Dollar General Is Poised for a Big Upturn: Here's Why

Willingness to go against consensus thinking often pays off handsomely if your own ideas are more accurate.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Dollar General DG is due to release its fourth-quarter and full-year fiscal 2023 results on Thursday, March 14, prior to the opening bell.

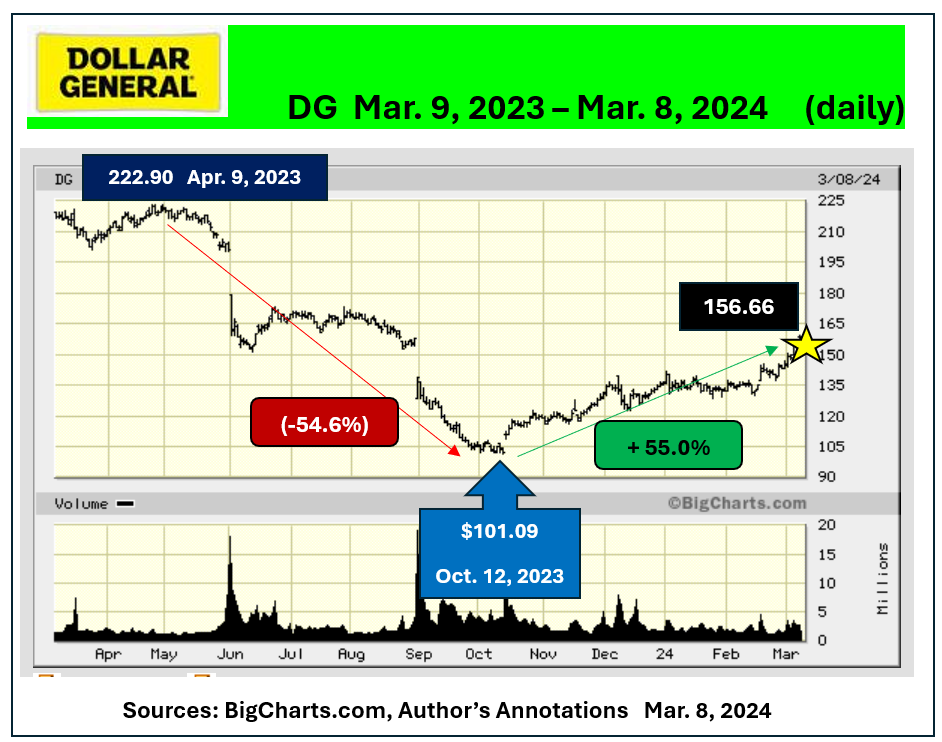

Profits are expected to lag comparable numbers from fiscal year 2022 by a large margin. Why then, have the shares rebound by over 55% since carving out a 12-month low of $101.09 early last October?

The answer? Despite declining earnings in FY 2023, DG fell way too far in relation to fundamentals.

Year-over-year earnings per share are likely going to have dropped about 29.7% while the shares had fallen 61.4% from the stock's March 2022 all-time peak of $262.20.

As of March 8, 2024, buyers at Dollar General's nadir had already regained about the same percentage as it declined from its April 2023 peak.

Those who didn't own DG until it got cheap have already pocketed excellent five-month returns.

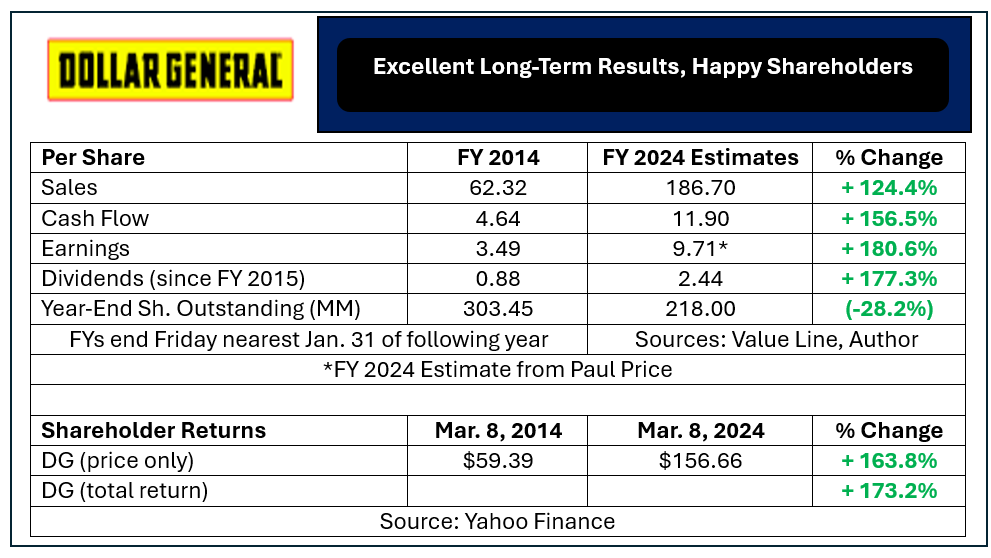

DG is a proven growth stock. All major business metrics more than doubled over the past decade. Additionally over 28% of all outstanding shares were retired using free cash flow.

