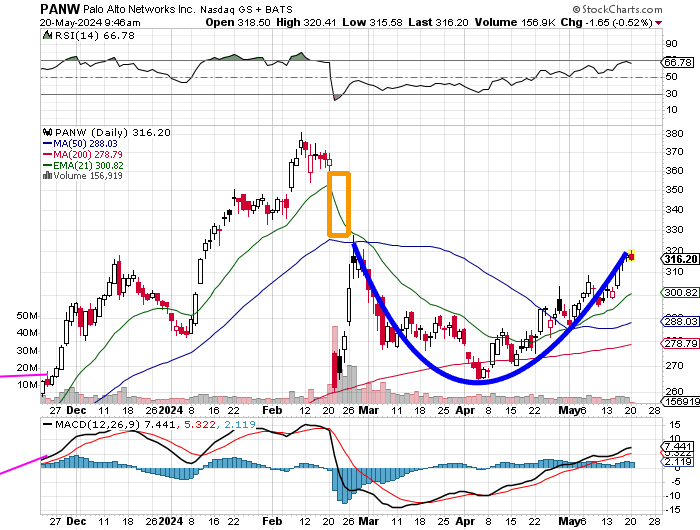

The Chart

That said, the chart is on the side of the PANW bulls. The stock has formed a cup pattern since the rally off of the February lows failed. The cup comes with a $327 pivot, with the shares not trading too far below. A breakout would put the still unfilled gap between $360 and $327 into play with the share trading above all of their key moving averages and both relative strength and the daily MACD (moving average convergence divergence) looking pretty good.

Still, the risk is that this cup might develop a handle. While potentially ultimately bullish, that would still make today a lousy day to buy the stock.

I think, if I were a PANW bull, I would rather sell $287.50 puts expiring this Friday for a credit of about $4.05 than pay up for the equity. Another idea would be to go out a month and get long a June 21st $325/$350 bull call spread for a net debit of roughly $7.30. That $7.30 would be the trader's max loss, while the max profit would come to $17.70.

At the time of publication, Stephen Guilfoyle was long CRWD, S equity.