Another Retailer Targeting Consumers on a Budget Gets Smoked

The Dollar Tree has been chopped and the stock does not seem investible at this point.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday morning, another retailer targeting consumers on a budget released their quarterly results, and another retailer targeting consumers on a budget got smoked.

Last week, Dollar General DG reported a fiscal second quarter that fell short of Wall Street's expectations for both top- and bottom-line performance, as well as same-store sales growth. Dollar General also cut guidance across those metrics going forward, and voila! DG stock gave up 32% this past Friday.

On Wednesday morning, it was Dollar Tree's DLTR turn in the barrel. For the firm's fiscal second quarter, which ended August 3, 2024, Dollar Tree posted an adjusted EPS of $0.67 (GAAP EPS: $0.62) on revenue of $7.379 billion (+0.7% year over year). As with the firm's competitor last week, these numbers both fell short of expectations, while across the enterprise, same store sales grew 0.7%, driven by 1.1% growth in foot traffic, but offset by a 0.5% decrease in the size of the average ticket.

Segment Performance

- Dollar Tree generated net sales of $4.066 billion (+4.9%), resulting in a gross profit of $1.391 billion (+7.6%) and an operating income of $342 million (-14%) as operating margin dropped from 10.3% to 8.4%. Same store sales increased 1.3%, driven by a 1.4% increase in traffic offset by a 0.1% decrease in average ticket size.

- Family Dollar generated net sales of $3.307 billion (-4.1%), resulting in a gross profit of $823.3 million (-2.2%) and an operating income/loss of $-14.6 million (down from $+11.8 million) as operating margin dropped from 0.3% to -0.4%. Same store sales decreased 0.1%, driven by a 0.7% increase in traffic offset by a 0.8% decrease in average ticket size.

Operations

As net sales grew 0.7% to $7.379 billion, the cost of those sales decreased 0.5% to $5.158 billion. Operating expenses increased 8.9% to $2.018 billion, leaving operating income of $203.1 million (-29.5%) as operating margin dropped from 3.9% to 2.8%. After accounting for interest, other income/expenses and taxes, GAAP net income printed at $132.4 million (-34%). This works out to a GAAP EPS of $0.62, down from the year ago comparison of $0.91.

Notable

In the press release, Chairman and CEO Rick Dreiling referred to the landscape that his stores are operating in as one of "immense pressures from a challenging macro environment." In the same press release, CFO Jeff Davis stated that "A portion (of the firm's underperformance) was attributable to a comp shortfall which reflected the increasing effect of macro pressures on the purchasing behavior of Dollar Tree's middle- and higher-income customers."

Guidance

For the current quarter, Dollar Tree sees net sales of $7.4 billion to $7.6 billion and comp store sales to grow in the low-single digits. Wall Street was looking for revenue of $7.5 billion, so that's in-line. Adjusted EPS is seen at $1.05 to $1.15. Wall Street had seen this number down around $1.05, so this is a positive.

For the full year, the firm sees net sales at $30.6 billion to $30.9 billion. This is well below the $31.2 billion or so that Wall Street had in mind. Comp store sales are seen growing in the low-single-digits. Full year adjusted EPS is projected at $5.20 to $5.60, which is a couple of miles below Wall Street's consensus view coming in, which was $6.55. Yikes.

Fundamentals

For the quarter reported, Dollar Tree generated operating cash flow of $306.9 million. Out of this number came capex spending of $500.7 million, leaving free cash flow of $-193.8 million. Out of that number, the firm repurchased $400 million in common stock (again, yikes), but at least did not pay shareholders a cash dividend.

Looking over the balance sheet, the firm ended the period with a cash position of $570.3 million and inventories of $5.102 billion, putting current assets at $6.092 billion. Current liabilities add up to an even $6 billion, including $1.25 billion in short-term debt. This puts the firm's current ratio at a barely acceptable 1.02 and its quick ratio (though we don't usually do those for retailers) at an awful looking 0.17.

Obviously, the firm does not have the cash on hand nor the free cash flow to take care of its debt-load maturing within 12 months. The firm will have to refinance a sizable chunk of that debt at prevailing interest rates.

Total assets amount to $22.617 billion, including $3.063 billion in goodwill and other intangibles. At 13.5% of total assets, at least this is not an issue. Total liabilities less equity comes to $15.237 billion, including another $2.429 billion in longer-term debt that is not today's headache.

My Thoughts

Well, no wonder the stock is having an exceptionally rough go of it on Wednesday. I have noticed of late that investors focused on budget conscious consumers have to be very choosy in picking out names that they think would do well in a struggling economy. While I have done well in names like TJX TJX and Walmart WMT that deliver off-priced or discounted goods to consumers, the dollar-themed stores cannot compete as their margins are squeezed and given their focus, it is more difficult for them to raise prices without losing those consumers.

Note that comp sales have struggled at Dollar General and at both Dollar Tree and Family Dollar, which is part of Dollar Tree's broader business. This is not pretty. The business is struggling. Cash flows are not strong. The balance sheet has problems. The guidance was weak. I really do not see anything here to get very excited about.

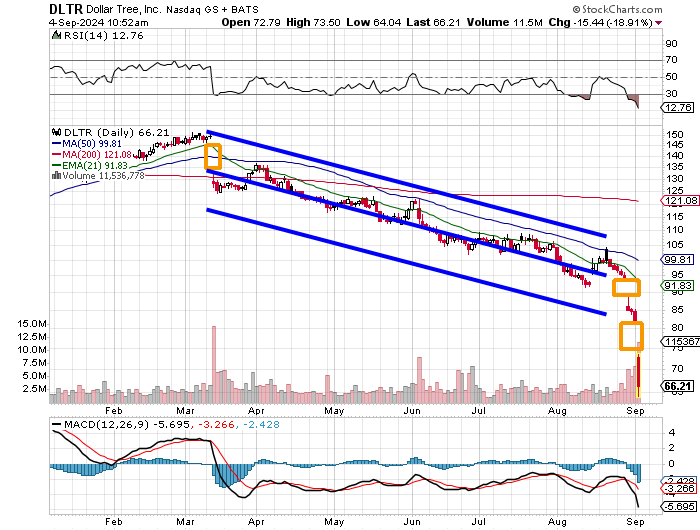

Just look at this train wreck. In a persistent downtrend since early March, the stock left a gap unfilled at the start of that change of trajectory, a gap unfilled last week in sympathy with DG, and a new gap on this morning's gap-down opening. Is that a positive? Maybe someday. Not tomorrow. This stock is a falling knife at this point. Relative strength is technically oversold with a reading of just "12" when 30 is considered negative. The daily MACD is about as bearish as bearish gets.

Just look at the 200-day SMA up at $121. The stock would need to rally 83% just to reach its own 200-day SMA. I cannot see investing in this name at this time. The stock probably is tradable, but to do so would be akin to gambling at this point. A trader willing to risk a little on the sock not staying put right here at $66 and change could go out to October 18, 2024 expiration and get long a $60/$70 strangle for a net debit of $2.45. Basically, the trader would need the stock to move either above $72.45 or below $57.55 in order to make such a play profitable. Definitely not for everyone, but the trader is hopefully not betting the farm on such a play.

At the time of publication, Guilfoyle was long TJX and WMT equity.