Continuous shareholders were up much more one to three-years earlier, but have still been well-rewarded since 2014.

What Is DG Worth?

Answering that question requires knowing what valuation the stock typically traded for over the long-term.

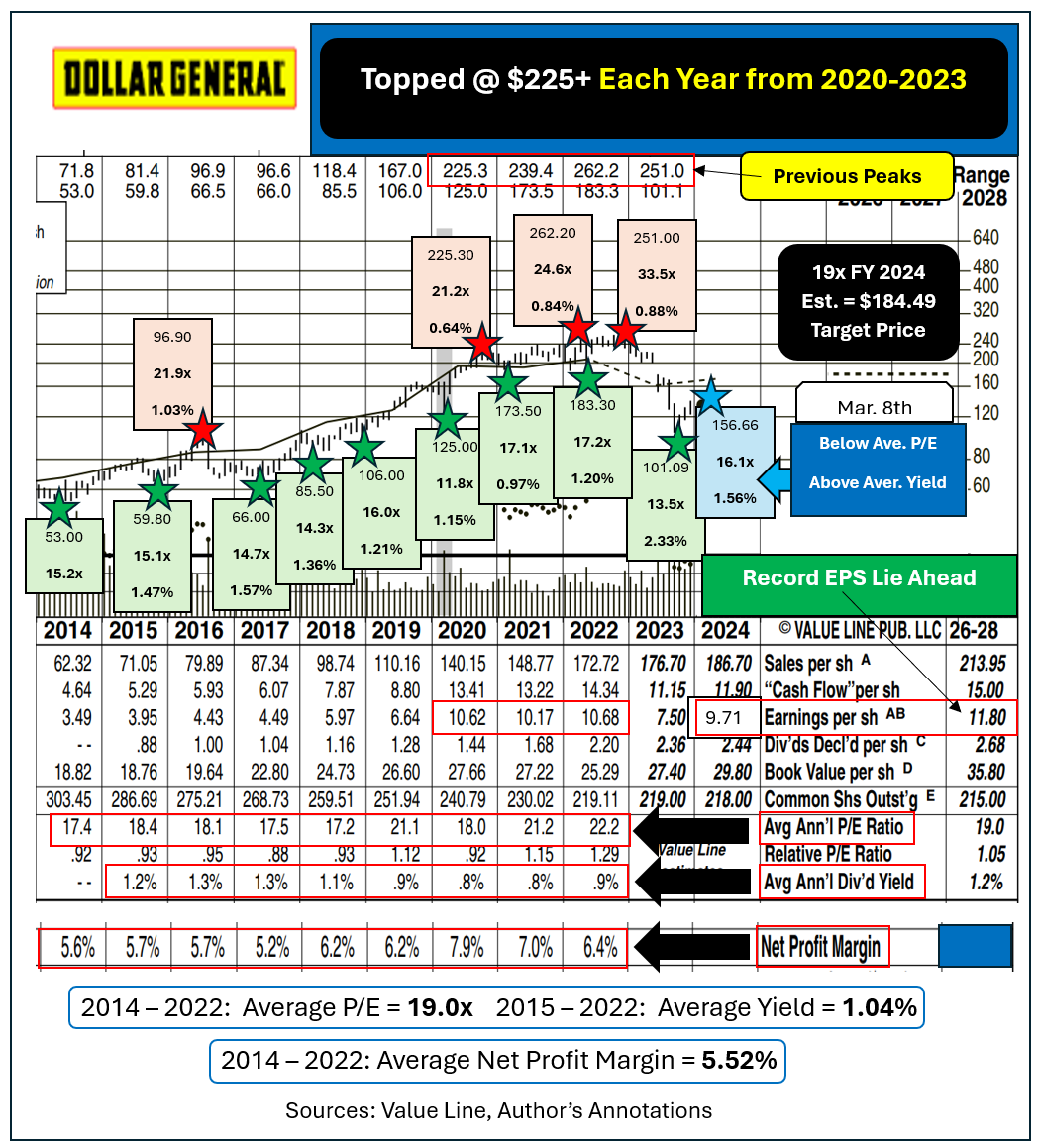

A normalized P/E calculates to 19 times and was typically accompanied by a yield around 1.04%. The very best buying opportunities in DG (green-starred below) saw multiples which ranged from 11.8x earnings at the Covid-panic low, to 17.1x in early 2021 when the stock had just established record EPS of $10.62.

Dollar General's four most recent "should have sold" moments (red-starred) each came when DG sported higher-than-average multiples along with lower-than-average current yields.

Last October's nadir came with the shares fetching the cheapest P/E and the highest yield in more than a full decade. Today's price represents a nicer-than-normal valuation on this very high-quality name.

Reverse engineering the projected $2.44 annual dividend for 2024 to a normalized 1.04% return suggests DG could rebound to as high as $234 by this time next winter.

