Cruise Giant Isn't a Lost Cause, but Trading Will Require Some Finesse

This is a tough-looking name to own, but there could be a way for traders to profit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday morning, Carnival Corporation CCL, released the firm's fiscal third quarter financial results. For the three-month period ended August 31, 2024, Carnival posted a GAAP EPS of $1.26 (adjusted EPS: $1.27) on revenue of $7.896 billion.

These top- and bottom-line numbers both beat Wall Street's expectations, while that revenue print was good enough for year-over-year growth of 15.2%. The top-line number was also the firm's all-time best revenue print for a third quarter. As leaders will see, the firm not only raised full year fiscal 2024 guidance, but the cumulative advanced booked position for full fiscal year 2025 is running ahead of 2024 with prices also ahead of the prior year.

The CEO

CEO Josh Weinstein commented in the press release: "We delivered a phenomenal third quarter, breaking operational records and outperforming across the board. Our strong improvements were led by high-margin, same-ship yield growth, driving a 26% improvement in unit operating income, the highest level we have reached in 15 years."

Weinstein then added, "We are poised to deliver record operating performance for full year 2024, with adjusted EBITDA now expected to cross $6 billion and adjusted return on invested capital to be approximately 10.5%. Strong demand enabled us to increase our full-year yield guidance for the third time this year and we improved our cost guidance driving more revenue to the bottom line."

Operations

As mentioned above, revenue generation was up 15.2% to $7.896 billion. Passenger ticket sales were up 15.2% to $5.239 billion, while onboard sales were up 15.1% to $2.657 billion. Total operating expenses that include administrative costs as well as depreciation and amortization, came to $5.718 billion (+9.3%).

This left an operating income of $2.178 billion (+34.1%) as operating margin expanded from 23.7% to 27.6%. After accounting for interest, other income and expenses and taxes, GAAP net income printed at $1.735 billion (+61.5%). This works out to earnings of $1.26 per fully diluted share, up from $0.79 for the year ago comparison.

Fundamentals

For the period reported, Carnival generated operating cash flow of $1.205 billion. Out of this number came $578 million in capex spending. This left free cash flow of $627 million. Carnival has not paid a cash dividend to shareholders since the onset of the pandemic in early 2020.

Glancing at the balance sheet, we see that Carnival ended the quarter with a cash position of $1.522 billion and inventories of $492 million. That brought current assets to $3.626 billion. Current liabilities add up to $12.265 billion. It's bad, but not as bad as it looks.

Included in those current liabilities is $2.214 billion in debt that will come due within 12 months. That is going to require the firm to refinance a chunk of that debt at rates that might be improving but will still likely be higher than what the firm had been paying to borrow. Also included in that number is $6.436 billion in customer deposits, also known as deferred revenue. That's not a financial obligation at all, as long as the firm honors those tickets.

All told, at the headline, the firm's current and quick ratios stand at an awful looking 0.29 and 0.26. Once adjusted for those deferred revenues, these two ratios rise to 0.62 and 0.54. Still hard to look at, but the firm is working on paying down its hefty debt load.

Total assets amount to $49.805 billion, that includes a small amount of intangibles. Total liabilities less equity comes to $41.207 billion, and that number does include another $26.642 billion in long-term debt. Debt management is the story here.

Guidance

For the current (fourth) quarter, Carnival sees adjusted EBITDA of $1.14 billion, which would be up 20% from FQ4 2023, but an adjusted net income of just $60 million. For the full fiscal year, Carnival now projects adjusted EBITDA of $6 billion, up from prior guidance of $5.83 billion and up more than 40% from the year-ago comparison. As far as adjusted net income is concerned, the full year is now seen at $1.76 billion, up from guidance of $1.55 billion three months ago and guidance of $1.275 billion six months ago.

My Thoughts

This is still a tough looking name to own, from my vantage point. They had a great quarter, but it may have been a one-off. The full year guidance was largely due to the monster third quarter. Forward-looking quarters look like a return to the less profitable past. Sure, the demand is there and so is free cash flow. That cash flow is going to have to stay positive and sizable as this firm is unfortunately over-indented. Still the effort is obviously there, not only to continue this company's turnaround, but to reduce that debt burden. I am not surprised that the market reaction to a solid quarter and a guidance increase is negative.

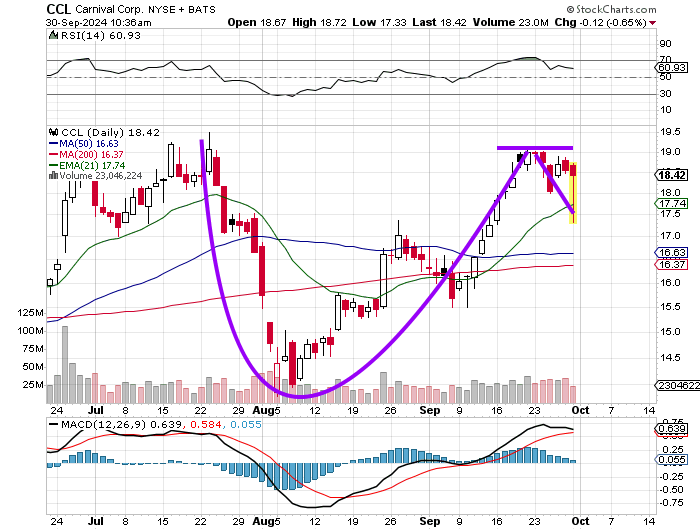

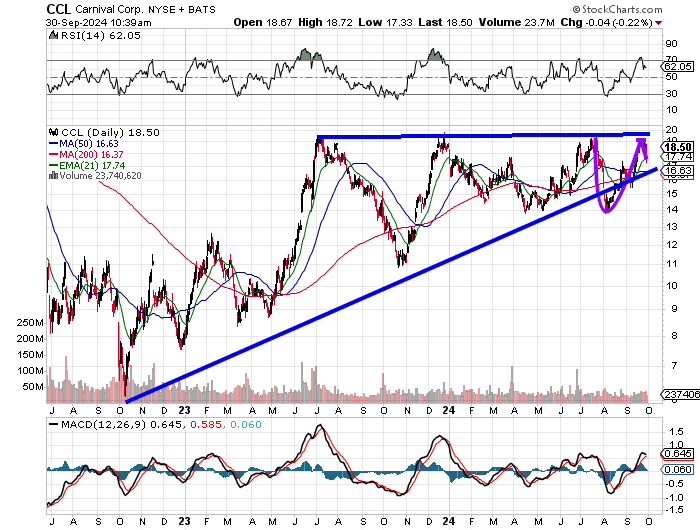

Taken in isolation, readers likely see a cup-with-handle pattern with a rough $19 pivot — a positive, if unspectacular reading for relative strength and daily MACD that, while postured bullishly, is threatening a bearish cross-under of the 26-day EMA by the 12-day EMA. However, let's zoom out a bit if you don't mind.

What we have here is really a very long ascending triangle going back to October of 2022 with a pivot that's really more like $19.50. My thoughts? I'll buy this stock closer to its 50-day SMA ($16.63), or I'll buy it on momentum above $19.50, but not in between.

One strategy might be to go out about six weeks and purchase $19 November 15 calls for about $1, while selling twice as many $17 November 15 puts for a rough $0.60. The trader will realize a small credit on those transactions but can take his or her time and allow the stock some time to choose what to do with that technical set-up.

This stock, in my opinion, is not the lost cause that its balance sheet suggests. That said, getting involved will, also in my opinion, require a bit of finesse.

At the time of publication, Guilfoyle had no positions in any securities mentioned.