CarMax Races Past Wall Street Expectations, but Is it a Buy?

CarMax has reported its financial results amid a period of contraction for the used car business.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Friday morning, CarMax Inc KMX released the firm's fiscal first quarter financial results. For the three-month period ended May 31, 2024, CarMax posted a GAAP EPS of $0.97 on revenue of $7.113 billion. These top- and bottom-line numbers both beat Wall Street's expectations despite a year-over-year contraction of 7.5% on the sales print. With the broader used car business generally in a state of contraction, these numbers provide investors with some relief. The fact that, as readers will see, margins held up quite well was also received quite well.

Operations

As revenue was contracting 7,5% to $7.113 billion, the cost of sales dropped by 8% to $6.322 billion, leaving a gross profit of $791.895 million (-3.1%), as gross margin improved from 10.6% to 11.1%. After accounting for auto finance income (+2.6%), operating expenses (+14.1%) interest expense (+2.9%), and depreciation/amortization (+5.9%), the firm was left with net income of $152.44 million, which was down 33.2% from the year ago comp, but still better than expected. This works out to the GAP EPS print of $0.97, down from $1.44 a year ago.

Key Data

Used vehicle sales contracted 3.1%, as average selling price contracted 2.7% and used vehicle gross profit contracted 3.7%. Gross profit per used vehicle contracted 0.6% to $2,347.

Wholesale vehicle sales contracted 8.3%, as average selling price contracted 10.3% and wholesale gross profit contracted 6.4%. Gross profit per used wholesale increased 2.1% to $1.064.

The company bought 314,000 vehicles from consumers and dealers, which was down 8.6% from the year ago comparison.

Guidance

I did not see any precise financial guidance mentioned either in the press release nor in the earnings call. That said, there was plenty of talk during the call about improving the firm's buildout of CarMax Auto Finance, so that it can become a more significant contributor to the firm's welfare overall. That said, the firm is holding its virtual annual shareholder meeting this coming Tuesday, so the intent could be to provide an actual outlook for the current fiscal year at that event.

Fundamentals

Cash flows are a problem for CarMax. For the period reported, CarMax generated operating cash flow of $-117.689 million. On top of that, the firm added on capex spending of $103.914 million, leaving the firm with free cash flow of $-221.603 million. The firm also repurchased and retired $106.85 million worth of common stock, so there is an imbalance here that will need to be corrected.

Looking at the balance sheet the firm has a cash position of $755.338 million, of which $536.407 million is currently restricted. That's down from $1.082 billion just three months earlier. Inventories landed at $3.773 billion, leaving current assets at $4.97 billion. Current liabilities add up to $1.986 billion, including a small amount of regular short-term debt and $514.394 million in non-recourse notes payable.

This puts the firm's current ratio at 2.5, which is very good. However, these numbers are tricky. Ex-restricted cash, the current ratio falls to 2.23. Ex-inventories, what we know as the quick ratio prints at 0.60. That's OK, given the industry we're in here. Ex-restricted cash, that quick ratio falls to just 0.33, which would not be so very healthy.

Total assets amount to $27.242 billion, including a very small number for intangibles. Total liabilities less equity comes to $21.075 billion, including $1.591 billion in normal long-term debt and $16.626 billion in non-recourse notes payable. Yikes. The firm is in a scary position as it has only $218.9 million in cash that it can touch on the books and a total debt-load of $18.753 billion. Wow, that's one heck of an imbalance.

My Thoughts

Yes, these results were better than expected and certainly better than feared. That said, cash flows have been negative while the firm has repurchased stock, and the long-term health of the balance sheet is highly questionable. The stock trades at 24 times forward-looking earnings. which is expensive. Additionally, at least as of mid-May, 14% of the float was held in short positions. There is enough not to like in this name to just stay away from the long side for anything beyond a trade.

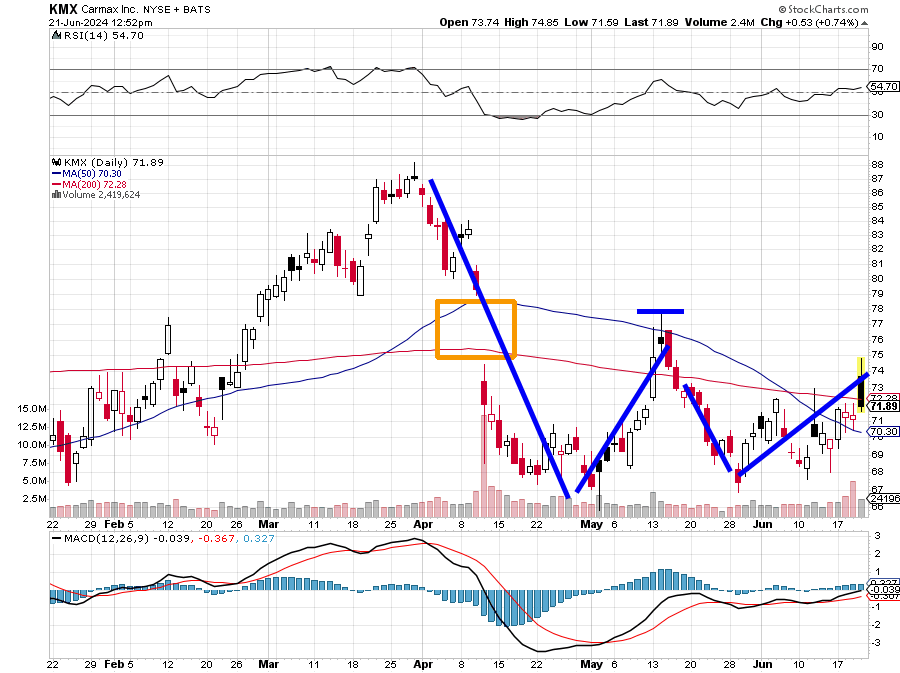

The chart is somewhat better than the fundamentals in this name. Readers will see a double bottom reversal that has left an unfilled gap that would need to see a tick at $79 or higher to fill. The double bottom pattern bears a pivot point of $78, which is where a breakout would occur. So far, the stock has not come close to that level on Friday. The stock may get another boost next Tuesday during or in response to the annual meeting. If the shares fail to take and hold $78, this stock is a "no-go" for me. I would suggest selling July puts with a $65 strike price rather than an equity position, but there is not much value in those right now.

At the time of publication, Guilfoyle had no positions in any securities mentioned.