There is another factor which I don't mention as often regarding Dollar General's prospects. From 2014 through 2022 its average net profit margin ran 5.52%. The lowest average annual net profit margin of those years was 5.2%.

A confluence of factors combined to hurt DG's results in FY 2023 (ended Feb. 2, 2024). They included higher labor costs, increased "shrink" (a.k.a shoplifting due to lax enforcement on thieves), and inflated cost of goods sold (COGS).

Profit margins for that year likely ended at an all-time worst 4.3% or so. We'll have an exact number for FY 2023 when management reports end-of-year results Thursday.

The CEO in charge during the poor year was replaced with the old CEO who set all Dollar General's records during his tenure at the helm.

Assume just a partial regression-towards-the-mean in profit margins to just 5.2%, the lowest level during the prior nine years. Based on Value Line's sales per share projection for the year already in progress and the forward EPS estimate would exceed $9.71.

A rebound to a typical 19 multiple would justify a 12-month target price of $184.50. My personal guess is that DG will outperform relatively pessimistic projections from most analysts, who tend to go with the trend in place continuing until proven wrong.

Yahoo Finance's consensus estimate for FY 2024 is just $7.55. Value Line's runs only $8.40. If my estimate proves more accurate than theirs analysts will be forced to start raising year-ahead numbers in a significant way.

Increasing estimates almost always translates into higher-than-average P/Es. Dollar General proved it can earn over $10 per share during each of the three years from 2020 through 2022. The shares topped out between $225 and $262 during each of those years plus in early 2023 on the way down.

Once it becomes clear that the firm can beat or exceed $10 in EPS again I'd expect the shares to be way over $200.

Owning DG shares outright is the best way to obtain unlimited upside with no preset time horizon.

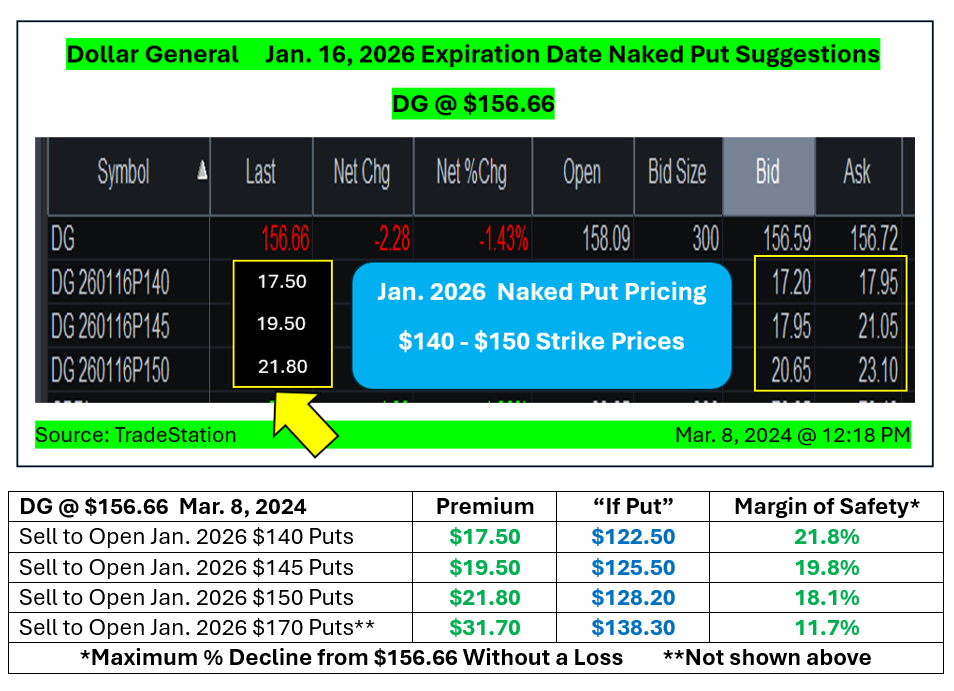

Option-savvy traders can also lock in generous naked put premiums on both in-the-money and out-of-the-money naked put sales as far out as Jan. 16, 2026. That allows for plenty of time for DG to see much higher EPS as well as gradually increasing dividend payments.

Worst-case net purchase prices on the out-of-the-money puts shown dropped to between $122.50 and $128.50, offering margins of safety of 18.1% to 21.8%.

The more aggressive $170 puts dropped the "if put" price to a still bargain price of $138.30 while offering almost $32 per share in premium per share if they end up expiring worthless as I expect.

My recent article on Peter Lynch's traits for successful investing listed "doing your own research" as one of the attributes needed. Willingness to go against consensus thinking often pays off handsomely if your own ideas are more accurate.

I believe Dollar General will see EPS rebound faster and harder than most other analysts. If so, DG can be back in the $200-plus range much sooner than they anticipate.

At the time of publication, Price was long DG shares, short DG naked puts, short out-of-the-money covered calls. Dollar General is one of Price's top 10 largest personal dollar holdings.